At Prometheus, we are committed to equipping our clients with the most granular, high-frequency, and actionable read of macro conditions in the industry — translated, every day, into systematic signals across global markets. Prometheus Institutional gives our clients access to our tracking of fundamental conditions via The Observatory, daily updates to our Macro Regime Probabilities, our signal-based views on global markets from The Monitor, and machine-readable signals from the Prometheus Multi-Strategy Program.

For a deeper overview of Prometheus Institutional, read the link below:

Prometheus Institutional

Prometheus is built on deep fundamental research into how the economy works. We have built a rigorous, systematic process for tracking virtually every major data point released in the US economy. That tracking of economic conditions is coupled with a study of macro markets and investment strategies over hundreds of years and dozens of countries, to crea…

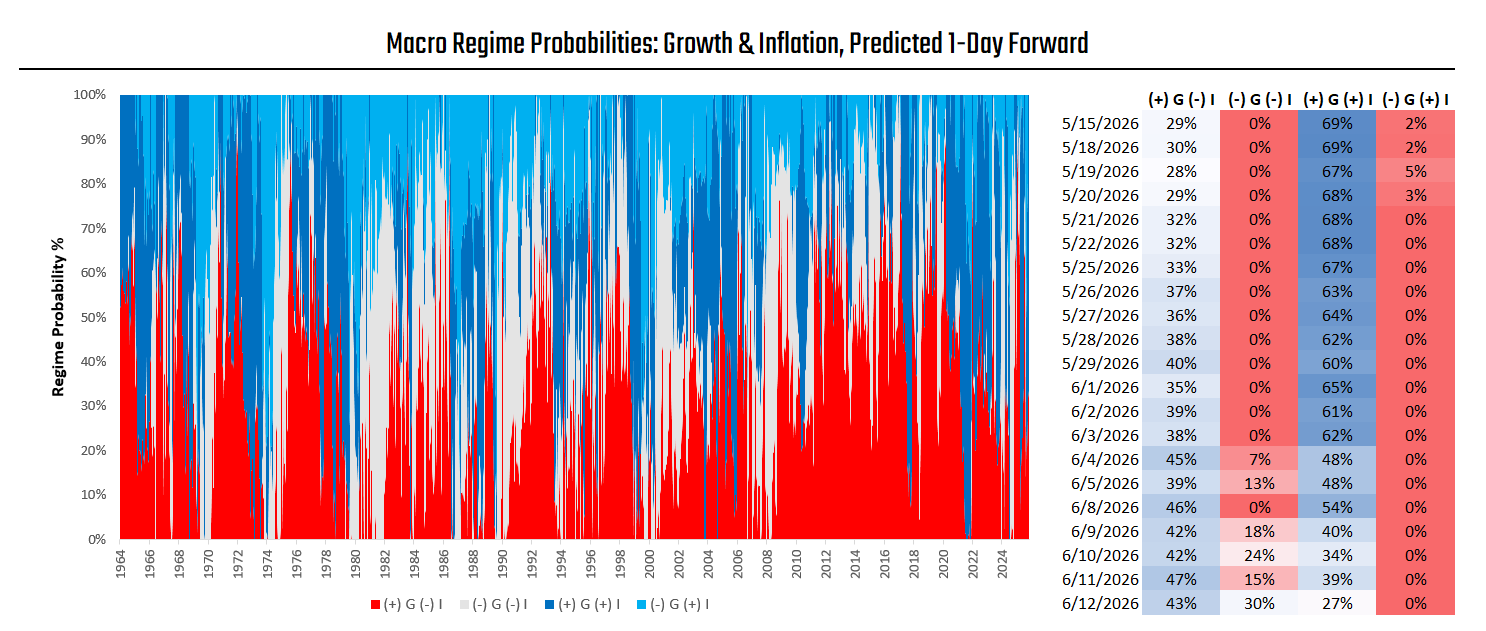

Every day at midday, we share updates to our US Macro Regime Probabilities with Prometheus Institutional, along with our synthesis of what the current regime probabilities suggest.

Our Macro Regime Probabilities use our bottom-up signals across asset markets to construct forward-looking estimates for the cross-asset macro market regime. These signals incorporate both fundamental and price-based information to produce high-frequency, forward-looking estimates for the US cross-asset environment. These signals are best used as a forward-looking guide for the cross-sectional returns across macroeconomic assets. We define the regimes as follows:

(+) G (-) I: Rising Growth & Falling Inflation, Equities Outperform

(+) G (+) I: Rising Growth & Rising Inflation, Commodities Outperform

(-) G (-) I: Falling Growth & Falling Inflation, Treasuries Outperform

(-) G (+) I: Falling Growth & Rising Inflation, TIPs Outperform

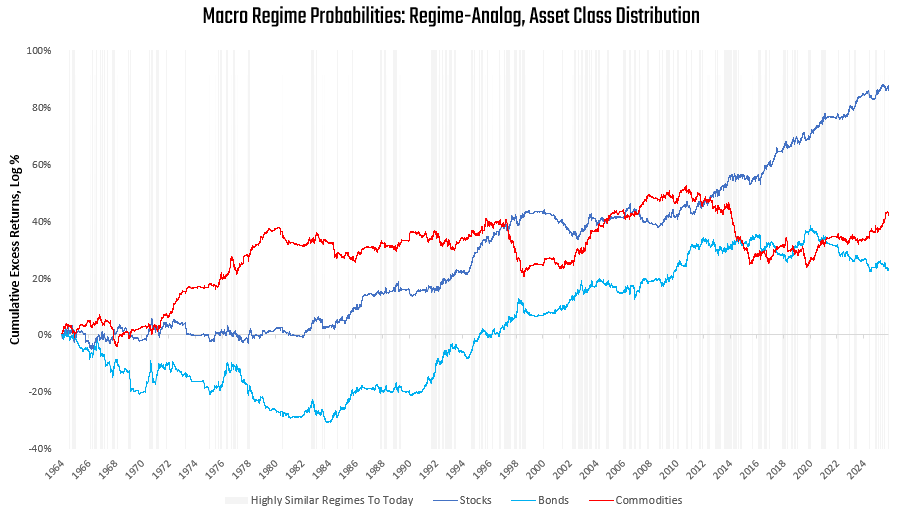

Synthesis: Our Macro Regime Probabilities have shifted to reflect a higher probability of disinflationary cross-asset market outcomes. This shift materially reduces near-term pressure on fixed-income markets and moderates the potential strength of commodities. Crucially, this change further boosts the expected returns for equities by reducing the downside pressure on rate expectations. We visualize the expected returns for assets scaled by regime similarity over time below:

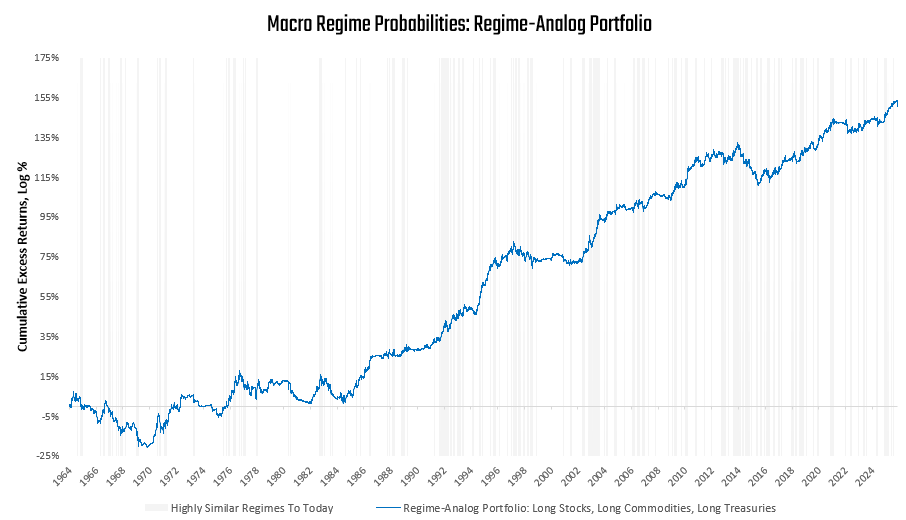

This regime mix favors being long stocks, bonds, and commodities—i.e., the preference for fixed-income shorts is removed. We show the expected returns for this portfolio scaled by regime similarity over time below:

We remain cautious on treasury exposure. While regime conditions are now more supportive, we think it is essential to recognize that these are potentially transient, market-action-driven shifts rather than a material change in fundamentals that will drive the Fed’s calculus. Pressure being lifted from breakeven pricing is not the same as pressure being lifted from the Fed; the latter is a far more durable signal for fixed income. Thus, we see this increase in disinflationary probabilities as more supportive of equities than fixed income.

Until next time.

>Pressure being lifted from breakeven pricing is not the same as pressure being lifted from the Fed

Is this because growth is offsetting the disinflation pressure?