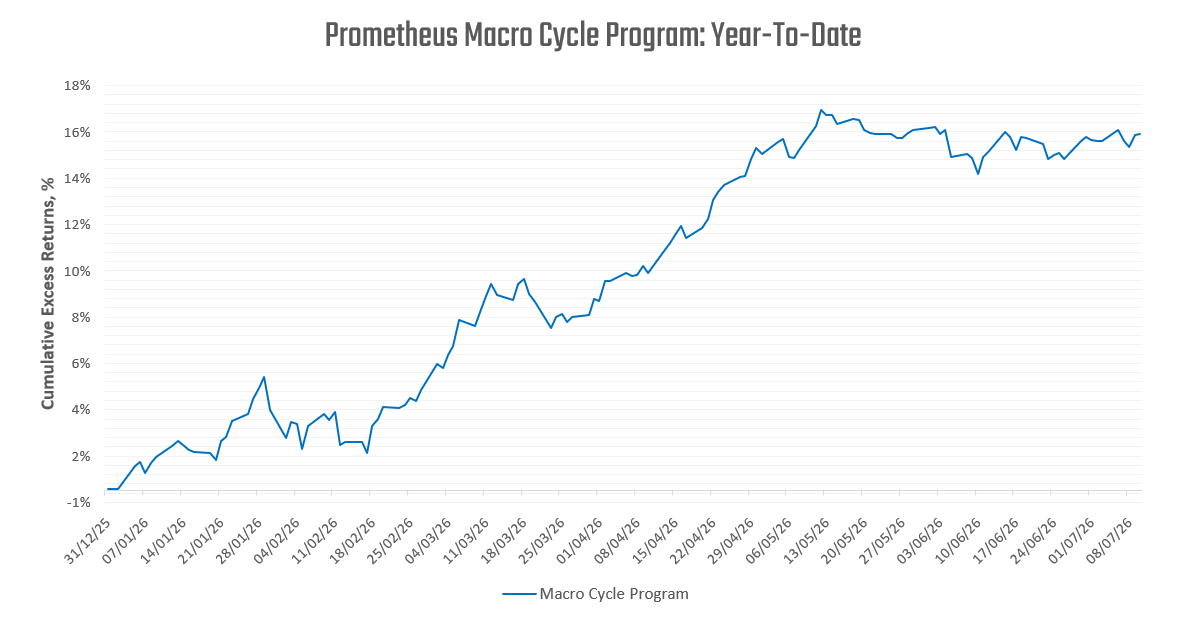

We review our Macro Cycle measures to assess the optimal mix of cycle-appropriate allocations. Leveraging our timely proprietary estimates of the current stages of the macro cycle continues to look attractive. This process has navigated this year quite well thus far:

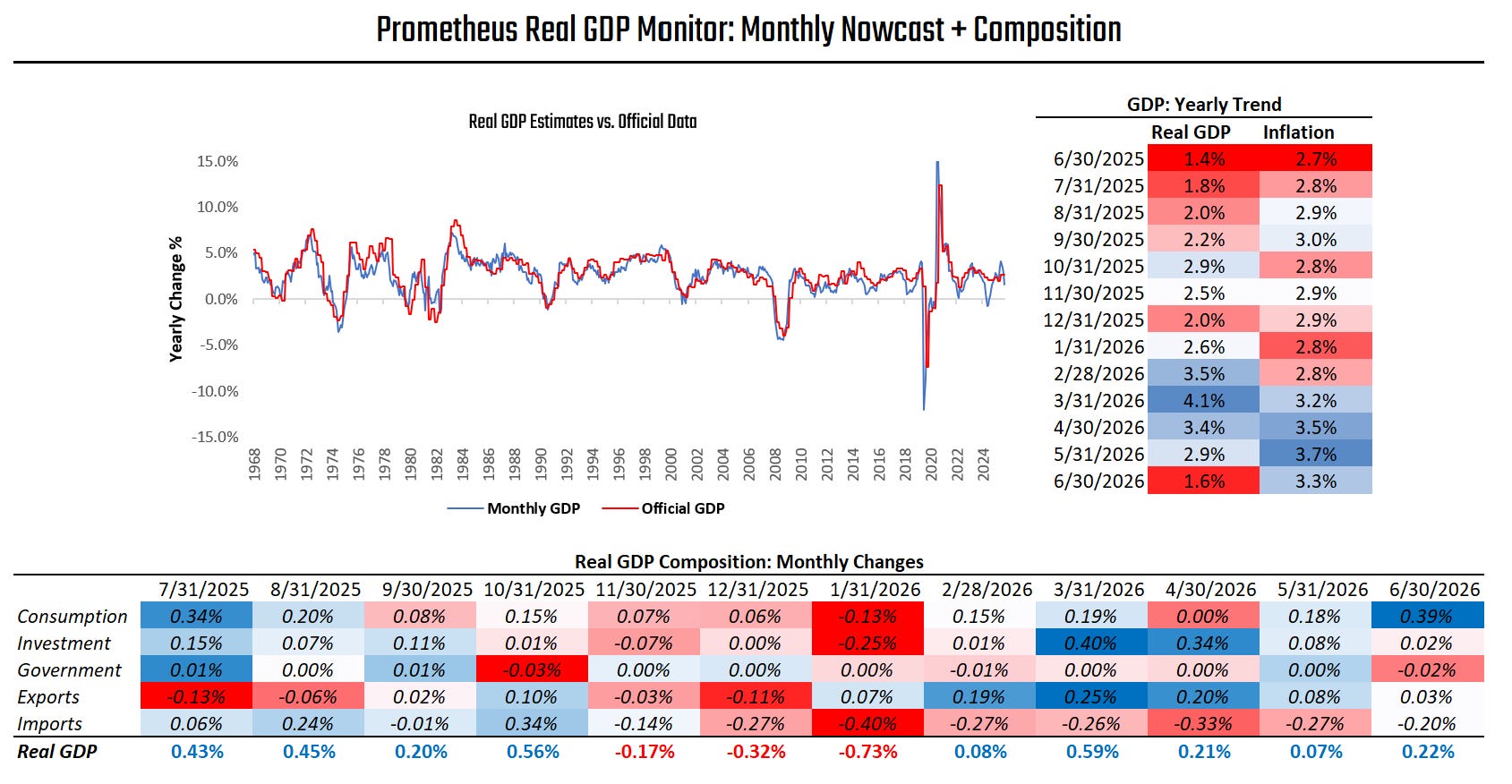

We dive into what our process is telling us. With the official retail sales numbers released, we now have enough data in hand to form our initial estimates for monthly GDP in the form of our GDP Nowcast:

The latest data shows moderating real GDP readings. However, it is essential to recognize that this data is largely being weighed down by volatility in trade data rather than consistent domestic weakness. Isolating the domestic drivers of economic activity, we continue to see the domestic real GDP growth of 2.5%. This is largely consistent with our high-frequency estimates of GDP growth:

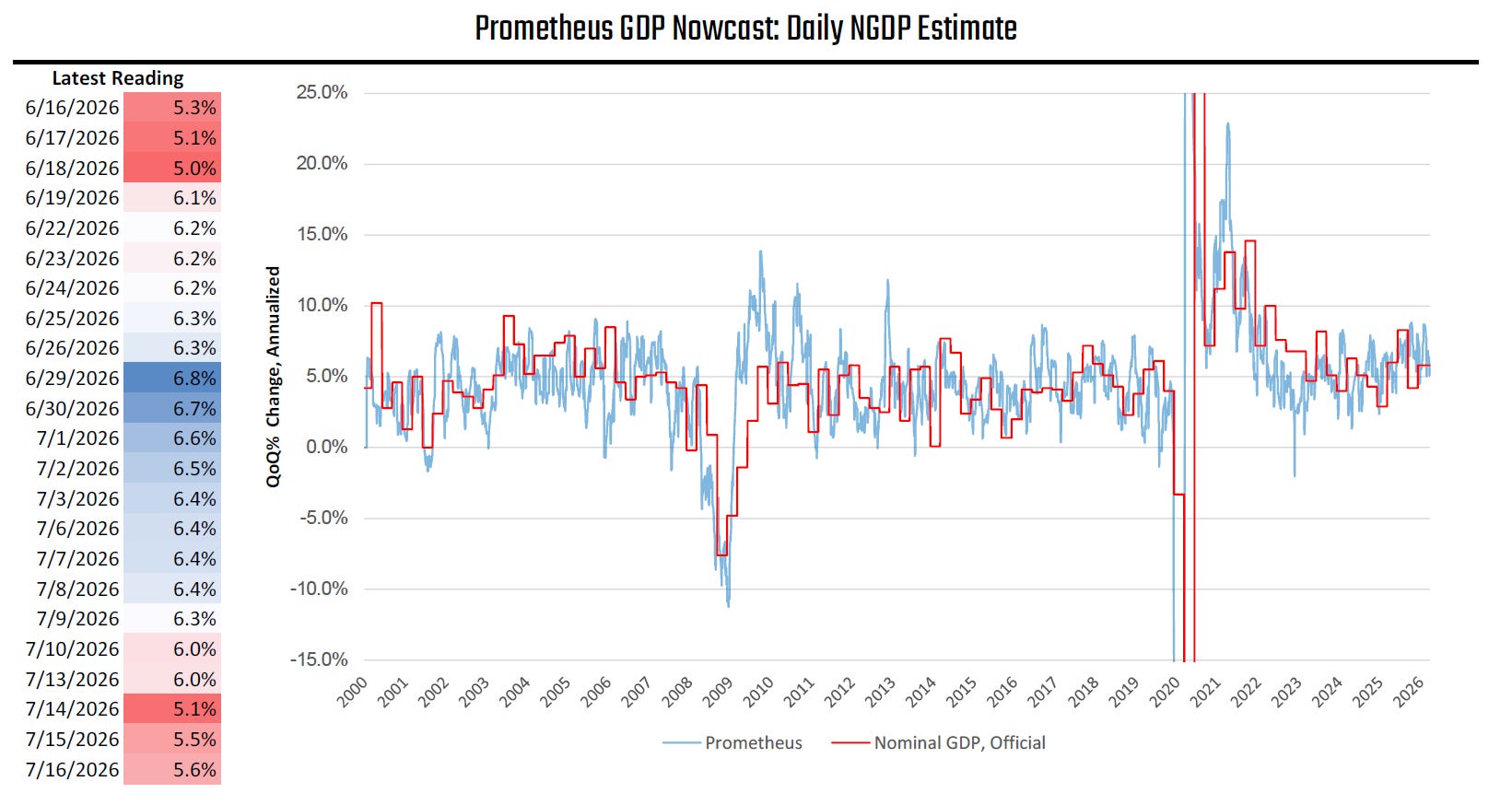

Furthermore, our daily business cycle gauges continue to show an expansionary business cycle: