We scan the latest real GDP data to understand the pressures on the equity market. Our conclusions on GDP will be free for all to read, while our views on the S&P 500 will be reserved for clients.

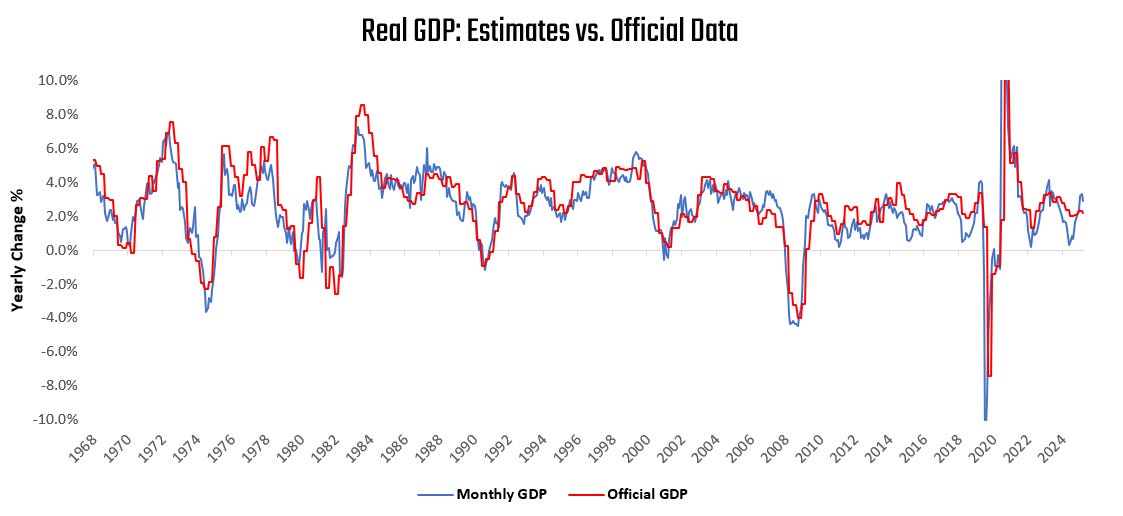

For the latest data through December, our systems place Real GDP growth at 2.88% versus one year prior. Below, we show our monthly estimates of Real GDP relative to the official data:

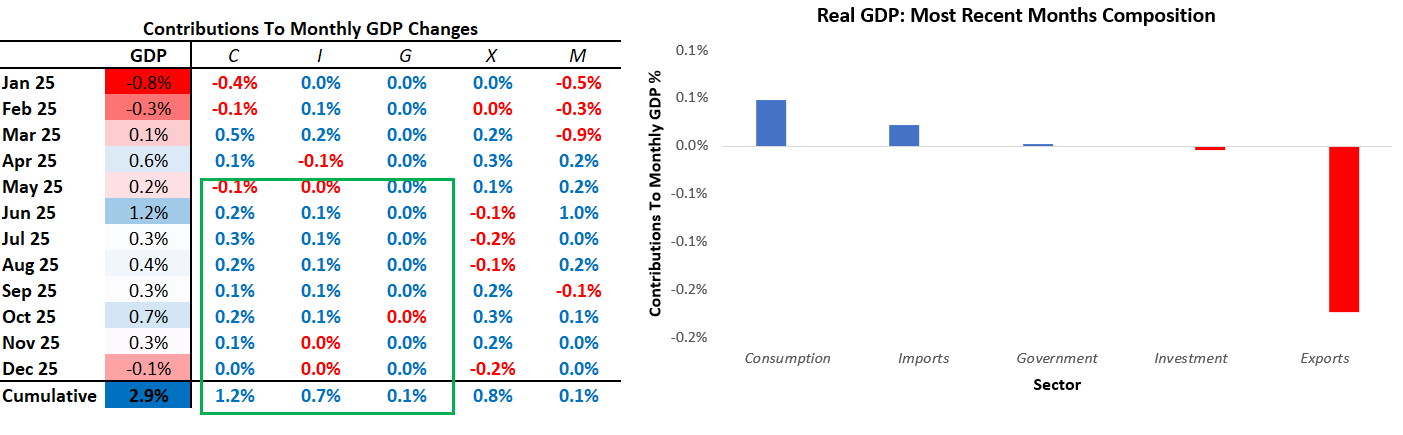

In December, GDP came in at -0.11% versus the prior month. Below, we show the weighted contributions to the most recent one-month change in real GDP, along with the recent history of month-on-month GDP. Additionally, we show the contribution by sector to monthly GDP in the table below:

The domestic engines of growth continue to hold steady and remain additive to real output, though we see some signs of slowing. We scan through the individual components, with a focus on domestic activity.

Consumption

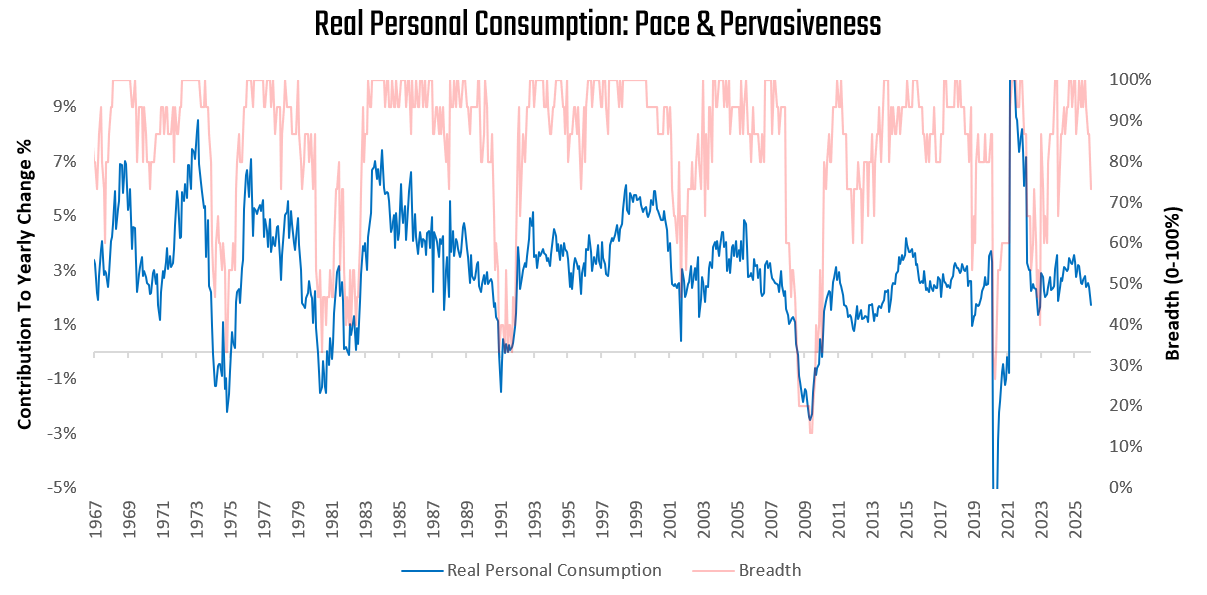

In December, real consumption spending increased by 0.05%. Over the last year, consumption has added 1.2% to the GDP growth of 2.88%.

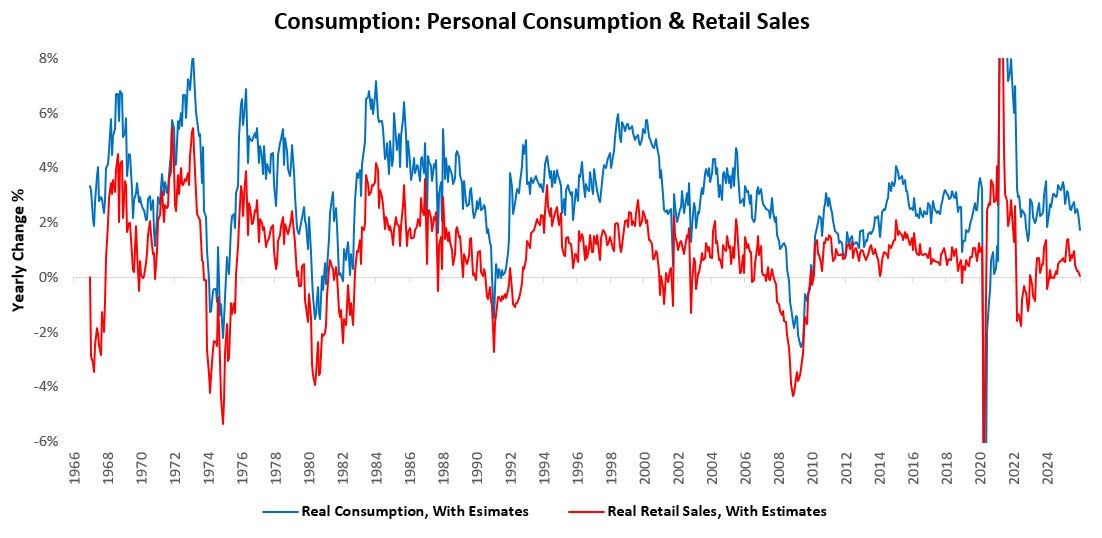

Under the aggregate data, services spending continues to support ongoing consumer spending, while goods have become a meaningful drag:

Even though aggregate consumption remains positive, some slowing is apparent, and is reflected in a narrowing of consumer spending breadth:

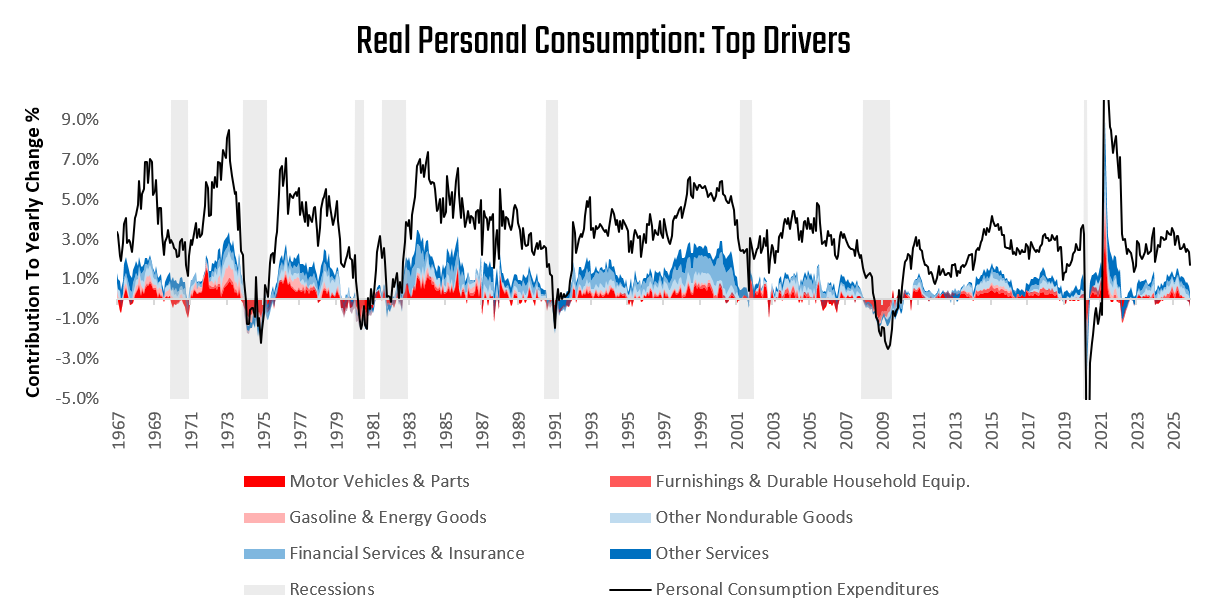

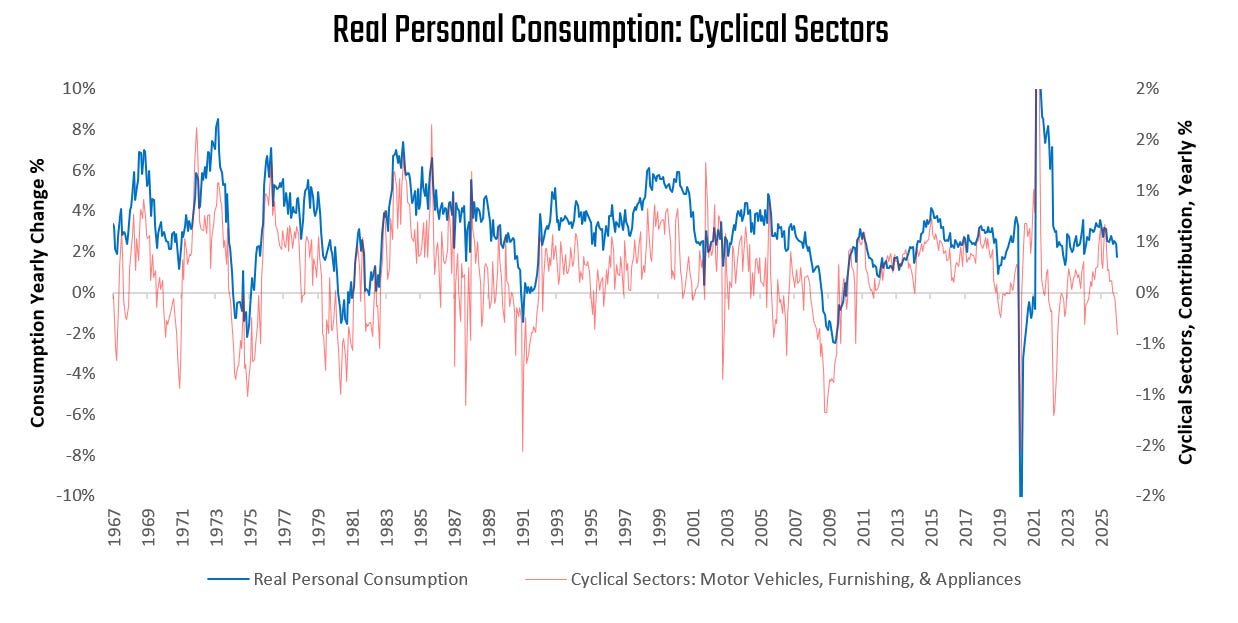

This narrowing breadth of consumer spending is largely coming from weak cyclical consumer spending:

In past cycles, this weakness in cyclical spending would, in itself, have been a cause of recession. However, the shifting structure of the economy towards a services-dominated one continues to keep the economy steady. Nonetheless, this is something to monitor closely.

Investment

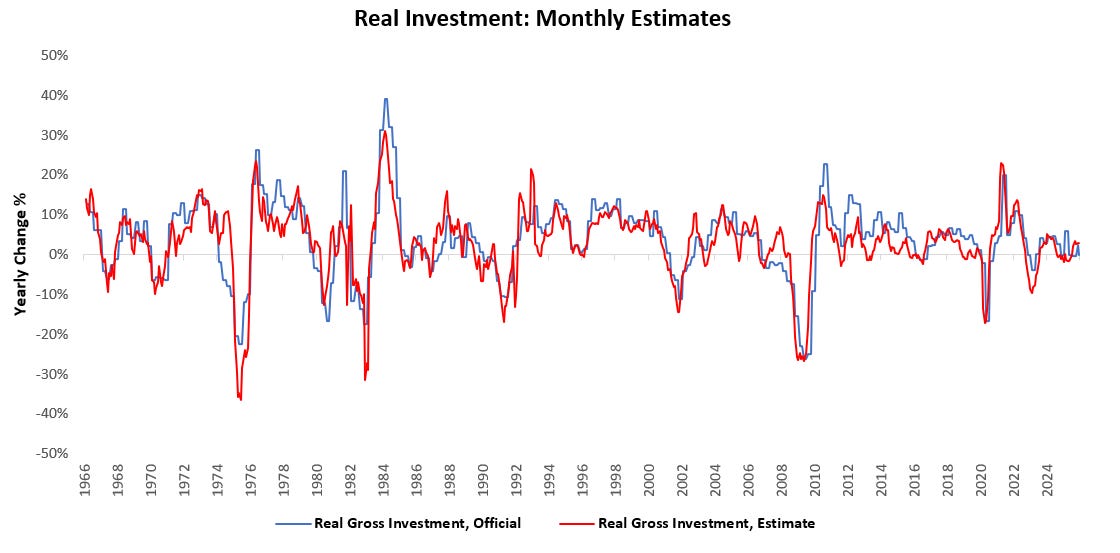

In December, real gross investment remained flat. Over the last year, investment has added 0.65% to GDP growth of 2.88%.

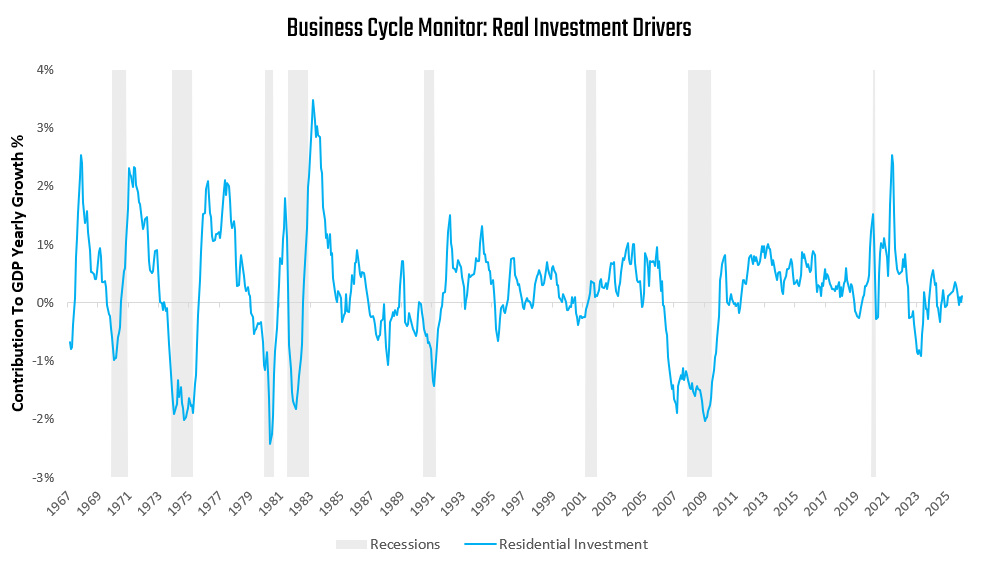

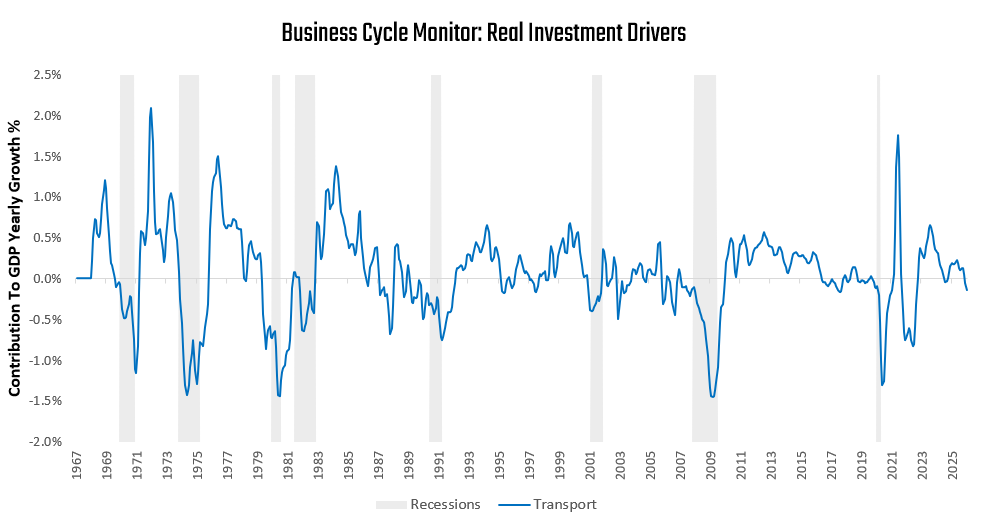

Business investment remains weak, with construction and transportation spending continuing to weigh on fixed investment:

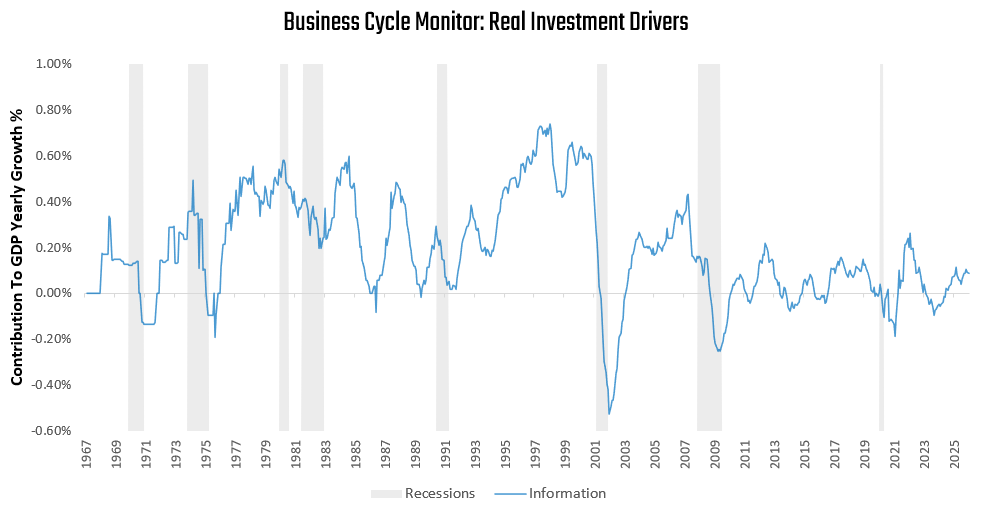

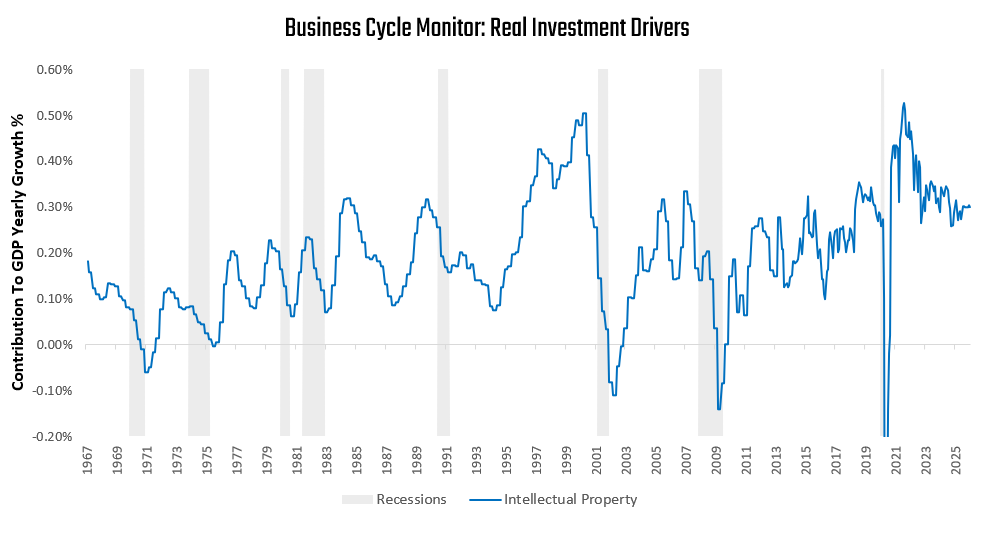

While these classically cyclical areas of the economy continue to show weakness, technology and related areas continue to show steady growth:

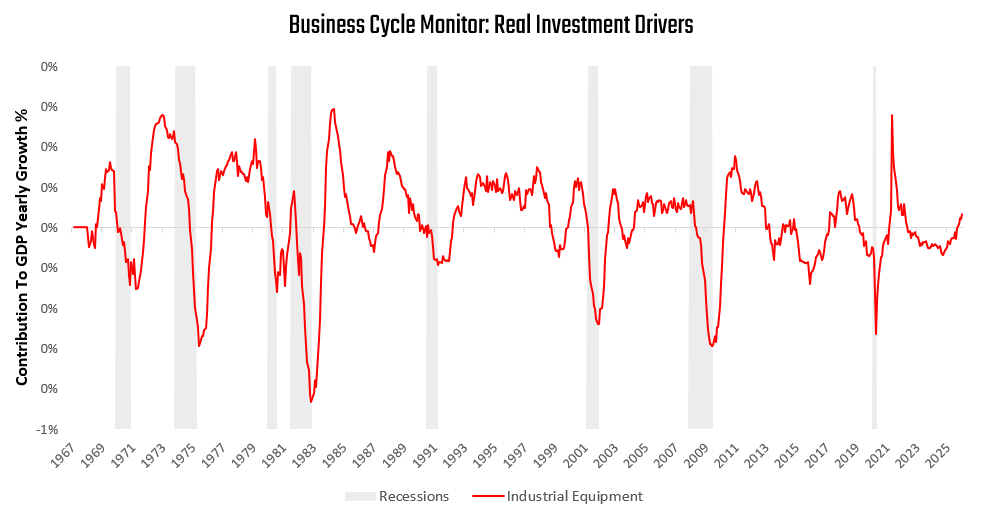

Finally, and most notably, industrial equipment investment has turned upwards:

Importantly, this upturn has been a broad-based one:

Much like consumer spending, business fixed investment shows readings that in past cycles have looked consistent with recessionary pressures, with declining residential construction and transportation equipment spending. However, the revival of industrial equipment investment and the stability of technology investment continue to deter recessionary downturn.

Government

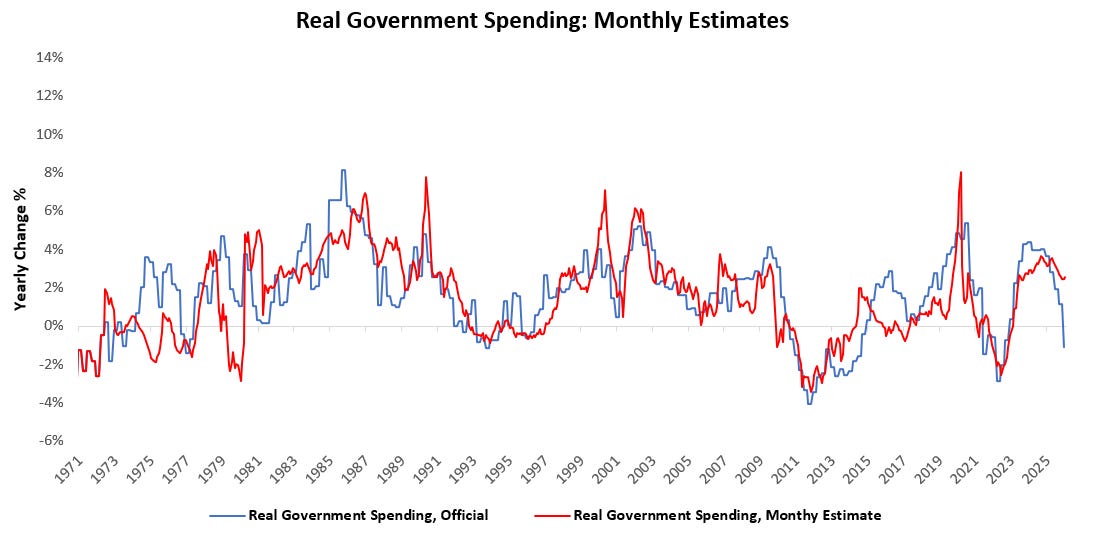

In December, real government expenditures increased by 0%. Over the last year, government spending has added 0.09% to real GDP growth of 2.88%.

Government output has moderated meaningfully per the official data and diverged from our estimates. However, we find this to be a feature of the BEA's treatment of the government shutdown rather than an indication of a major shift in government output. This is because furloughed federal employees received back pay; the shutdown had no impact on nominal federal compensation and was reflected as a temporary increase in the prices paid for federal employee compensation. Below, we show how nominal spending continued despite a modest downtick:

With the resumption of regular operations of the government, we expect government spending to converge with our estimates over the next quarter.

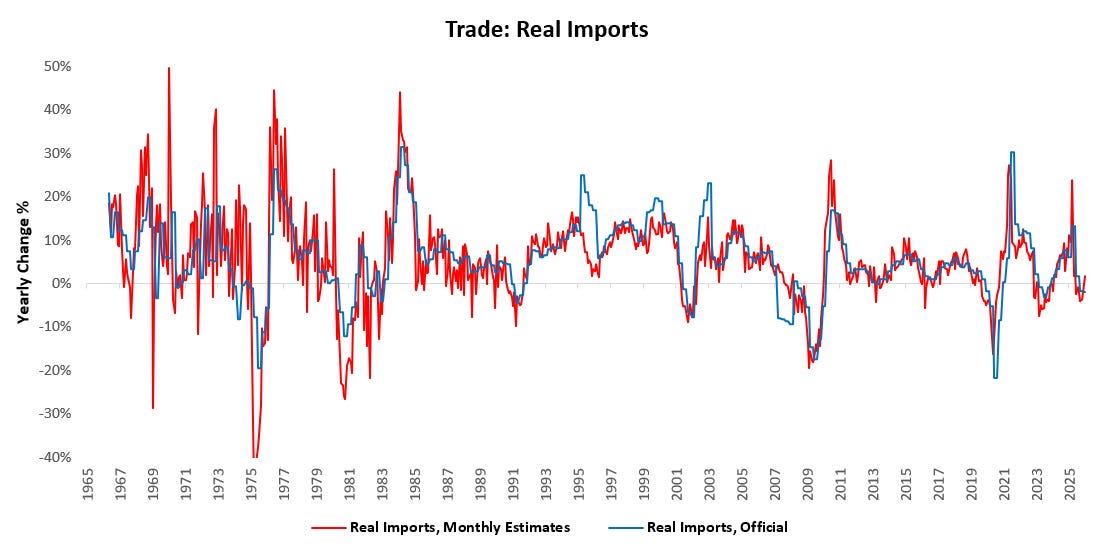

Trade

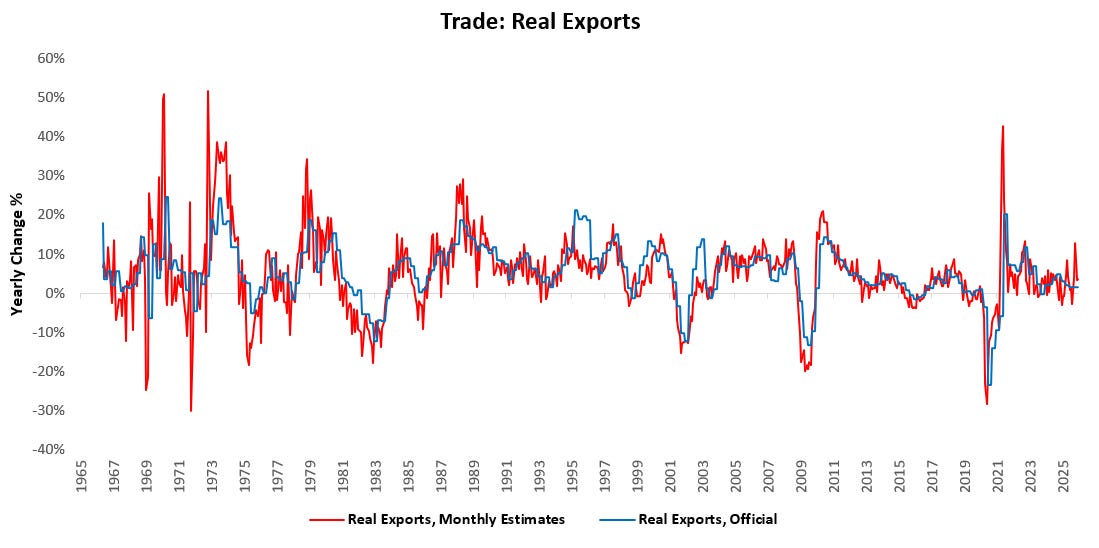

In December, real export revenues decreased by -0.17%. Over the last year, exports have added 0.78% to GDP growth of 2.88%.

In December, real import expenditures increased by 0.02%. Over the last year, imports have added 0.13% to GDP growth of 2.88%.

The key takeaway is that trade is no longer a major incremental tailwind, but it is not exerting material drag either. The impulse from global demand has moderated, yet it remains broadly consistent with steady expansion rather than contraction.

At present, the domestic economy continues to carry this cycle. Trade is neutral-to-slightly supportive, not a source of stress.

GDP: Synthesis

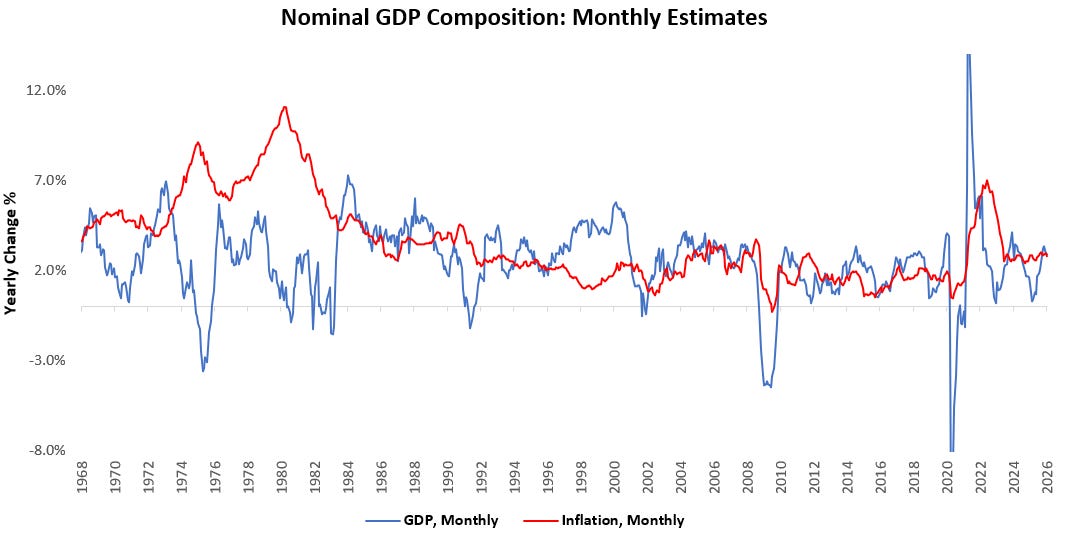

Additionally, we show the composition of the monthly estimates of nominal GDP, broken into real GDP growth and inflation. Our latest estimates place nominal GDP at 5.86% versus one year prior, with real GDP growth of 2.88% and inflation of 2.98%:

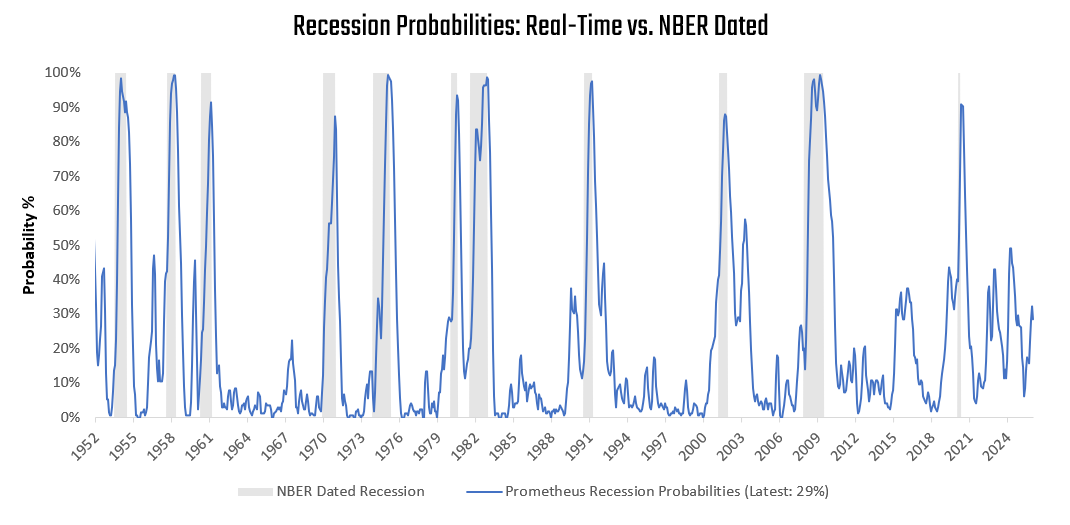

For further insight into whether GDP conditions are consistent with recessionary pressures, we aggregate macroeconomic indicators, consistent with the NBER methodology of recession classification, into a recession probability monitor. This gauge gives us a real-time understanding of developing recessionary pressures. Currently, recession probabilities are at 29%:

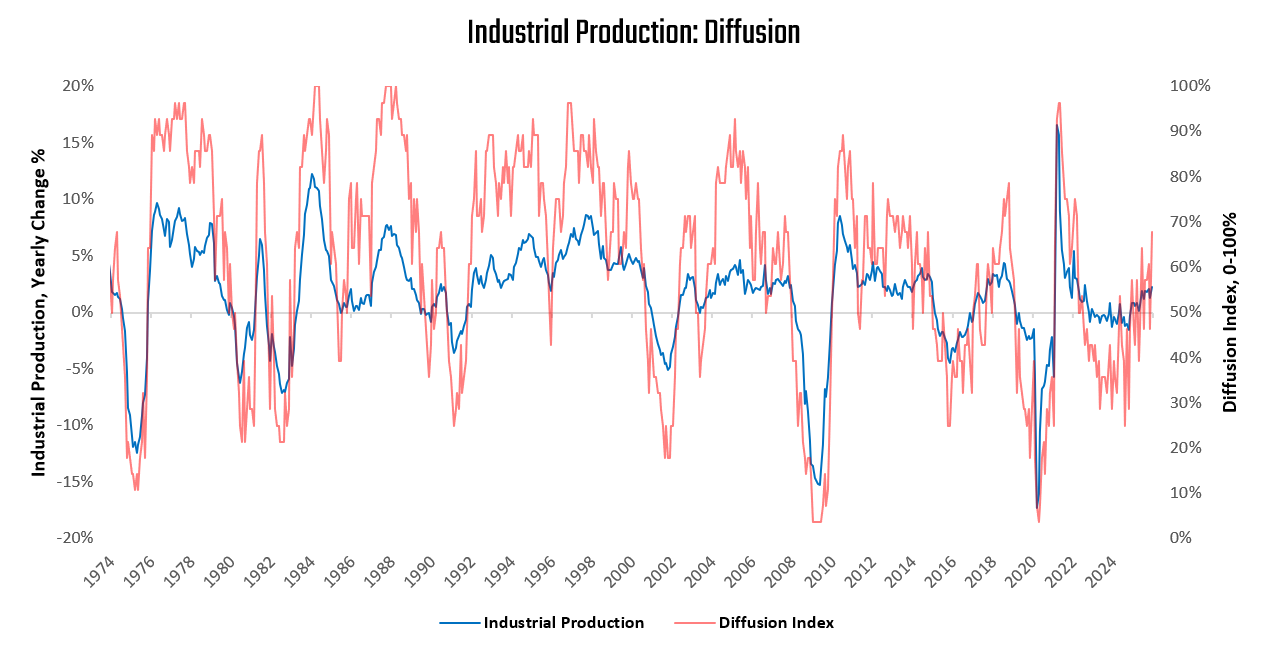

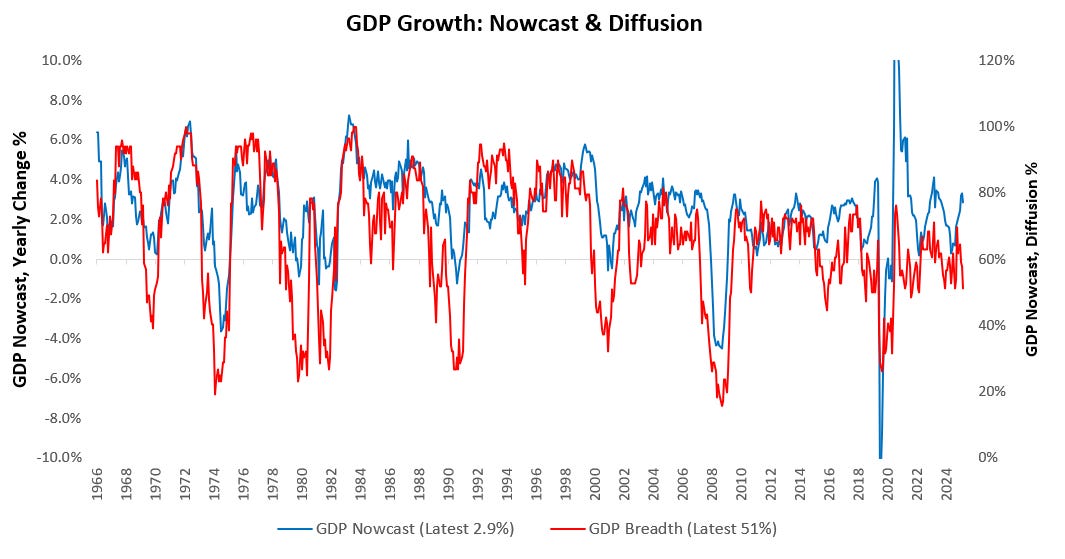

Finally, we zoom out to offer what the mosaic of economic data says about the pervasiveness of GDP growth. Our GDP Nowcast economic data across 75 measures of real growth conditions to understand the economic conditions in a timely manner. We share both the current level of the nowcast in blue, along with a diffusion index of the underlying components in red. Currently, 51% of subcomponents are rising, consistent with early indications of a recession:

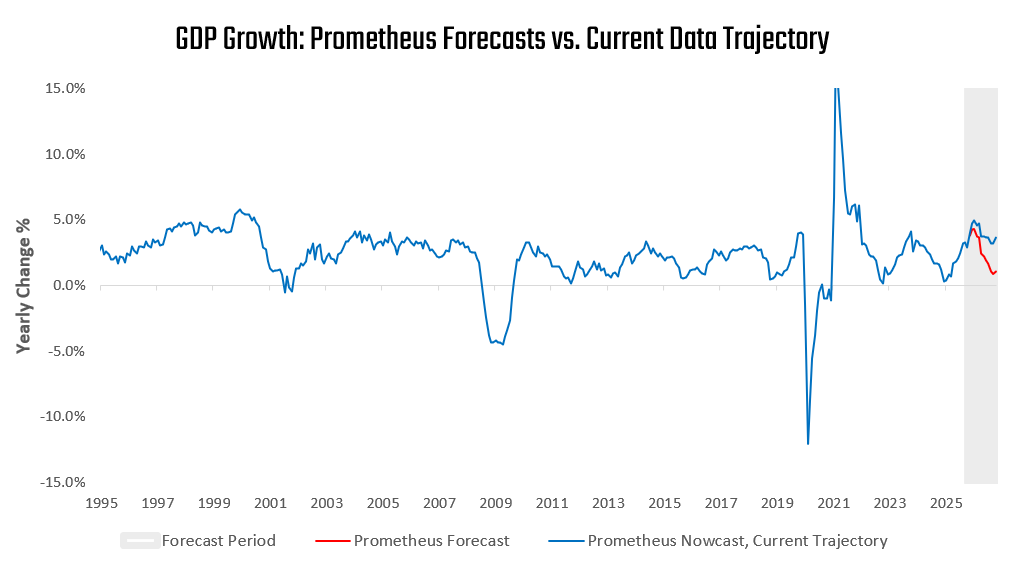

Below, we visualize the prospective paths of real GDP growth over the next twelve months using our data trajectory monitor. We share two processes. First, we extrapolate the current trend in the data to visualize the prospective trajectory of GDP based on the current trend. Additionally, we share our forward-looking estimates for real GDP growth:

GDP conditions remain mixed. Classical cyclical and rate-sensitive parts of the economy continue to show weakness, while non-cyclical areas add stability. Given these conditions, GDP growth will likely peak in the next 3 to 6 months, driven by time-series effects. A mixed, but positive outlook for the economy persists.

Equity Strategy

We translate these fundamental macro dynamics into systematic investment views for the equity market. When approaching equity markets, we think there are four major perspectives from which to take market views:

Expected Returns

Cyclical Regime

Earnings Mispricing

Tactical Positioning

These views span the spectrum of timeframes we can express our equity views on. We offer our systematic readings for each.