The Prometheus S&P 500 Program aims to outperform the S&P 500 over a full investment cycle. The program will strive to achieve this objective by leveraging a combination of Sector Selection, Beta Timing, Active Overlays, and Dynamic Risk Control. Our S&P 500 Program can be integrated with our Crisis Protection Program, which seeks to offer a portfolio diversifier during periods of economic and financial instability by blending active, long-only exposure to Gold, TIPS, and VIX.

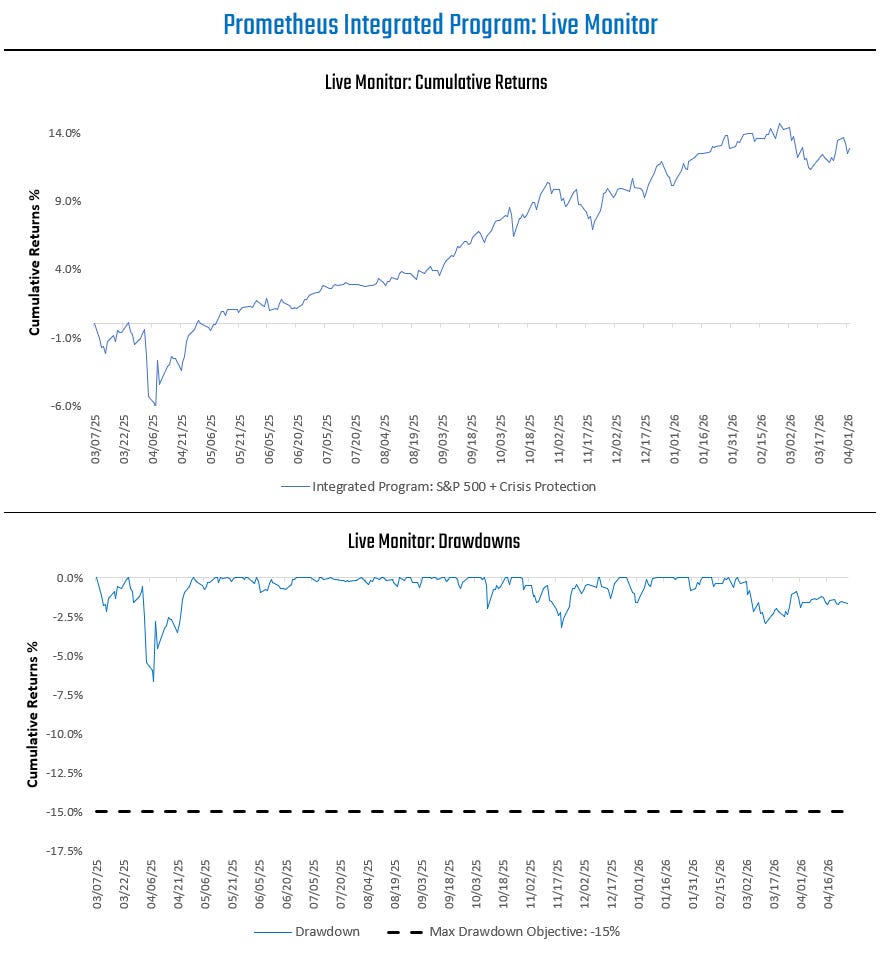

For context, we visualize the live returns for our Integrated Program below:

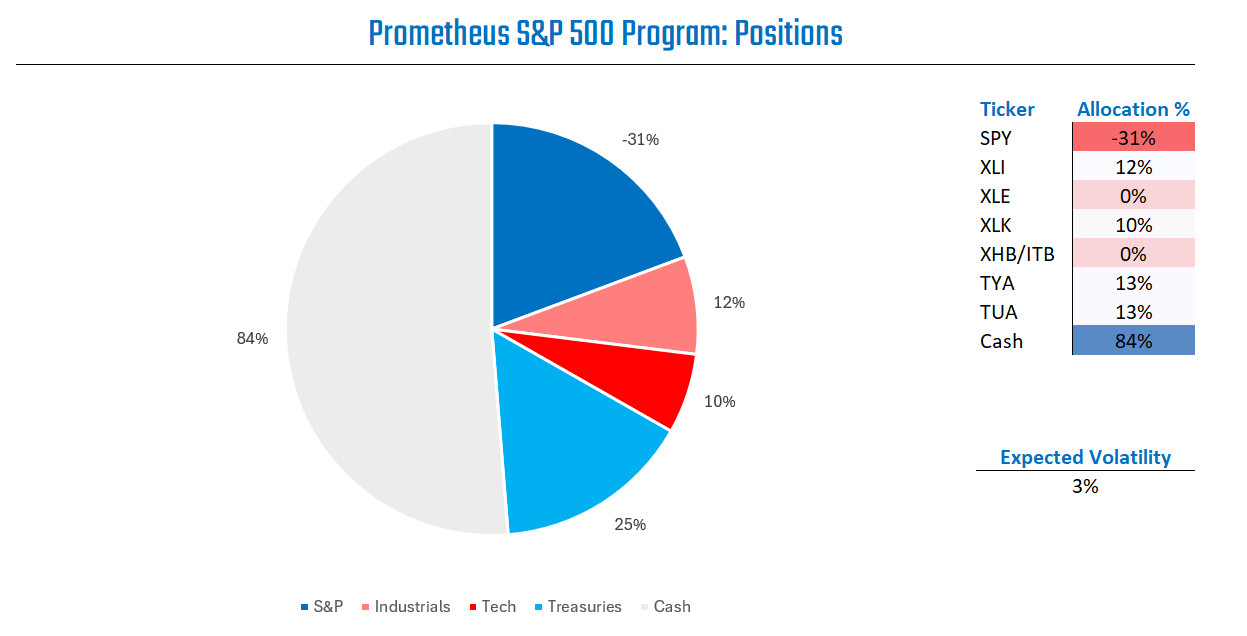

Our programs are operating in line with their long-term expectations. Today, the S&P 500 Program is positioned as follows:

There are four major takeaways from these positions:

Beta Timing: Our beta timing measures continue to show downward pressure on equity indexes from locally expensive equities, which may have rallied too dramatically.

Sector Selection: Macro markets are experiencing a sustained inflation shock, which will change the distribution of sector returns. Across the equity sectors, our signals favor technology and industrials.

Risk Control: Our risk control continues to guide us effectively in managing drawdowns. In a multi-standard deviation event across all our positions, our expected drawdown is 8%.

Bond Overlay: While we face an ongoing inflation shock in market pricing, fundamental conditions are beginning to align more with a weakening growth backdrop. This weakness of growth, coupled with a modestly positive yield curve, makes treasuries and amenable exposure within a portfolio. This positioning is primarily about carry and diversification during a growth slowdown, rather than an outright alpha view.

To this allocation, we add our Crisis Protection Program. The Prometheus Crisis Protection Program is allocated as follows: