This is a note from Prometheus Institutional.

The latest CPI data came in materially colder than expected. Markets have taken this as confirmation that the disinflationary trend will continue, reducing the pressure on the Fed to hike policy rates. This may be premature. We scan through the data and offer our assessment.

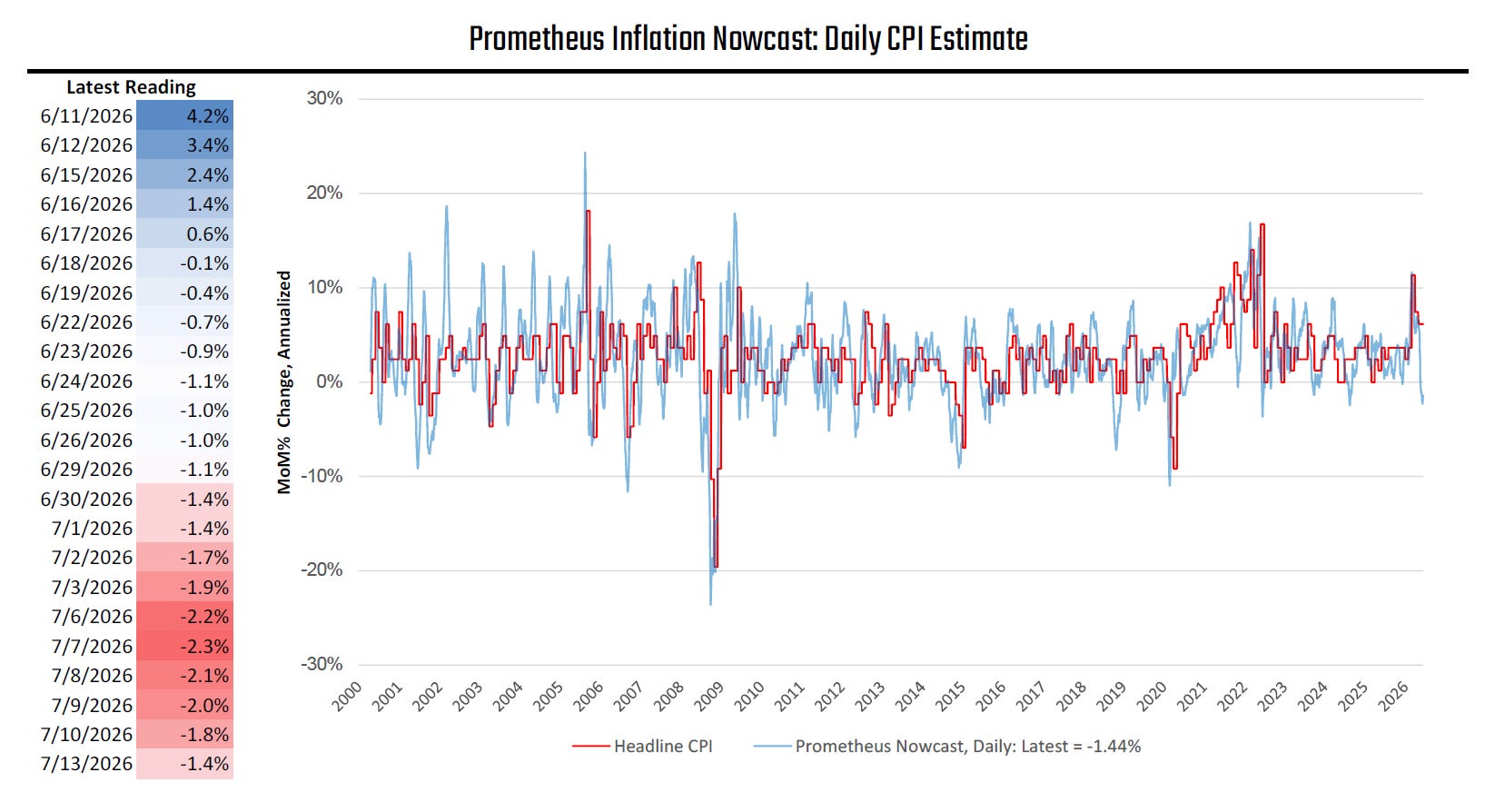

The softness in the headline data was largely in line with our CPI Nowcast, with oil prices materially weighing on the headline CPI. We show our estimates headed into today’s release below:

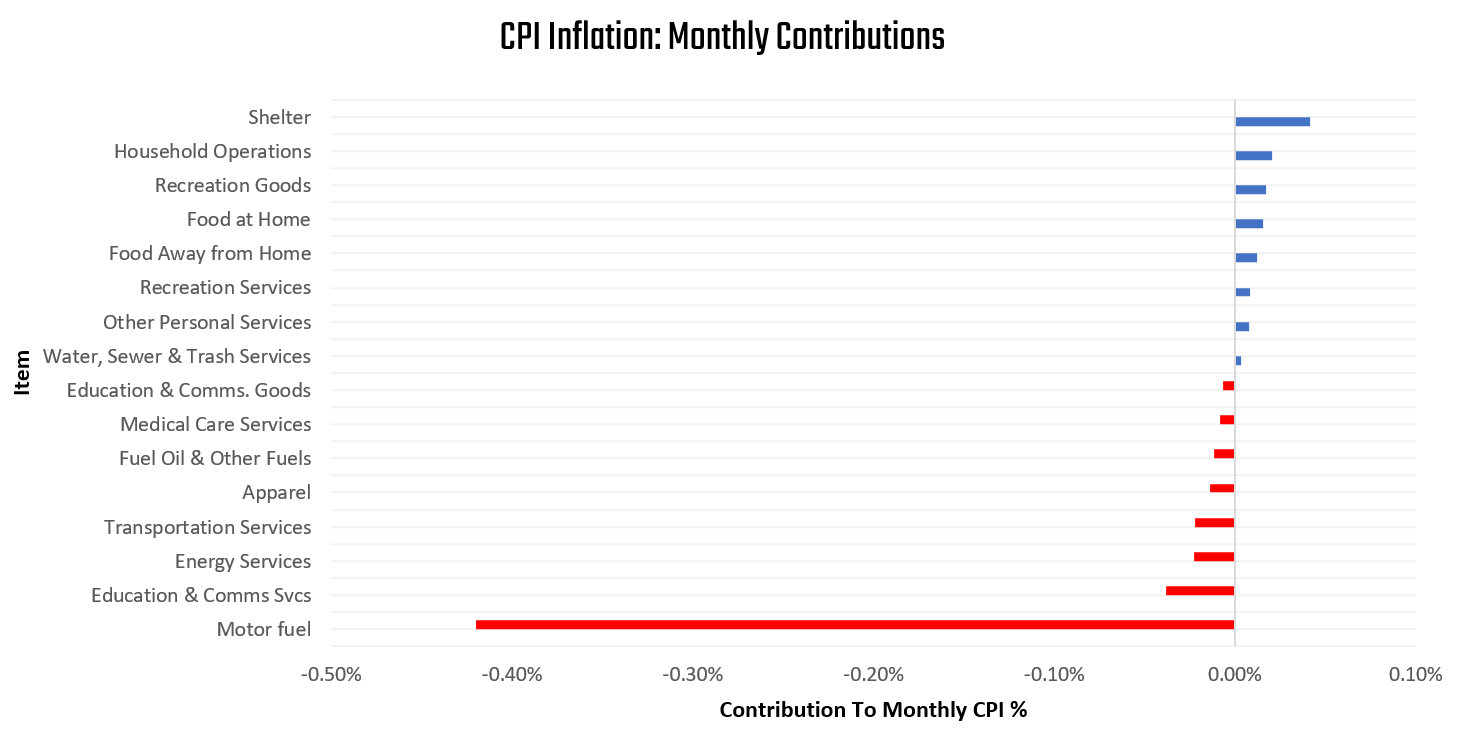

Headline inflation came in even more negative than our estimates, however. This was driven, in large part, by a slowdown in shelter inflation, coupled with price declines in transportation services:

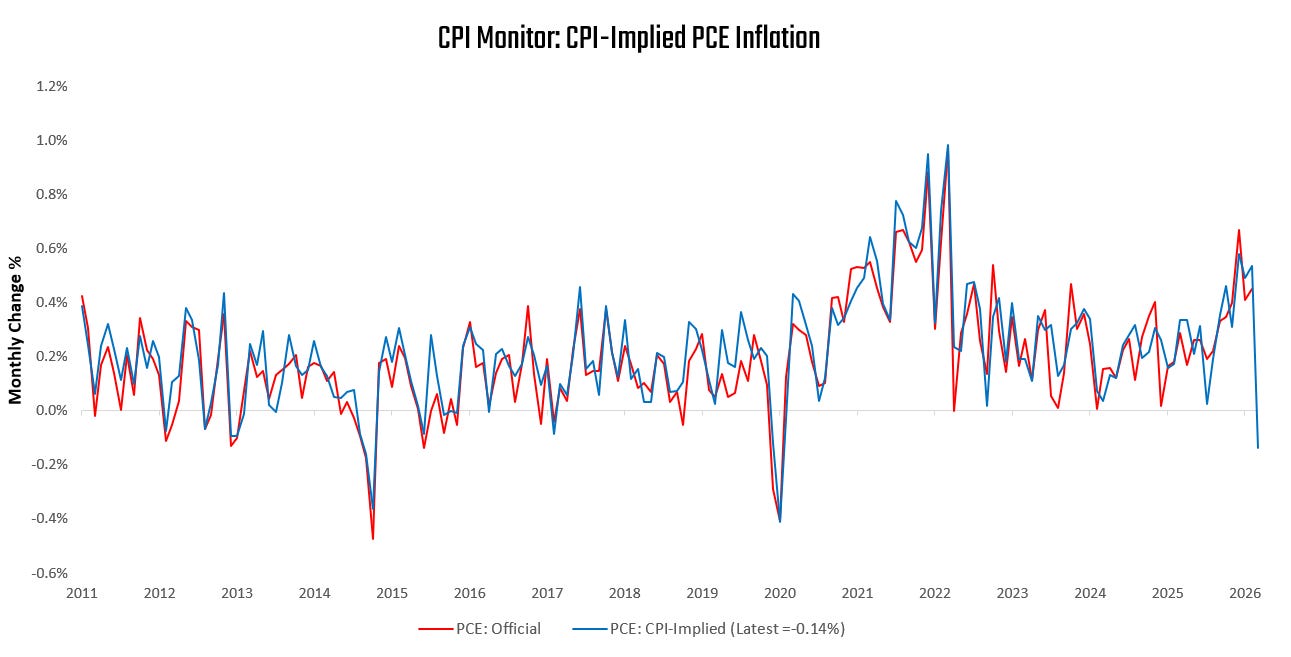

This weak data implies weaker PCE inflation. We estimate the next PCE reading using the latest CPI data:

The latest CPI data suggests a -0.14% headline PCE print in June, bringing the 6-month trend in headline PCE to 4.4%. This is a much more timid disinflationary effect than CPI itself suggests.

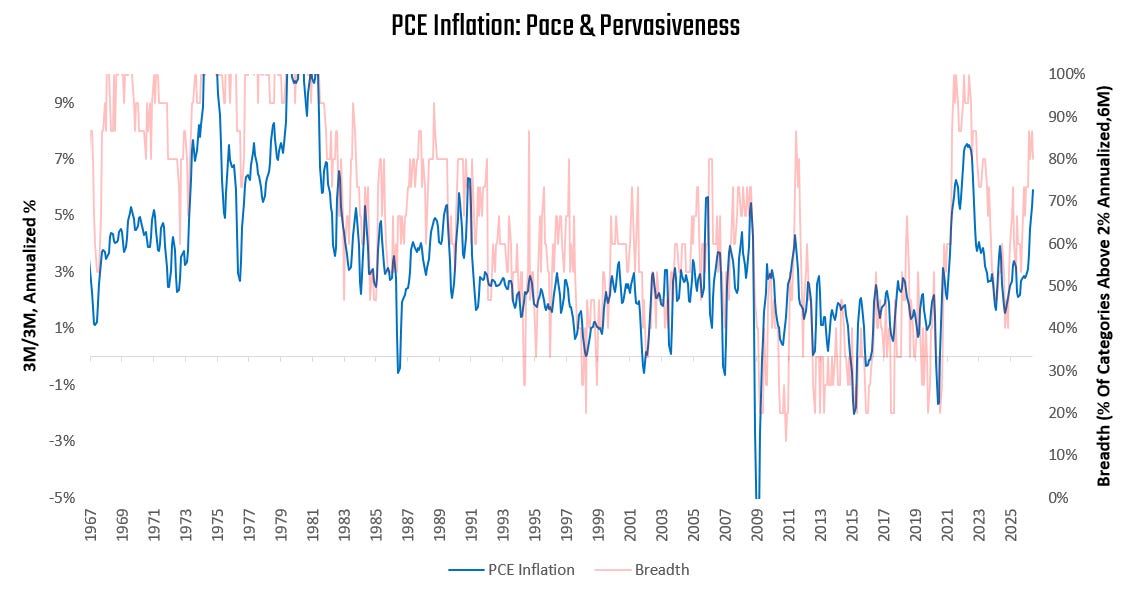

Furthermore, reconciling the components of this CPI print that drive their respective PCE counterparts, we continue to see inflation breadth as pervasively elevated:

Accounting for the latest CPI data, our estimate of PCE breadth (% of areas with 6M annualized inflation >2%) remains unchanged, with 80% of sectors showing inflation above the target.

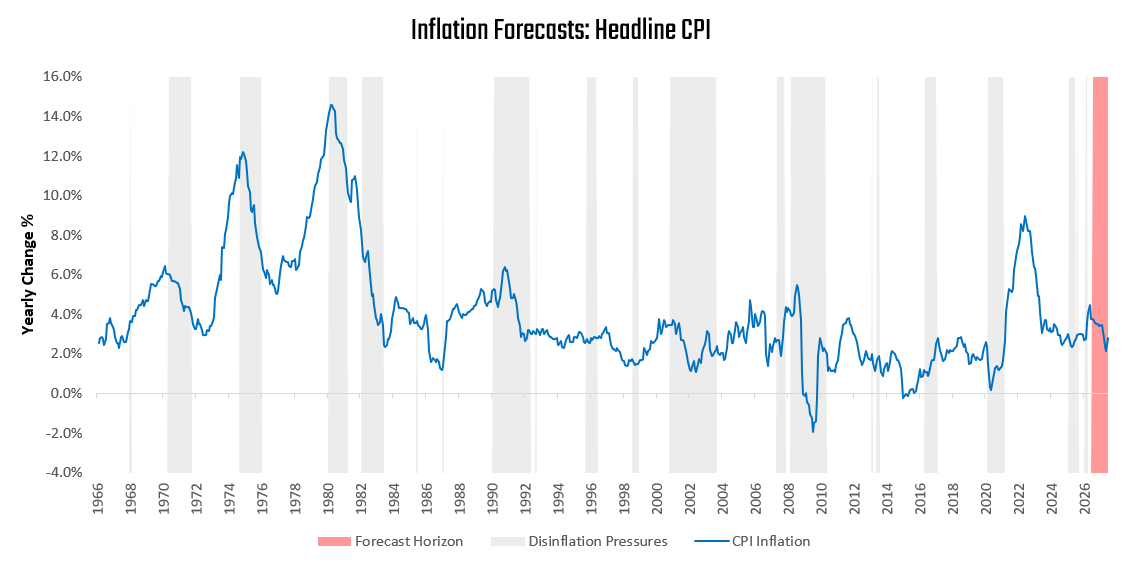

Thus, while this print is indeed a step in the right direction for the Federal Reserve, we think it’s important to recognize that one print is not indicative of the underlying pressures. Even if we extrapolate the current trend forward, we are still unlikely to see annual inflation rates consistent with the Fed’s 2% target. At the current trend, we would still be looking at an annual trailing inflation around 3% this year:

Therefore, as we review the data, we continue to see significant challenges ahead for the Fed, which we expect to be reflected in fixed income markets. Treasury markets remain secularly rich relative to nominal GDP conditions and, without a material repricing, will continue to whipsaw.

Read all the data driving our CPI assessment below:

Until next time.