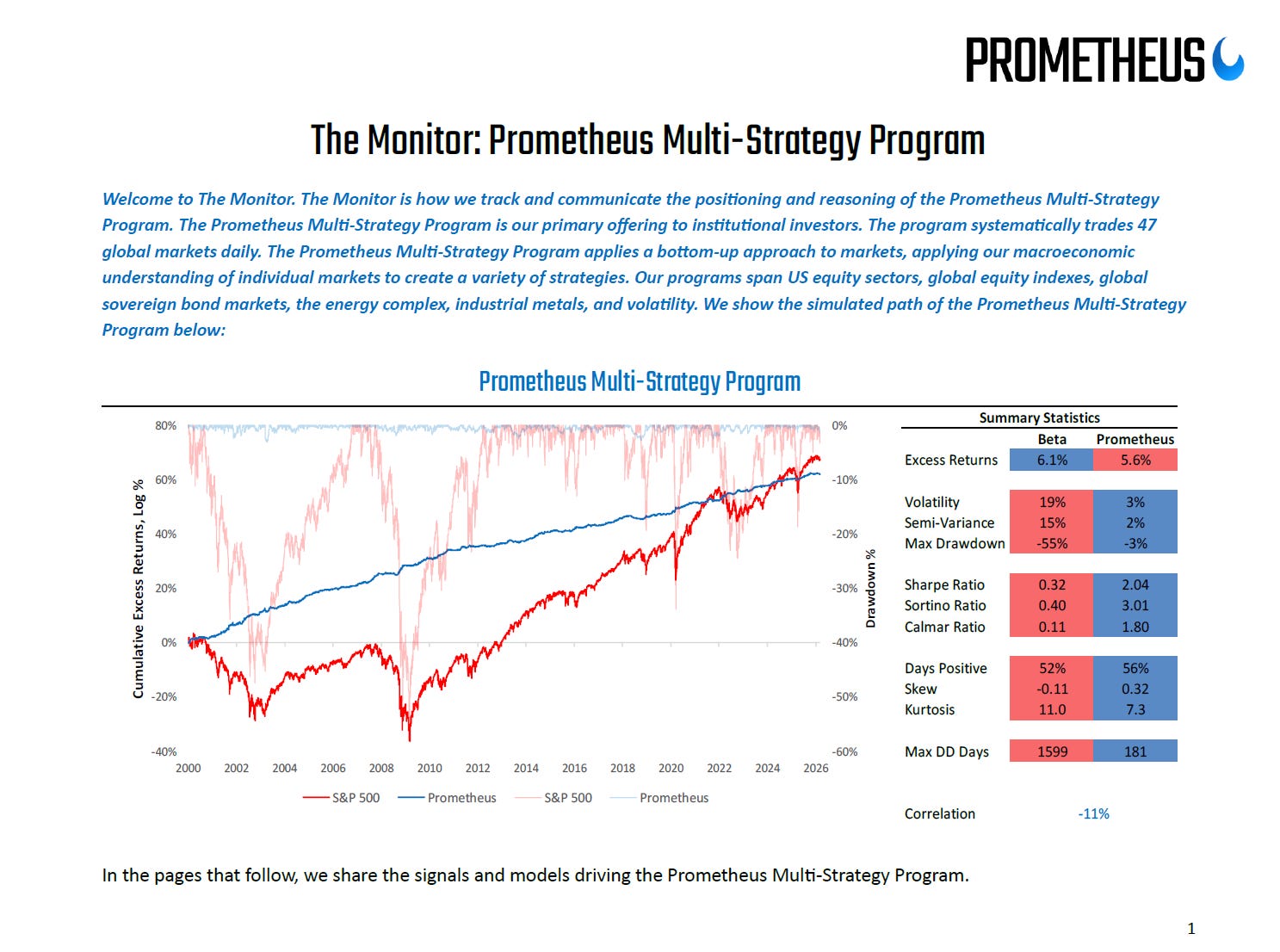

The Prometheus Multi-Strategy Program is our primary offering to institutional investors. The Monitor is how we track and communicate the positioning and reasoning of the Prometheus Multi-Strategy Program. The program systematically trades in 47 global markets daily.

To complement our existing offering for individual investors, we offer excerpts and insights from The Monitor. If you are a professional investor and would like access to our real-time signals and analysis, email us at info@prometheus-research.com for more information.

Our observations are as follows:

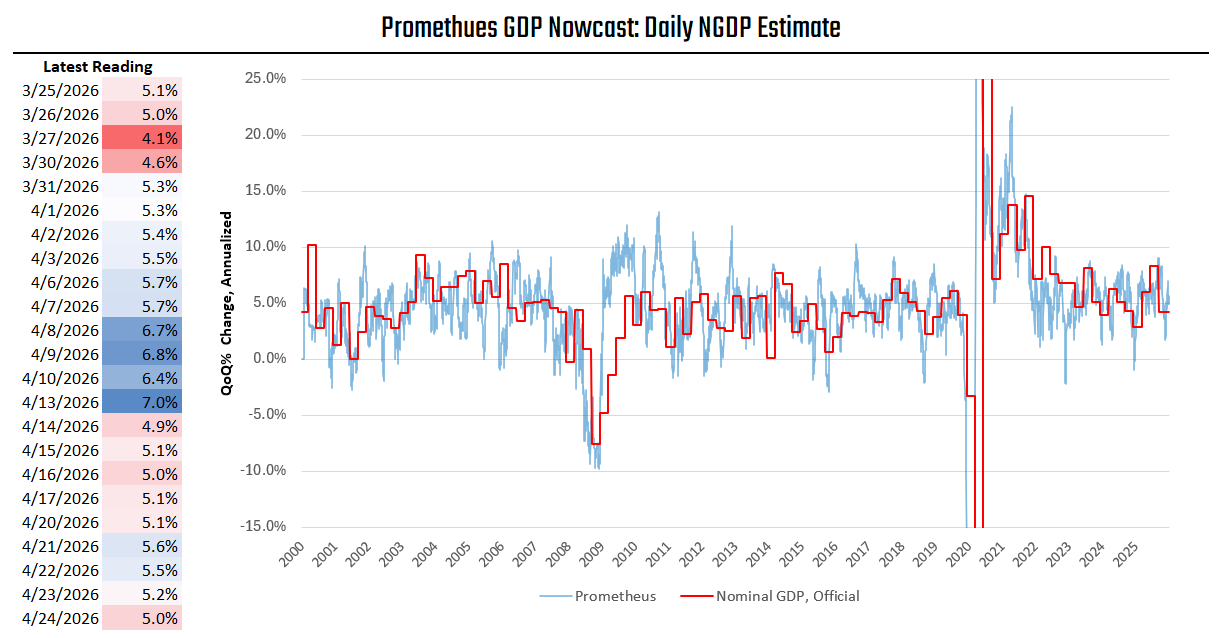

The latest readings across our gauges of economic activity continue to suggest an extremely strong nominal growth backdrop.

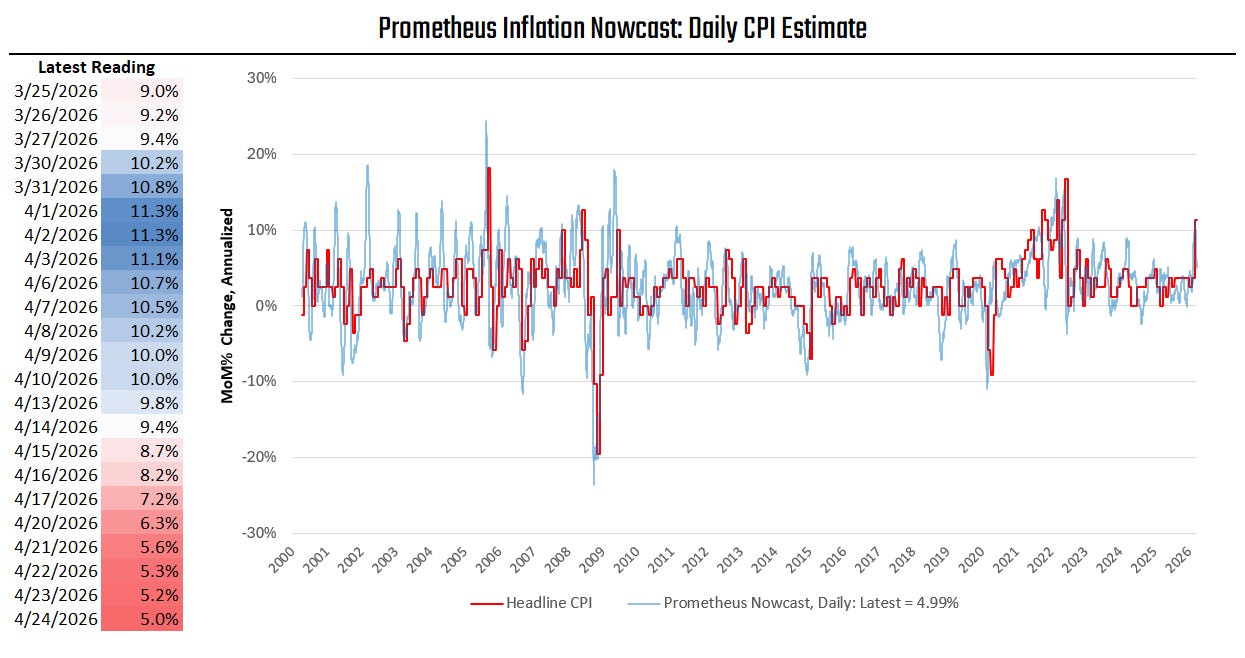

The inflation shock to the CPI remains elevated, and the rate of change remains downward.

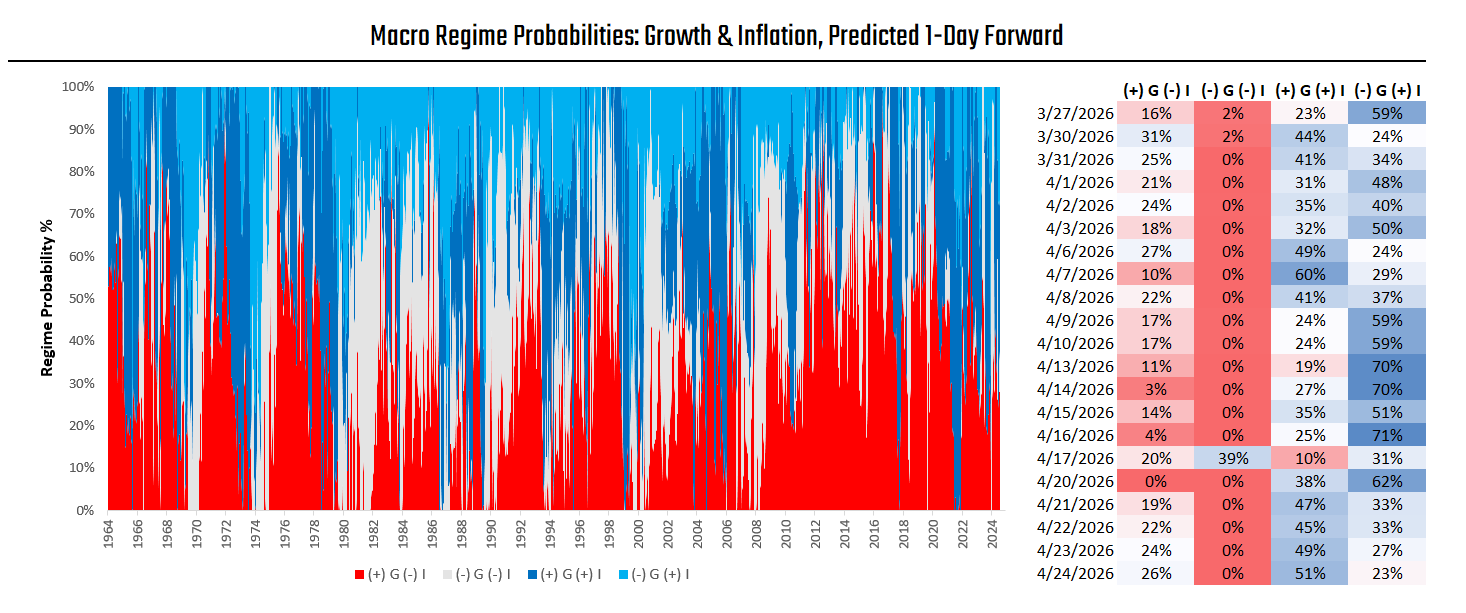

Our macro market regime probabilities are back to favoring inflationary regimes— now with a rising growth bias.

Amid this backdrop, the Prometheus Multi-Strategy Program is now running with a much more neutral risk profile across assets—seeking to catch a rally in US fixed income while maintaining a more neutral bias across global asset markets. This portfolio exposure is technical rather than fundamental, and the positions may unwind quickly. While the Prometheus Multi-Strategy Program is not actively deploying significant risk right now, our process shows evolving opportunities in the commodity landscape. We scan through our macro monitors before diving into this thread.

We show that our timely NGDP readings have remained stable through April:

While our CPI estimates continue to decelerate from their recent peak:

Further, we show how our forward-looking market regime probabilities have shown a transition back to inflationary conditions:

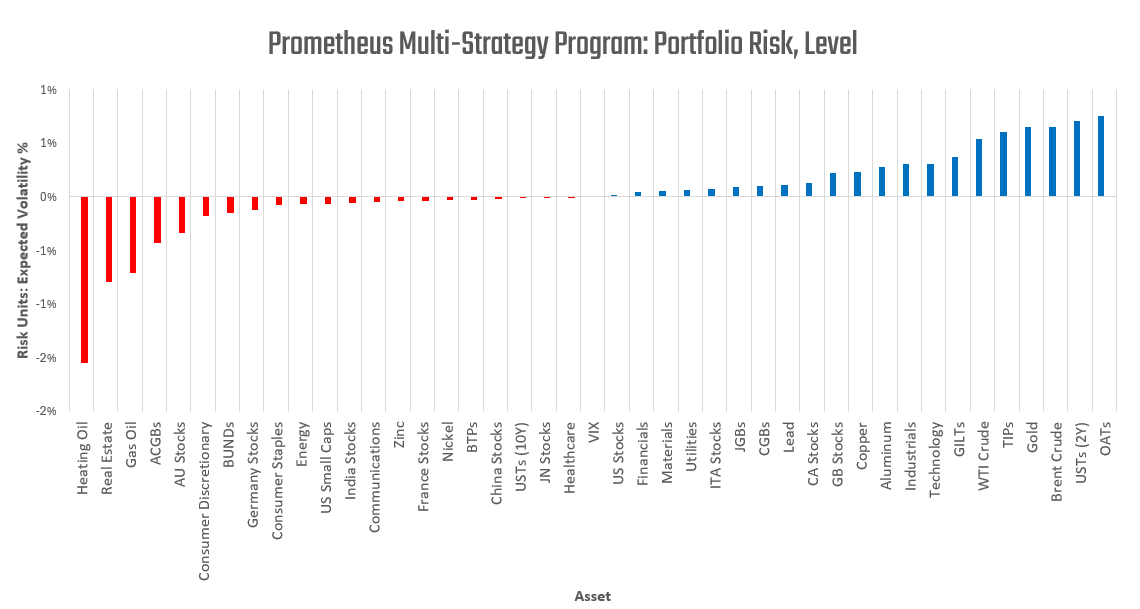

Despite these inflationary-regime expectations, the Prometheus Multi-Strategy Program remains cautious due to regime volatility and potential instability. We show the current positioning of the Prometheus Multi-Strategy Program below:

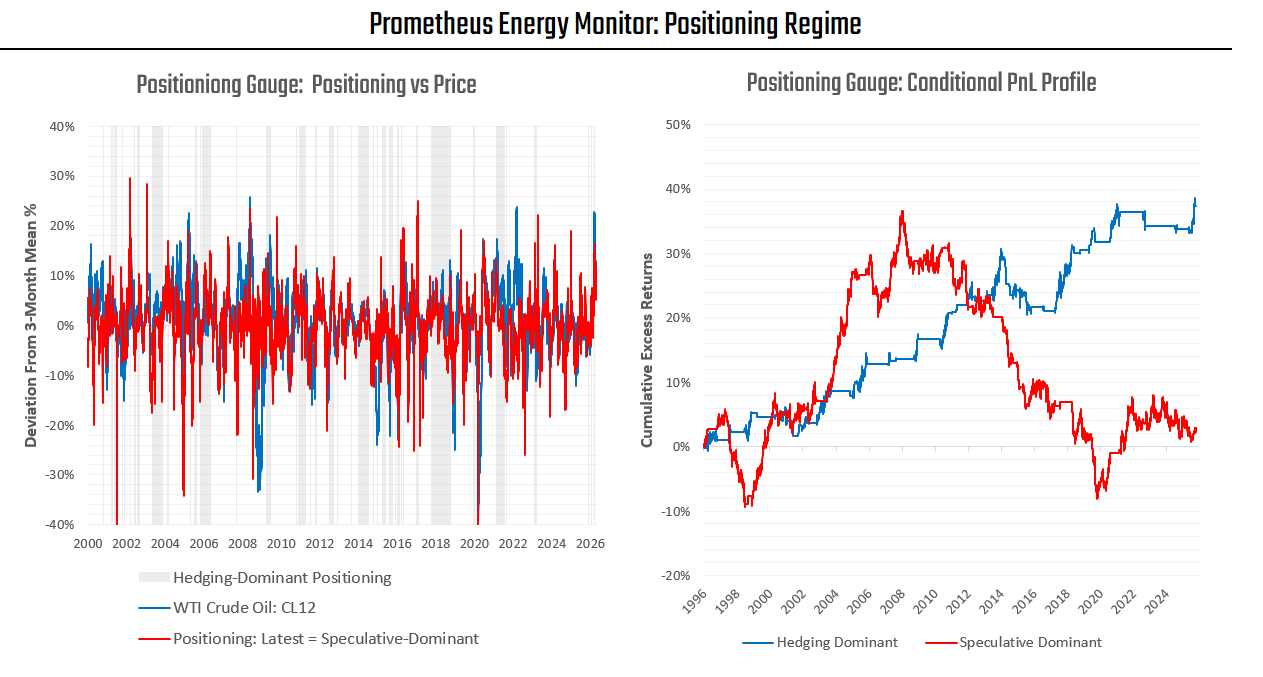

While Prometheus Multi-Strategy is not currently deploying material directional risk exposure, we see two avenues for future signal strength. First, we see a positive backdrop for the oil complex, particularly for back-dated contracts. While our short-term signals for the energy complex have turned neutral since April 8, we are starting to see some shifts in the dynamics underlying price action— becoming more conducive to oil beta. Principally, energy markets are composed of two participants: speculators and hedgers. Speculators seek financial gain through their exposure to commodity futures. Hedgers, on the other hand, seek insurance against future revenue volatility. While hedgers seek to minimize hedging costs, they are not profit-seeking in futures markets. This relative near-term price-insensitivity makes their flow mechanical and more consistent in markets. As such, hedgers are a countercyclical force in markets— pushing down prices relative to their fair value as commodities rise due to shortages. This creates a conducive backdrop for owning energy futures beta. Below, we show how our positioning regime monitor allows us to classify periods into those where speculators are dominant versus those where hedgers are dominant:

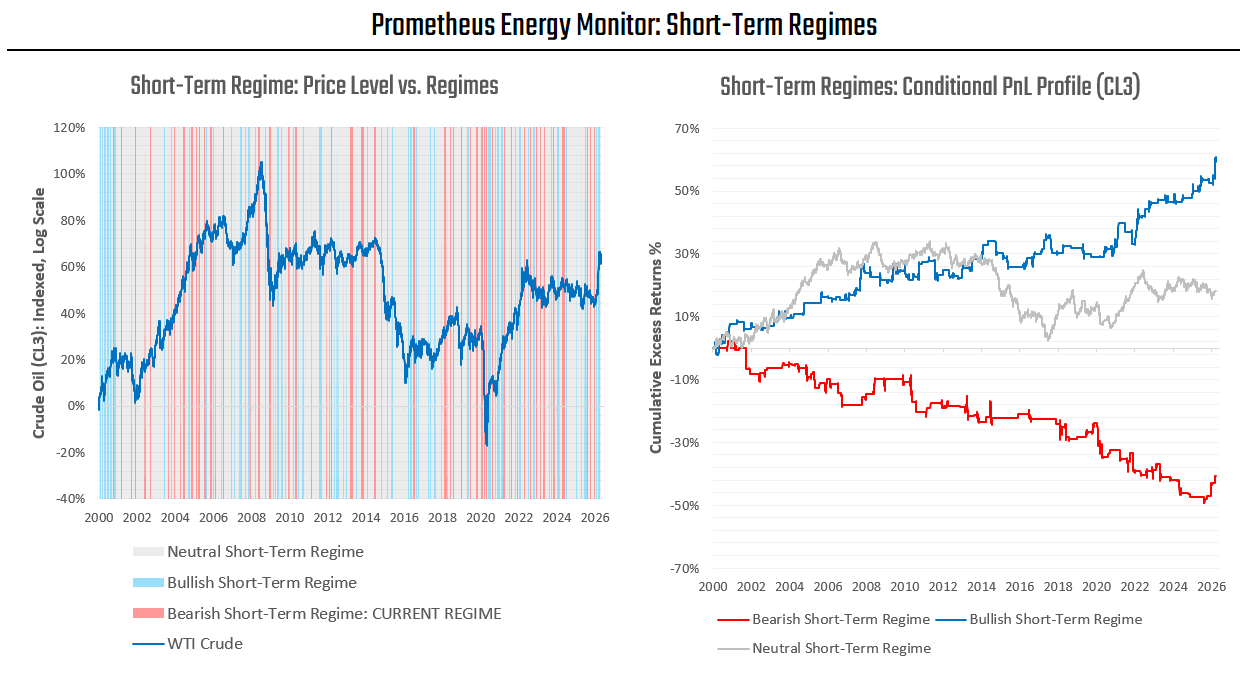

While our systematic classification still shows a speculative-dominant market, the numbers under the hood are quite evenly matched; i.e., there is a large hedging presence in markets today as well. Further, we see potential for us to transition into a hedging-dominant market as speculators unwind their positions. While not an optimal backdrop for the energy complex, it is nonetheless a positive one. However, our short-term signals for oil continue to show pressure on spot prices:

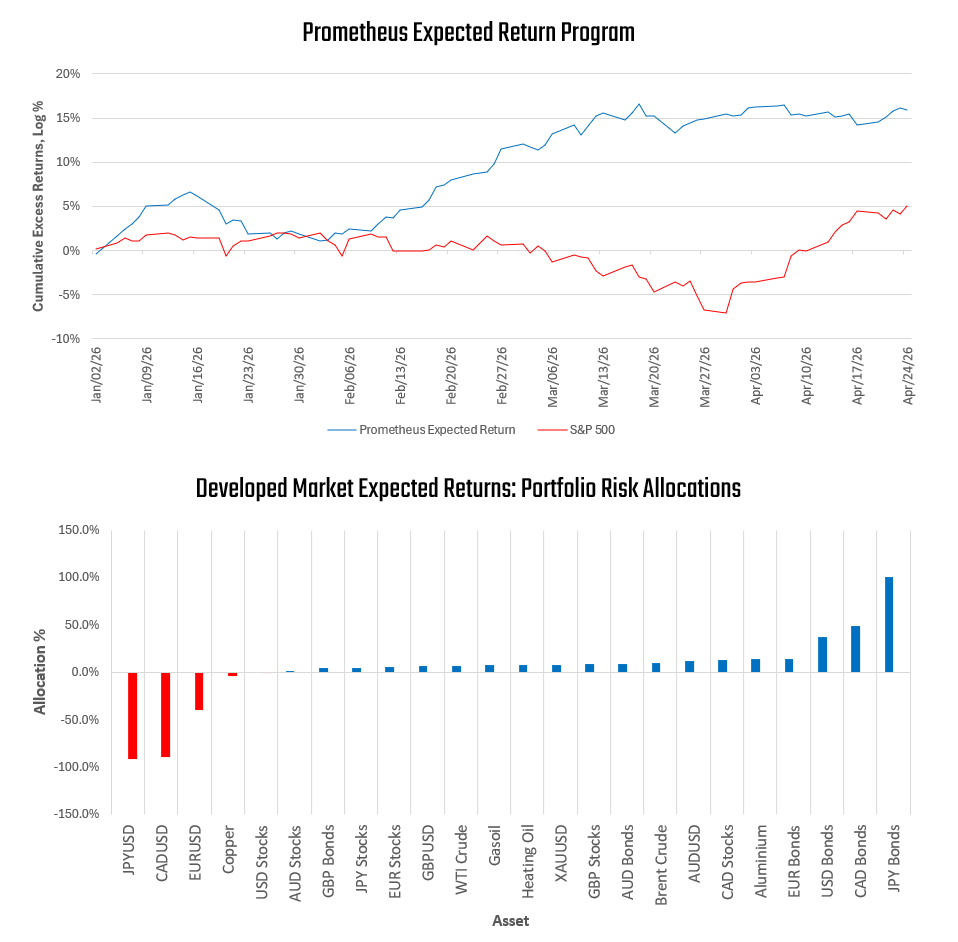

As such, the best expression for long energy exposures, which we continue to believe tactically necessary in this backdrop, is via back-dated contracts (6 months and further). The Prometheus Expected Return Program has benefited from these exact types of exposures year-to-date:

Tactical exposure to energy, with strong risk management, remains the best way to protect and compound portfolios during this regime. The latest developments indicate that the opportunities have shifted from the front of the curve to the back.

Until next time.