The Prometheus S&P 500 Program aims to outperform the S&P 500 over a full investment cycle. The program will aim to achieve this objective by leveraging a combination of Sector Selection, Beta Timing, Active Overlays, and Dynamic Risk Control.

You can read the 27-page primer detailing the mechanics of our approach below:

We started Prometheus with a simple premise: bring the highest quality of institutional-grade macro investment research to everyday investors. Today, we are taking another big step in this direction with the official launch of our systematic Prometheus S&P 500 Program.

Prometheus S&P 500 Program Primer

We started Prometheus with a simple premise: bring the highest quality of institutional-grade macro investment research to everyday investors. Today, we are taking another big step in this direction with the official launch of our systematic Prometheus S&P 500 Program.

For reference, we visualize the simulated path of the program below:

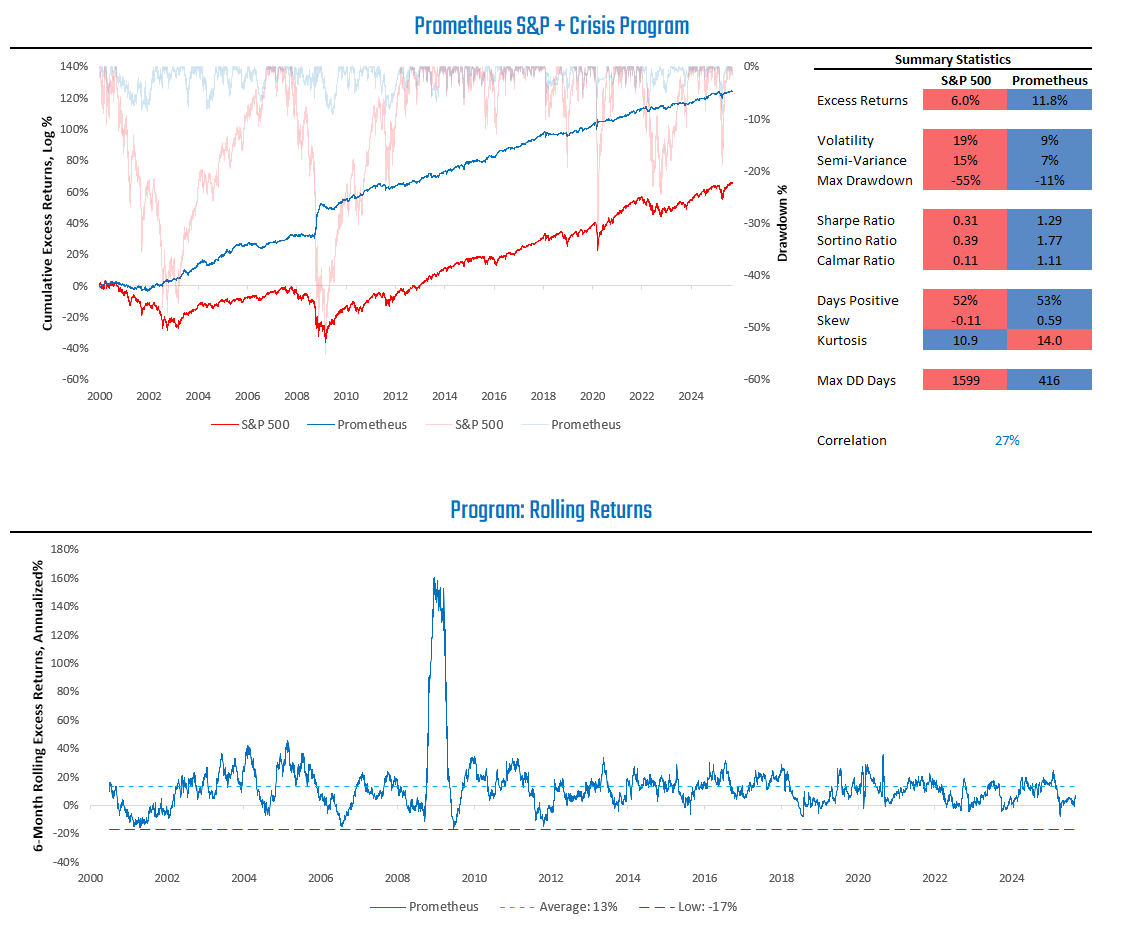

Today, this program continues to control the equity market drawdown using risk control measures. While the S&P 500 experienced a drawdown of 20% during the 2025 correction, the Prometheus S&P 500 Program never exceeded a 10% drawdown. Further, the program has maintained upside capture while maintaining these improved drawdown characteristics. This is consistent with the portfolio’s objectives, i.e., maintaining upside exposure to equities while reducing or avoiding drawdowns.

Our programs continued to maintain modest long exposure to equities, which remains consistent with the direction of the business cycle. Crisis protection continues to offer an attractive return to risk amidst a period of elevated valuations.

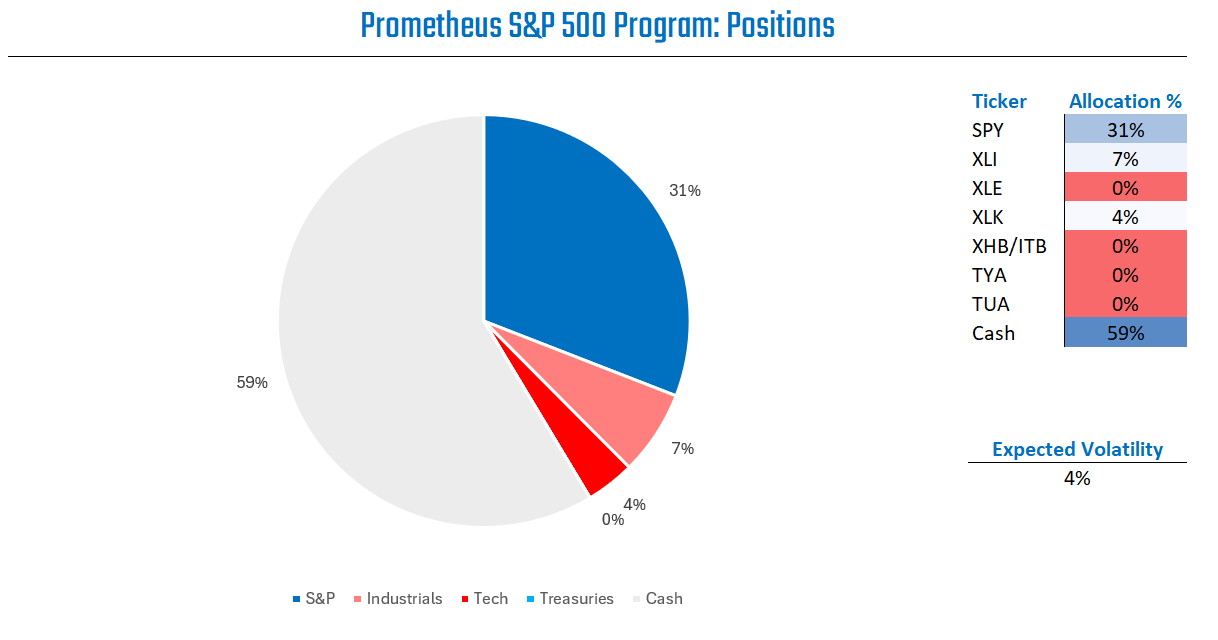

Today, the S&P 500 Program is positioned as follows:

Our systems are now long stocks, with an elevated amount of cash. There are four major takeaways from these positions:

Beta Timing: Our beta timing shows modest signal strength at this junction. Equity markets remain supported by strong trends.

Sector Selection: Within the cross-section of equity sectors, our signals favor a mix of industrial and technology stocks. Our positioning remains skewed towards industrials due to better relative valuations.

Risk Control: Our risk control has guided us well through this most recent bout of equity volatility, maintaining our drawdown at less than half that of the S&P 500 during the sell-off while also maintaining upside exposure as equity markets climb to all-time highs. In a multi-standard deviation event across all our positions, our expected drawdown is 3%.

Bond Overlay: Our systems continue to see bonds as expensive in an environment where the economy remains resilient. Bonds offer little by way of excess returns relative to cash and look unattractive without a material weakening of the economy, which continues to look improbable.

Our systems combine these dimensions to create one comprehensive outlook reflected in our portfolio positions.

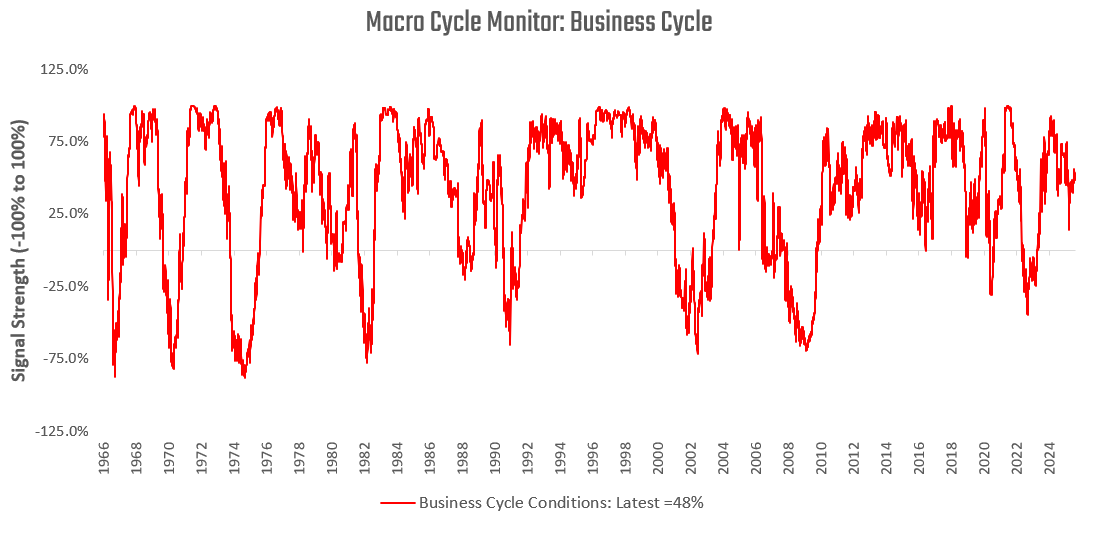

Our latest tracking of economic growth indicates that the business cycle is slowing modestly, but remains in an expansionary phase. We show these proprietary tradable signals below:

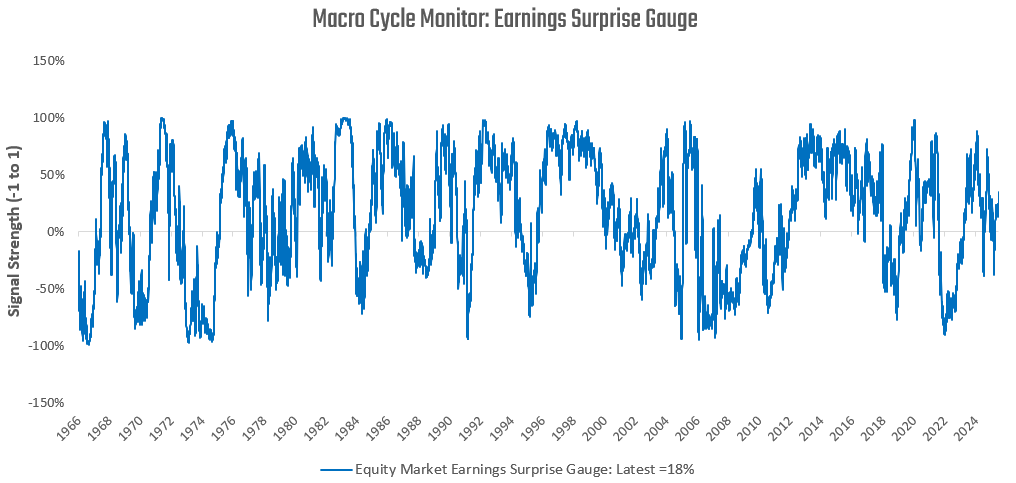

These business cycle conditions continue to support the prospects for positive earnings growth relative to expectations.

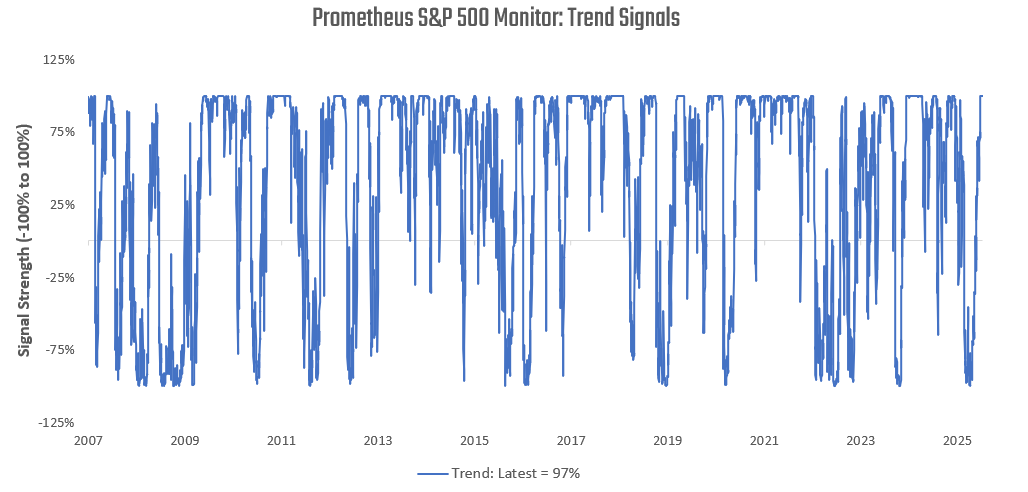

These conditions have been in place over the last few months and remain so. Furthermore, these conditions remain supported by extremely strong trend readings:

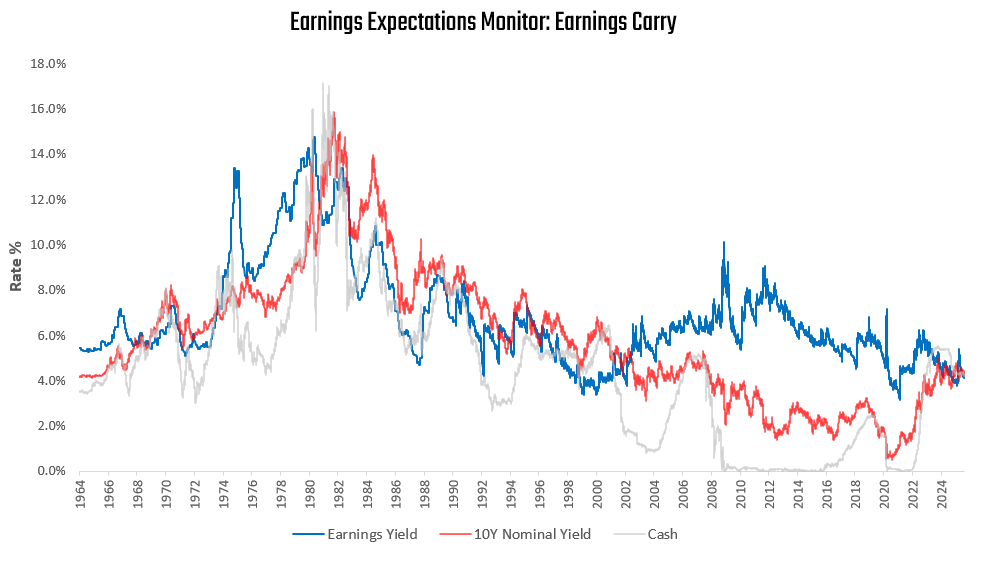

Despite these positive dynamics, expected returns for equity markets remain compressed versus other assets. Recall, today, cash offers essentially the same expected returns as stocks and bonds, with none of the risk:

Given these compressed expected returns across equities and bonds, and the modest convictions coming from our market timing signals, we can use our Crisis Protection Program as an overlay.

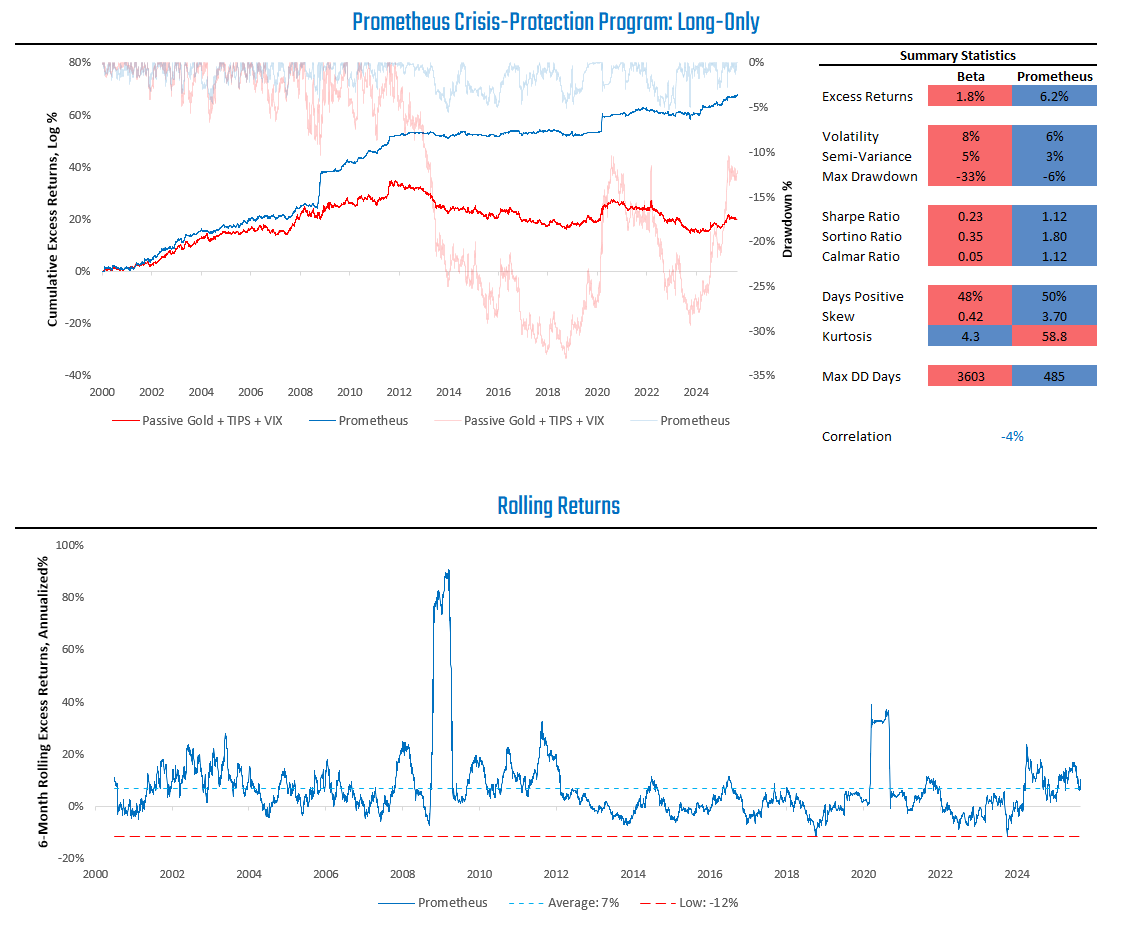

The Prometheus Crisis Protection program seeks to offer a portfolio diversifier during periods of economic and financial instability by blending active exposure to Gold, TIPS, and VIX. Actively managing these exposures is integral, as their expected returns are time varying with the macro cycle. We demonstrate how actively managing these exposures can add significant value compared to holding them passively:

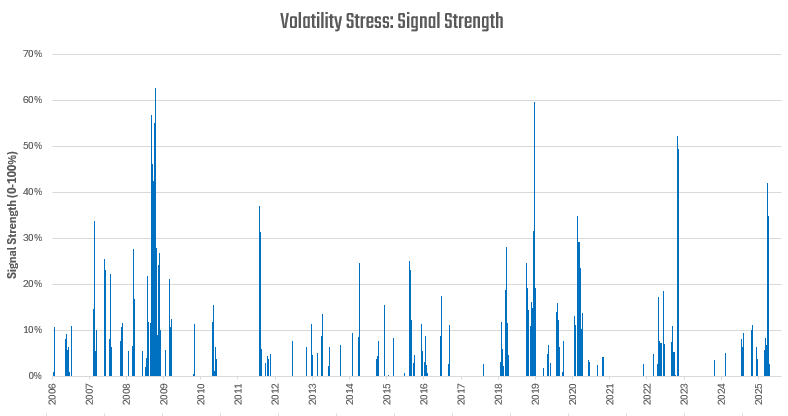

The most crucial part of this program is its correlation to equity markets. During equity market down days, this program has a mean Sharpe Ratio of 2, suggesting strong diversification characteristics to beta. Today, these programs do not see signs of elevated financial stress, which we capture in the form of our Volatility Stress guage:

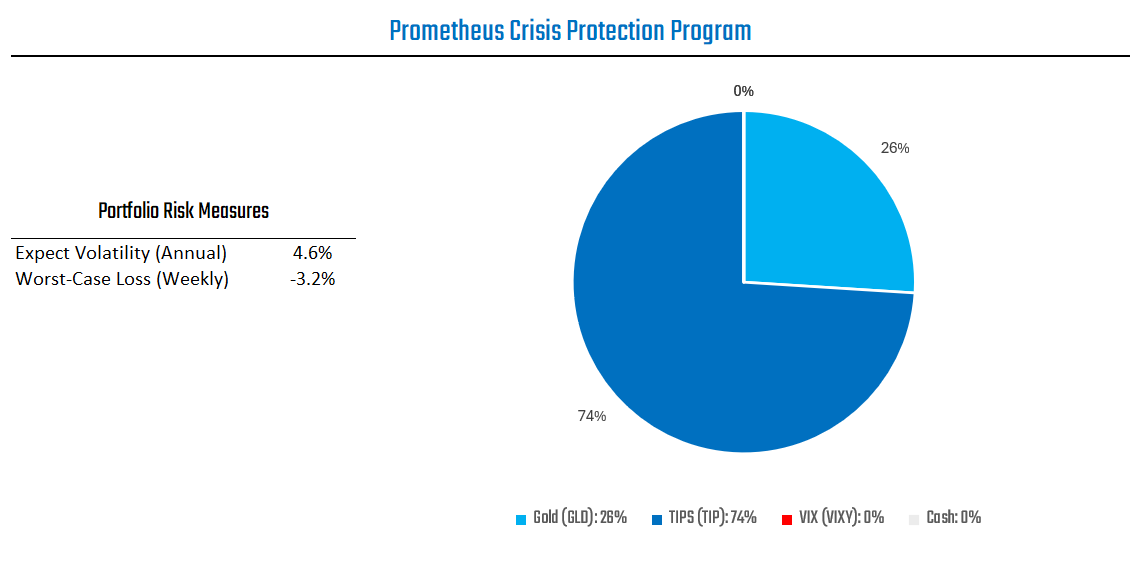

Nonetheless, gold and TIPS offer attractive expected returns during periods of elevated nominal GDP, easy monetary conditions, and above target inflation. As such, the Prometheus Crisis Protection Program is allocated as follows:

The Crisis Protection Program currently has an expected volatility of 4.6%, with a maximum of 10%. In an outlier event, our estimate for a worst-case loss at the portfolio level over the next week is -3.2%.

Integrating our S&P 500 and Crisis Protection programs offers an attractive and highly diversified portfolio. We visualize the simulated path of this portfolio below:

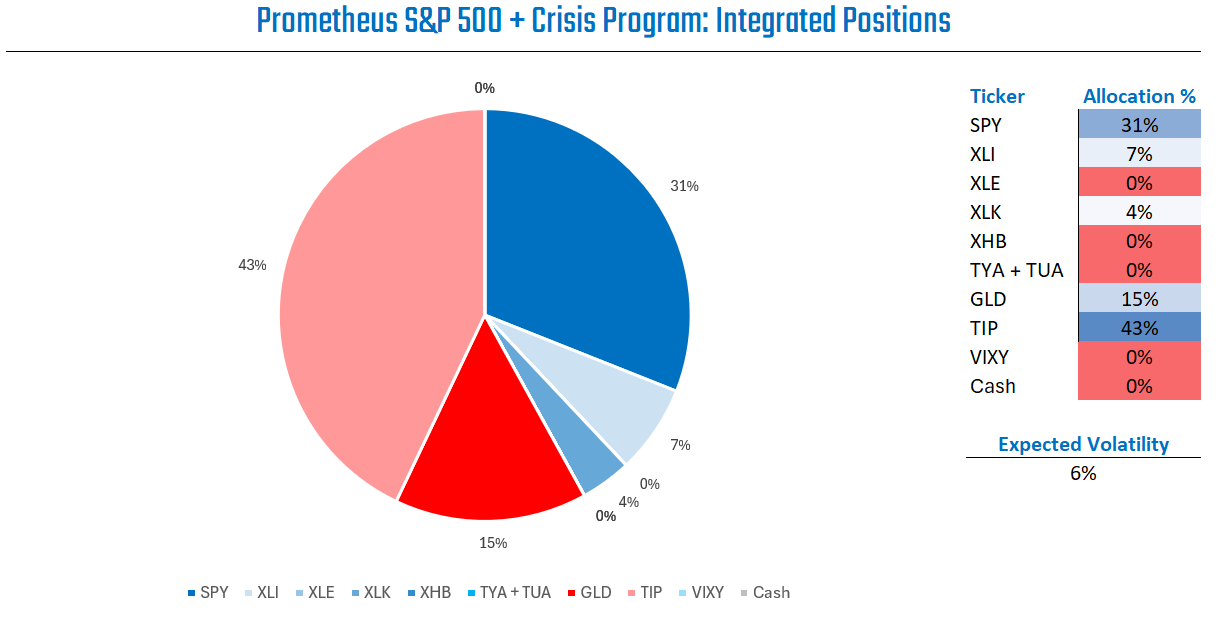

Today, this portfolio is allocated as follows:

The business cycle remains in an expansion, and while there might not be significant alpha in owning equities here, owning beta during an economic expansion is profitable over time. Given the low levels of expected returns in treasuries and bonds, an allocation to crisis protection assets will likely offer carry and diversifying characteristics.

The future is dynamic, and our systems will adapt as the data evolves. We will keep you updated as the outlook shifts. Until next time.

One question on the crisis protection program (but I think it also true for the S&P 500 program too), how do you evaluate that the program is not overfitting the historical data especially when it comes to rare occurrences like a crisis?

Looking good!