Military confrontation continues in Iran, sustaining the global inflationary impulse through energy prices. This inflationary impulse has material effects for all asset prices. This inflation shock has caused much debate amongst the macro community about its implications for US Treasuries. We leverage our systematic process to offer some insight into how to navigate these conditions as a fixed-income investor. As usual, we’ve tested our reasoning over time to understand the range of possible outcomes better.

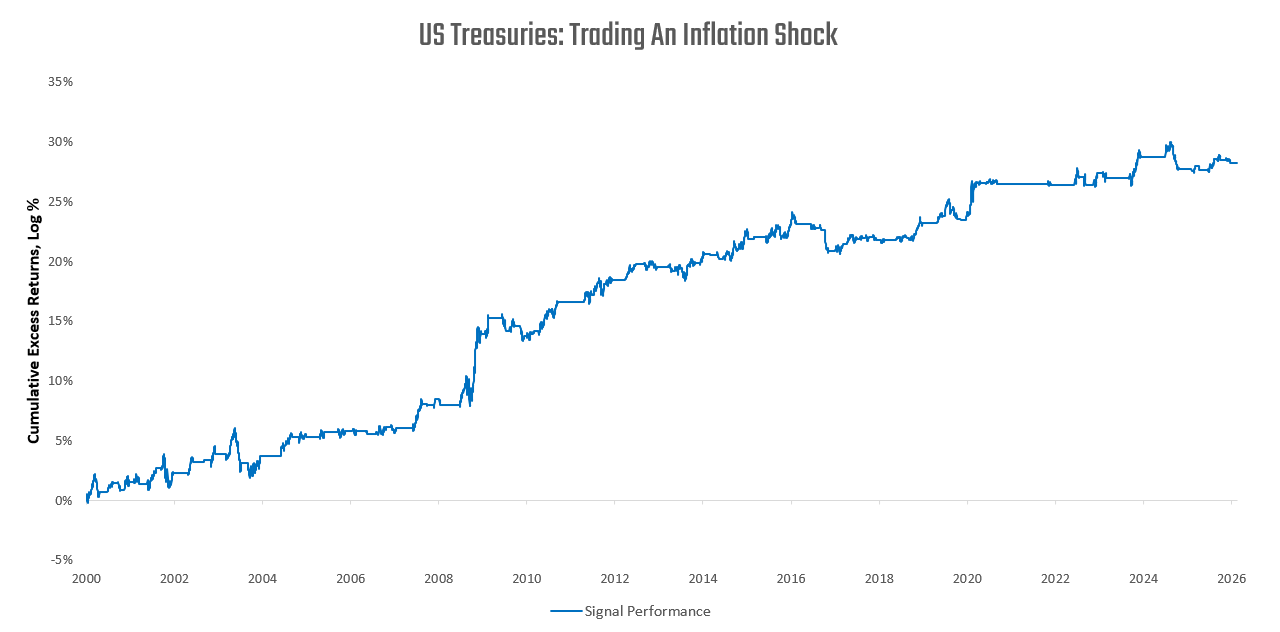

We visualize this below:

In this note, we discuss the principles driving the signal visualized above. We aim to provide a simple, actionable framework for thinking about Treasury exposure during this period of macroeconomic and geopolitical volatility.

The primary effect of the pressures in Iran has been surging energy prices across the oil complex. This surge in energy prices has two effects on the global economy and, in turn, Treasury markets:

Inflation Shock: Energy is a core input to every economy. Energy price shocks reverberate through an economy’s cost structure, and this is reflected in inflation calculations. These shifts in inflation rates are incremental pressure on central banks worldwide to hike policy rates. This incremental pressure is reflected in Treasuries through some mix of higher real rates, breakeven inflation, or policy expectations. Regardless of the composition of the yield changes, the inflation shock mechanically drives yields higher. The inflation shock is a headwind for Treasuries.

Demand Destruction: Inflation shocks are self-defeating. As prices spike relative to potential nominal demand, output begins to fall as real demand and output enter a downward spiral, nominal spending declines, and prices eventually fall to meet demand. The threshold at which this occurs is not knowable in advance, at least with systematic rigour; however, the signs of the turning point are apparent: deteriorating activity measures coupled with declining prices signal demand destruction and deflation. Demand destruction is a tailwind for Treasuries.

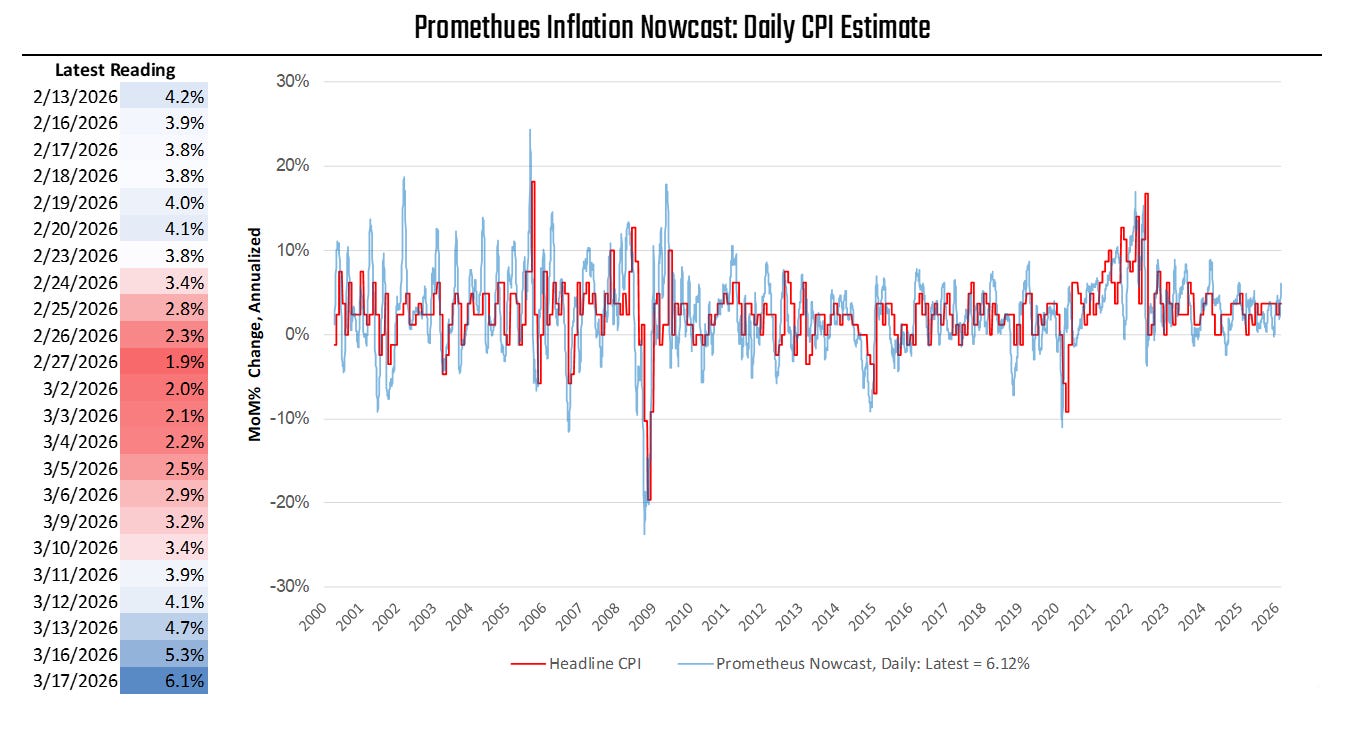

Today, market participants in fixed income are mixed on which outcome to position for: An Inflation Shock Or Demand Destruction? As quantitative systematic investors, our answer would be: Why not both, dynamically? We think our Inflation Nowcast can help us do so. As a refresher on our Inflation Nowcast:

As part of our systematic macro process, we track US CPI conditions promptly. Using market-based estimates, we can closely track the evolution of inflation pressures as reflected in the reported CPI. Our daily estimates for headline CPI closely track the official data, without the reporting delay inherent in official statistics. We find these measures particularly relevant for assessing ongoing pressures on fixed-income markets.

As noted previously, energy price spikes translate into inflation shocks that weigh on Treasuries. Our latest inflation nowcasts suggest material upward pressure on the CPI. Our latest readings suggest an annualized CPI rate of 6.1%, which is dramatically at odds with the Fed’s 2% inflation objective. Of course, we don’t expect year-over-year numbers to approach this pace, but it is nonetheless a sign of the times: we are in an inflation shock. This inflation shock will persist so long as the ongoing pace of inflation remains at odds with the Fed’s objective. Demand destruction will only take place once output contracts. Most importantly, demand destruction will be apparent as energy prices reverse, weighing on our timely CPI reads.

Combining the features of these dynamics, we expect our inflation nowcast to serve as a strong gauge of the market regime for Treasuries. The greater our latest readings exceed the Fed’s objective, the further we are into an inflation shock regime. The closer our gauges are to disinflationary or deflationary, the further we are into demand destruction. Furthermore, given our relatively short one-month window for calculating CPI, we will capture shifts in the energy components of CPI fairly quickly.

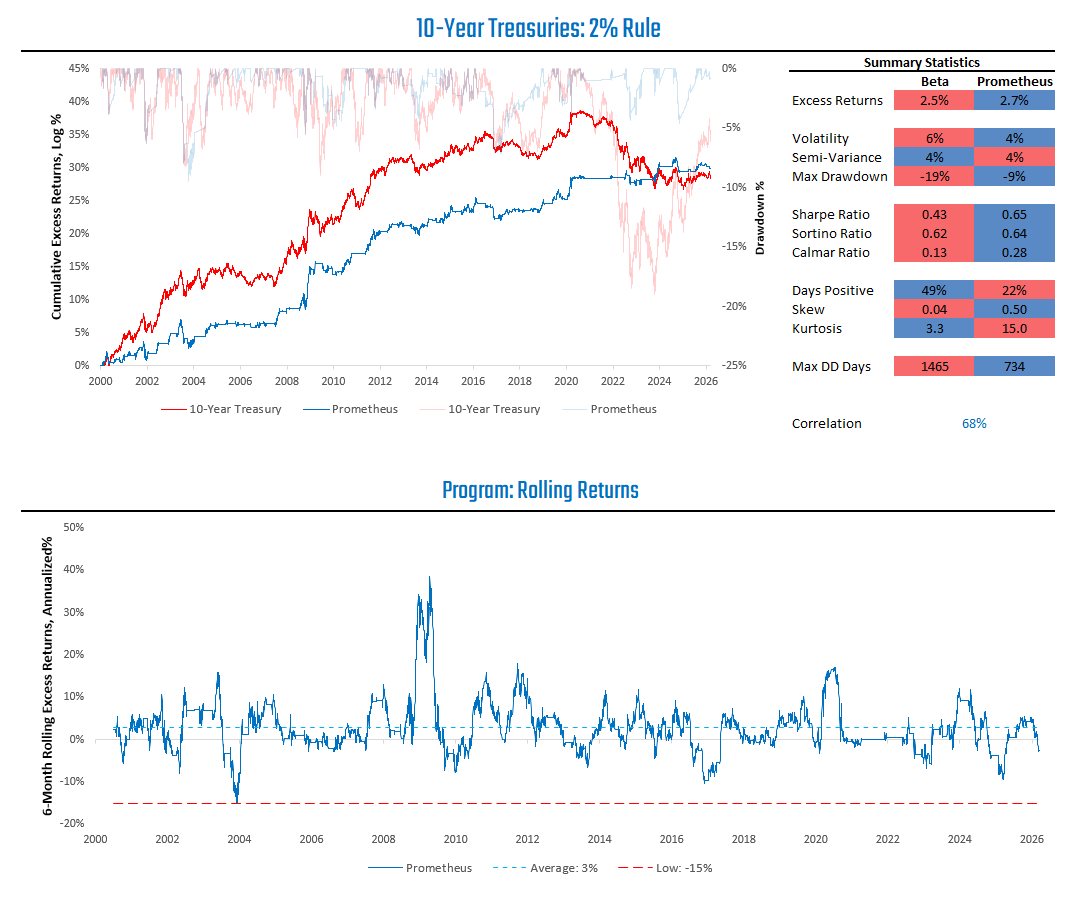

As such, we can construct a simple rule set for owning Treasuries: If our annualized CPI estimate is below 2%, we own fixed income. If not, we stay in cash. We’re not building a comprehensive trading system for treasuries using all the factors we track. Instead, we’re offering a simple, actionable roadmap for investors on how to think about their Treasury exposure during an inflation shock, which could lead to demand destruction. We show that the simulated performance of using the simple but defensible approach has been strong versus a buy-and-hold strategy:

We think that this approach, while simple, offers investors a clear guidepost to navigate treasury markets. Of course, the daily updates of our CPI Nowcast are available to Prometheus Institutional clients. However, we will also provide timely updates on this gauge here to help investors navigate these turbulent times.

Until next time.

This has high value for me right now. I hope you’ll continue to provide your CPI Nowcast updates.

How often do you update the annualized CPI estimate?

Also, strong is the prediction power of the estimate?