We review our Macro Cycle measures to assess the optimal mix of cycle-appropriate allocations.

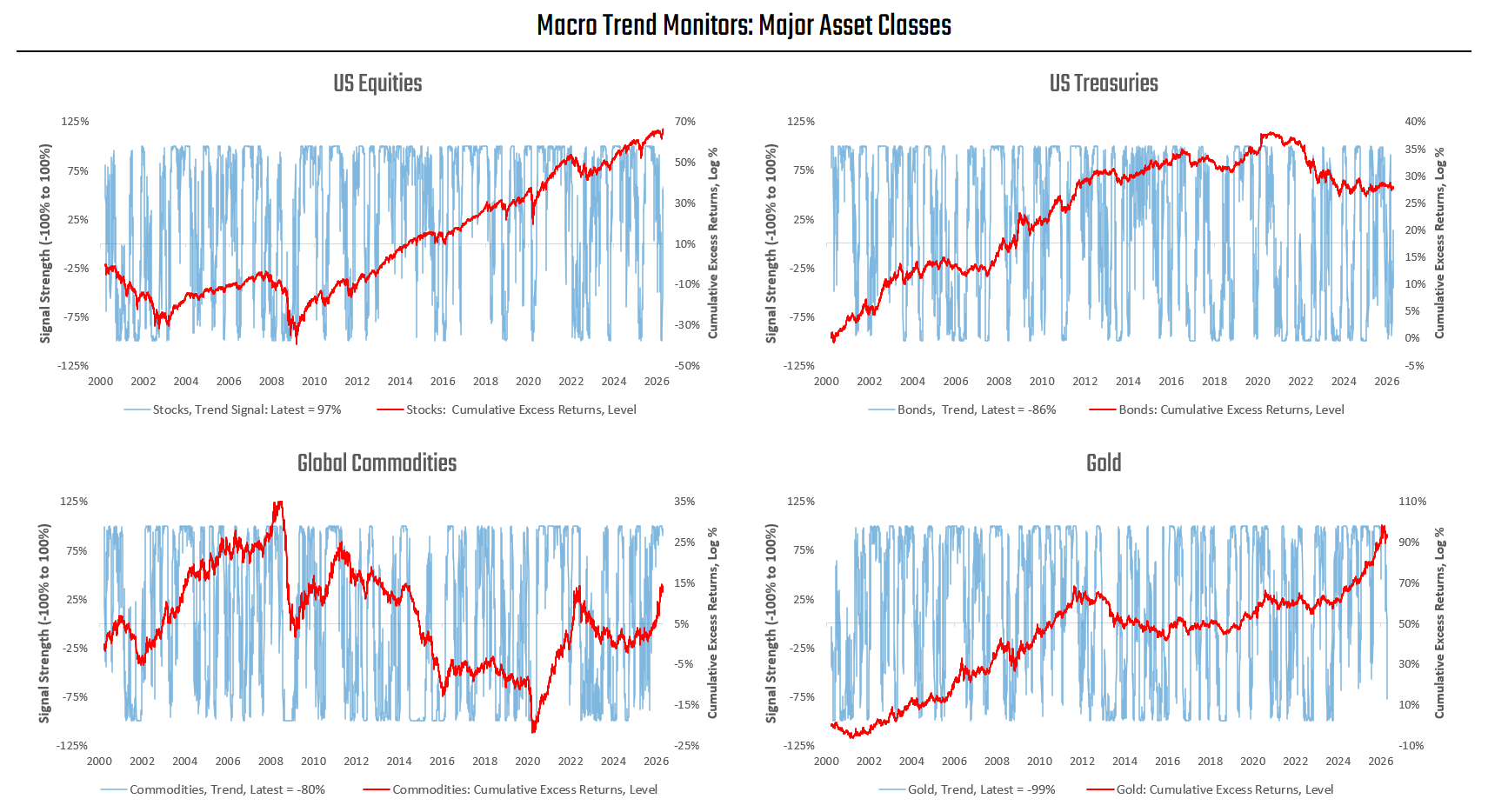

We begin with major macro trends across stocks, bonds, and commodities (US-focused). Scanning across those markets, we continue to see US equities as the only markets with persistently positive trend strength:

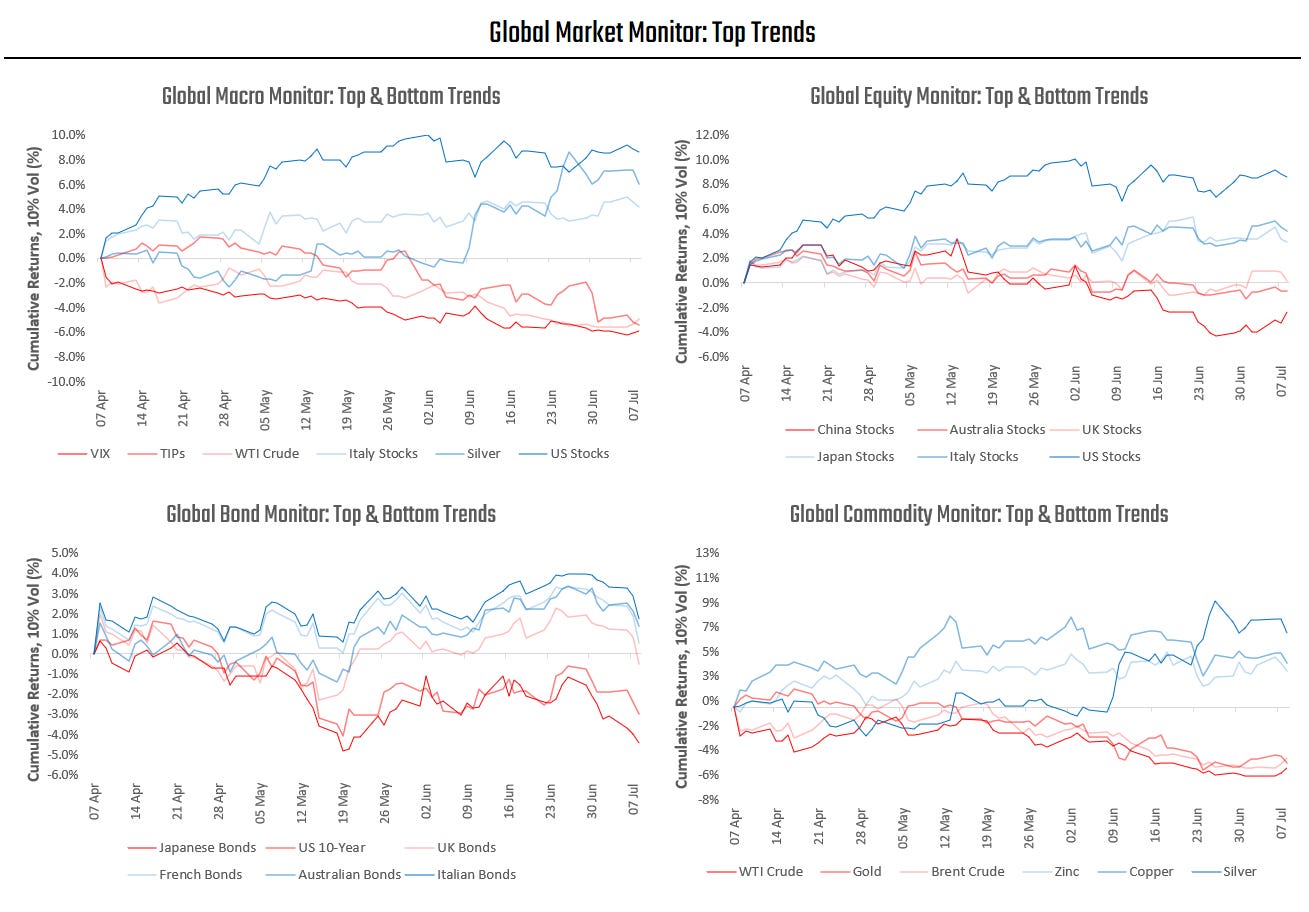

We see these trend signals reflected in the distribution of global market returns as well, with US equities leading the pack amongst global assets:

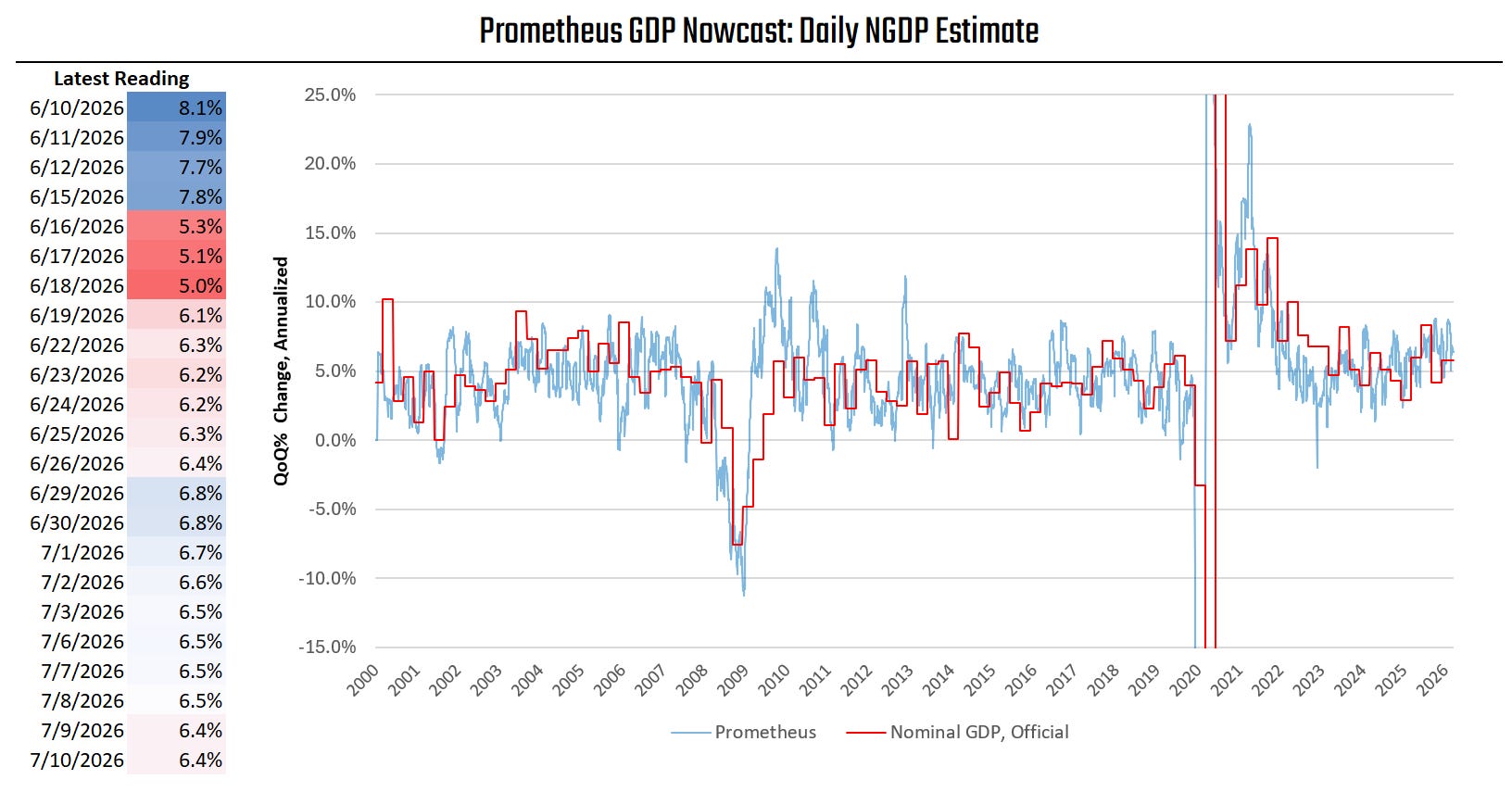

These macro market trends are largely supported by our fundamental gauges. Our timely reads on nominal GDP growth continue to show a steady expansion:

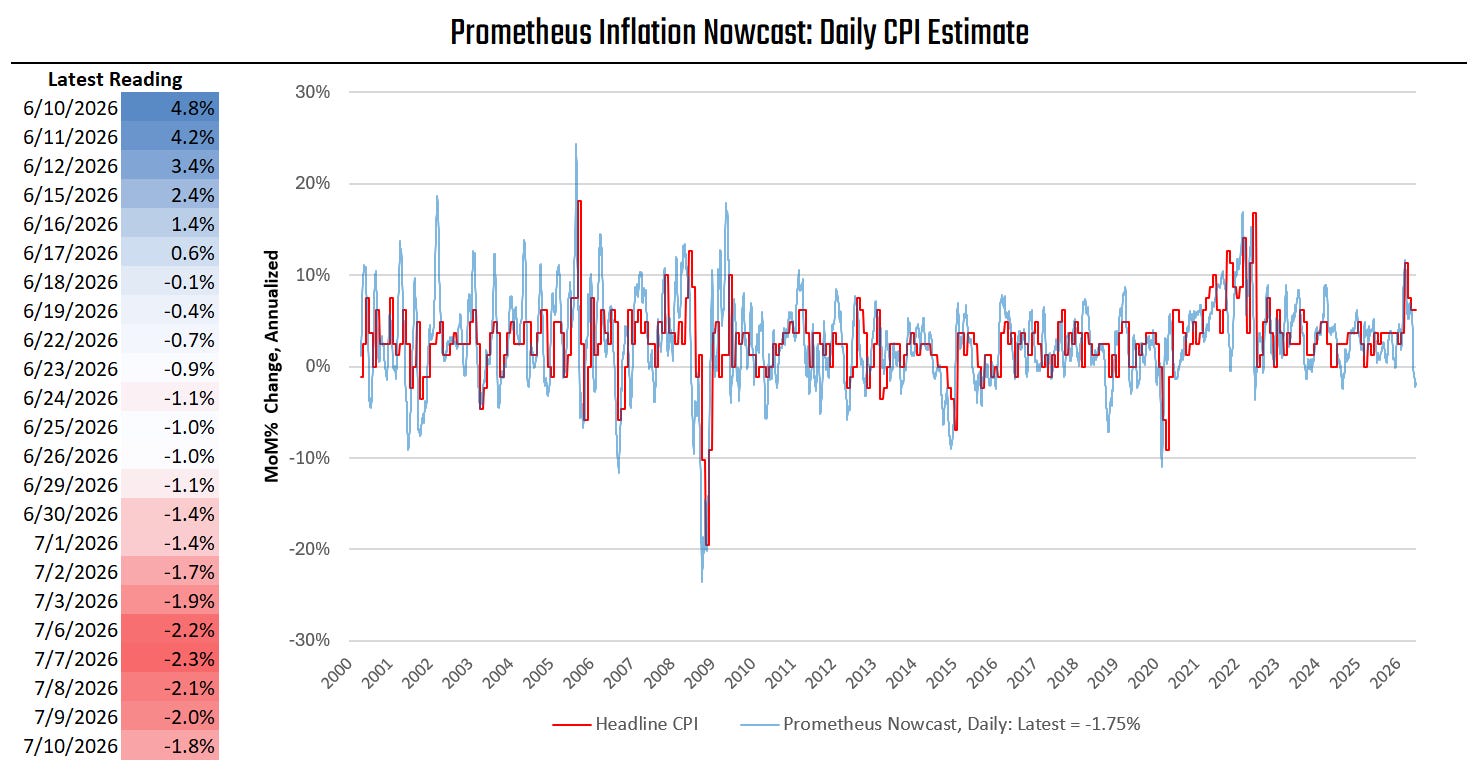

Meanwhile, our inflation readings continue to suggest near-term disinflationary pressures:

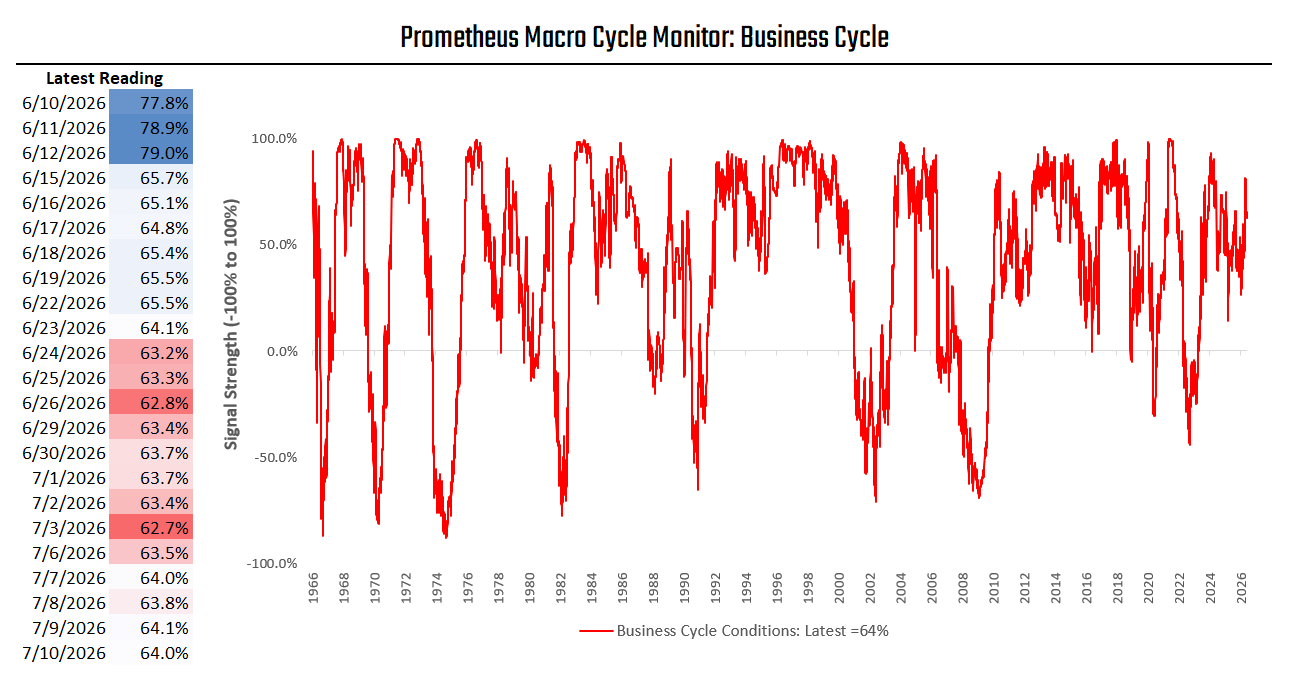

Additionally, our business cycle gauges continue to show an expanding business cycle:

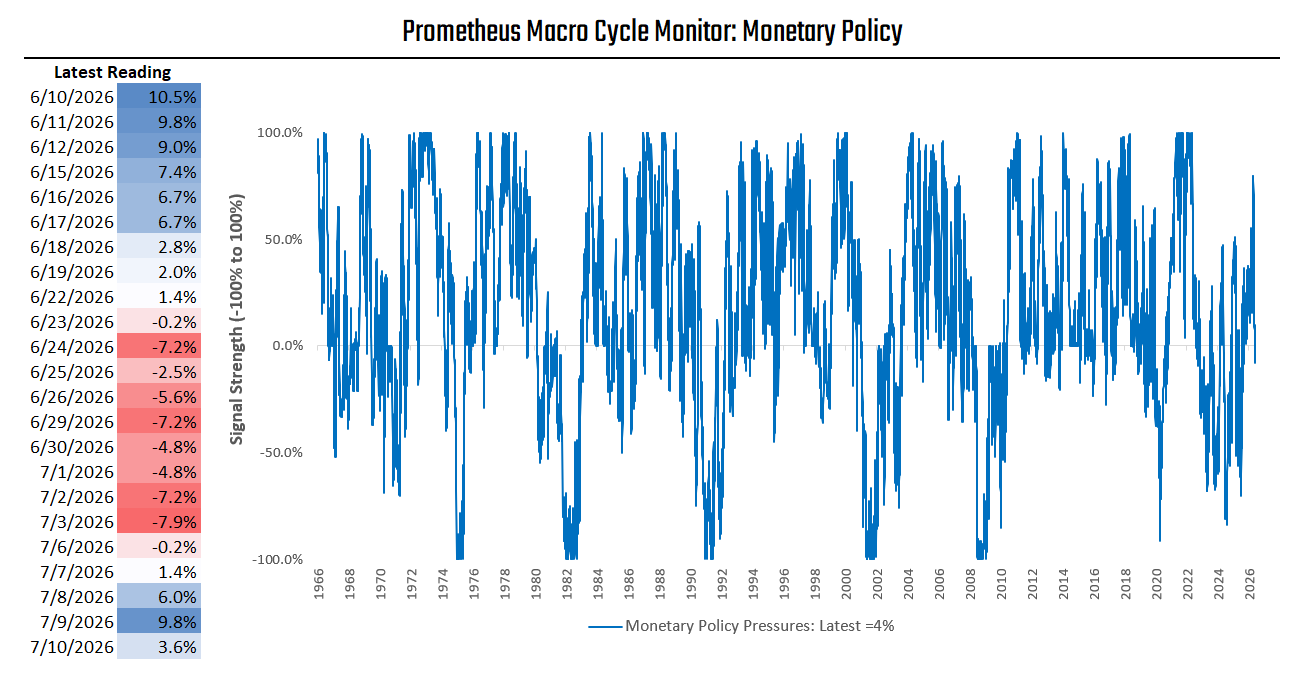

And our monetary policy pressure gauges are now neutral:

The combination of these dynamics continues to suggest an economy in steady-state expansion, with significant inflation volatility driven by oil price dynamics.

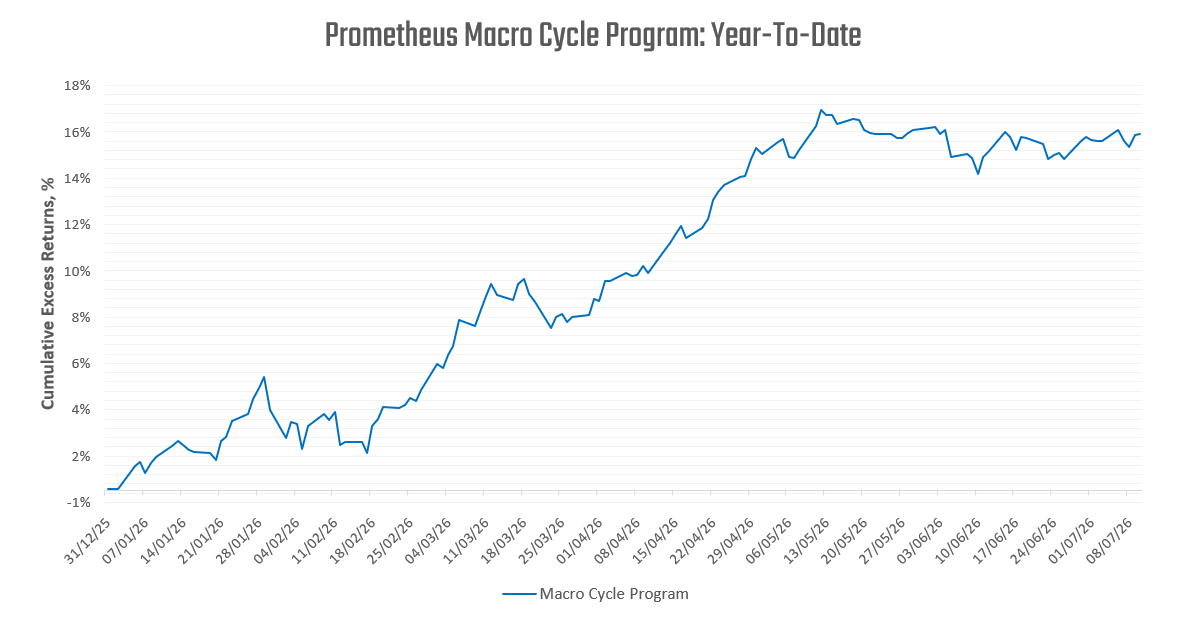

Leveraging our timely proprietary estimates of the current stages of the macro cycle continues to look attractive. This process has navigated this year quite well thus far:

Combining our indicators, a Macro Cycle Allocation would be long