The Observatory

Opportunities Across The Treasury Curve

The Observatory is how we systematically track the evolution of financial markets and the US economy in real-time. Due to the strong demand for the product, we will start sharing the beta version of The Observatory (click to download) as we finalize its designs. This will offer a high-frequency resource to those using our systematic macro approach, allowing them to “Observe” the macroeconomy through our quantitative lenses. We will soon be launching the product officially, i.e., with explainer materials and a standardized format. And don’t worry, it’s all still free! Also, make sure to follow us on Twitter for timely updates:

Without further ado, let’s dive into what our systems are telling us:

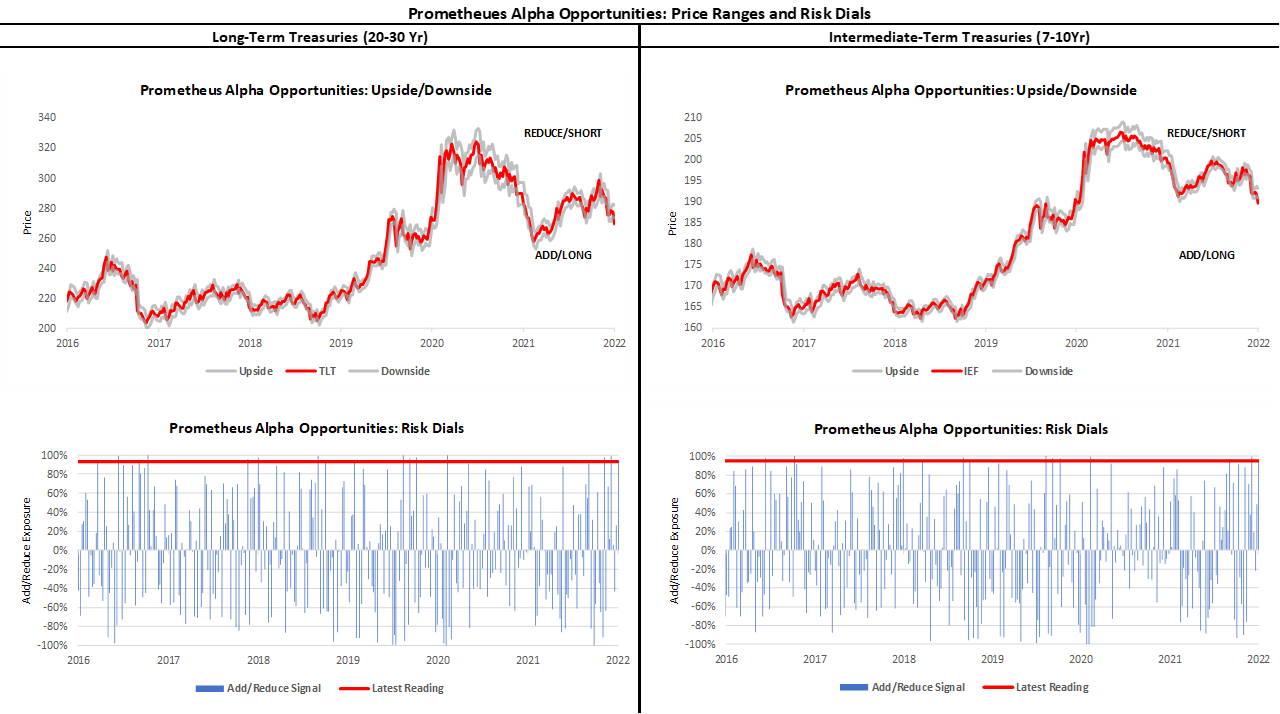

Markets: Markets continue to add strength to (+) G (+) I, with both equities and commodities showing strength yesterday. Treasuries continue to show lackluster performance. From a beta rotation perspective, this environment continues to favor commodity exposures, which continues to support our systematic preferences. From an alpha perspective, the strength of commodity moves in the recent past has been significant, triggering our systems to flag opportunities to reduce exposures. The aggressive nature of the current (+) G (+) I environment continues to hurt Treasuries; however, signals across the Treasury curve are moving in unison, telling us these moves are overdone.

To summarize our systems' current assessment: Our Market Regime Monitors show a dominance of (+) G (+) I extended. Our Momentum Monitors show rapid gains for Gold, with a Momentum Score of 83%. There is a rising possibility of markets beginning to price a (-) G (+) I, induced by extreme Commodity strength. Consequently, our expected return and risk analysis tell us that the best opportunities are Long: Bonds, Cotton, Lean Hogs, Cattle, Sugar, and Short: Communications. However, our Risk Management Monitors indicate that we can ADD to LONG: Bonds& Cotton. We can REDUCE our LONG: Lean Hogs, Live Cattle, & Sugar and SHORT: Communications. Our systems indicate the move in Treasuries, across the curve, is overdone. This selloff creates opportunities for our systems to add exposure. Resultantly, our Expected Return Strategy is LONG: Bonds & Lean Hogs.

Macro: This morning, CPI data came in sequentially stronger and above consensus. Further, it surprised our Inflation Nowcast to the upside as well. Our Inflation Nowcast considers a broader set of data than CPI; therefore, we expect them to again fall into step over the next few months. Today's CPI print will increase the pressure on the Federal Reserve to begin tightening liquidity provision, both via interest rates and balance sheet policy. This policy move will likely coincide with growth and inflation data starting to decelerate in March and April, respectively, creating a challenging market environment.

To summarize our systems' current assessment: Economic Momentum remains under the 50% mark, and our GDP Nowcast remains relatively unchanged this week. Our Inflation Nowcast provided a false signal for today's CPI print. However, this sequential acceleration potentiates future declaration, and our systematic Inflation Impulse forecasts have inflation turning decidedly lower in March-April. Sequential strength in US CPI was driven by food, transportation, household supplies, and shelter. Energy pressures abated.

The future is dynamic, and our systems adjust as new information is available. Our bias is to allocate for the existing regime while trying to peek around the corner to what the future may hold. Finally, we optimize these views to minimize portfolio risk, resulting in our trading signals. We show all this in the document below.

Click here to enter The Observatory.

hi all love the work, curious if your making this platform more broad or interactive, would love to know how somehting like iwm fits in these regimes along with growth tech like arkk thanks