A scan through the latest labor market data.

The latest jobs data continued to show mixed readings. Payrolls showed weakness relative to expectations but continued to expand, while unemployment rates continue to show tight labor markets and surprised to the upside.

Demographic shifts, in the form of lower participation rates, continue to weigh on labor market growth, as reflected in the household survey. Meanwhile, the establishment survey continues to reflect strong business cycle conditions.

Our synthesis remains that these divergences in labor market data continue to come from deviations between the secular and cyclical drivers. We continue to see the labor market as one challenged by falling participation, but supported by a strong economic cycle.

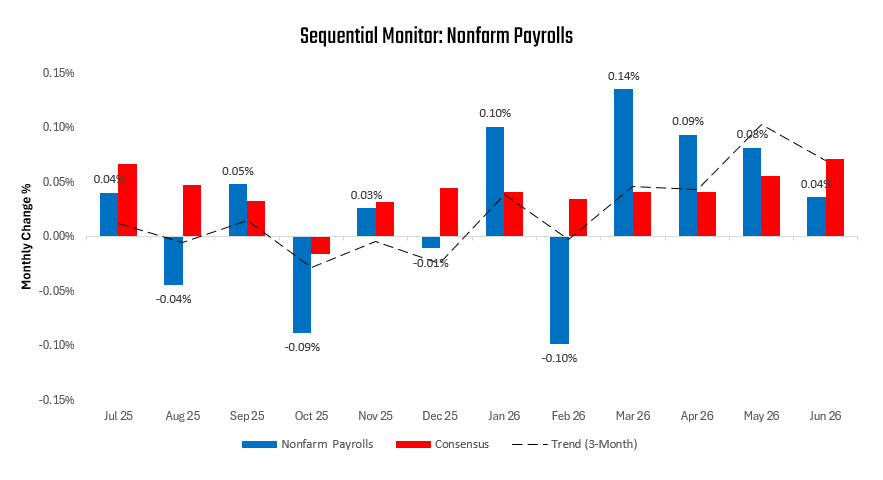

We work through the data driving this synthesis. We start with the latest payroll numbers, which showed a minimal increase, which also disappointed consensus expectations:

While the latest print did not show strong job gains, it also did not stop the recent momentum:

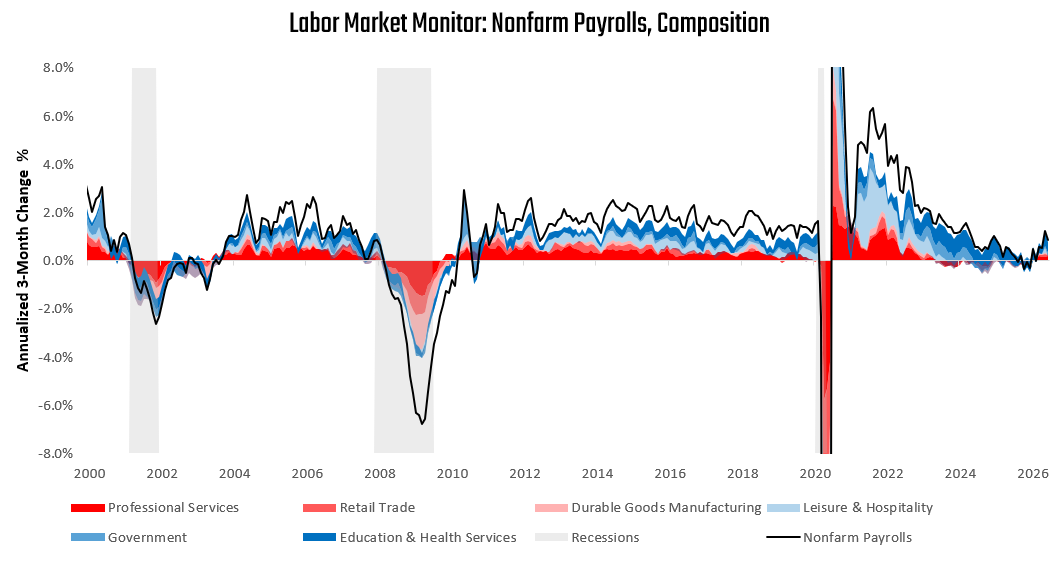

As shown, recent nonfarm payrolls have shown signs of acceleration. These signs of acceleration have come alongside improving labor market breadth:

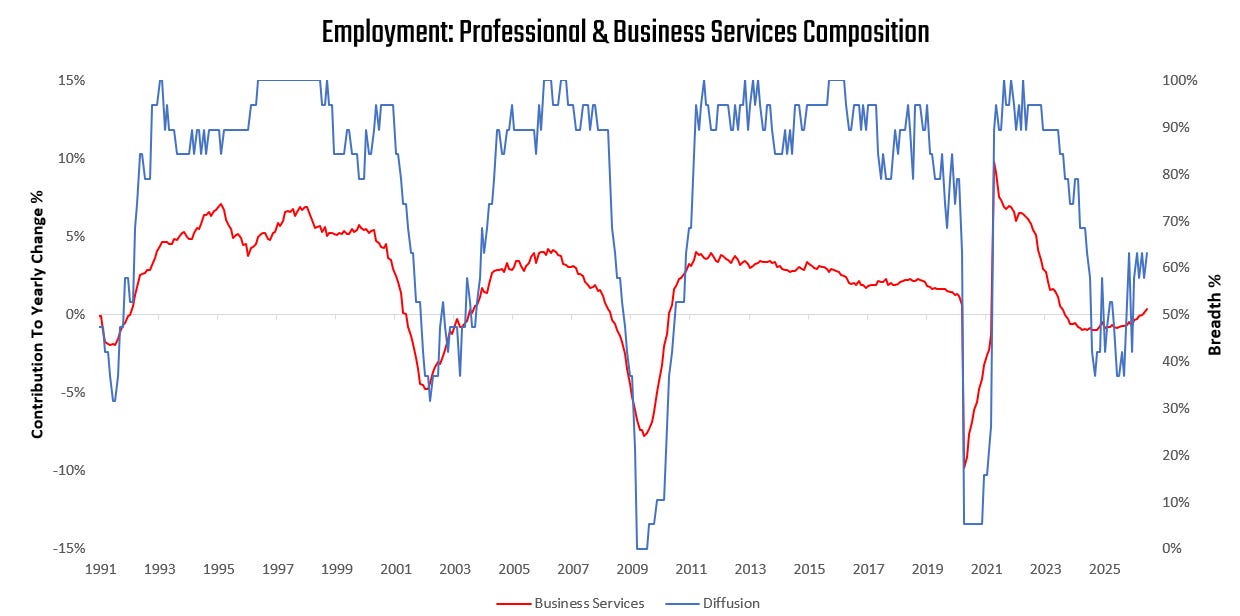

Importantly, this improving breadth has come with a nascent recovery in business services, a large segment of the labor market which has been under pressure. This sector’s employment has been inversely correlated with tech capex, i.e., companies have invested more and hired less. However, we are seeing the initial signs of hiring resuming:

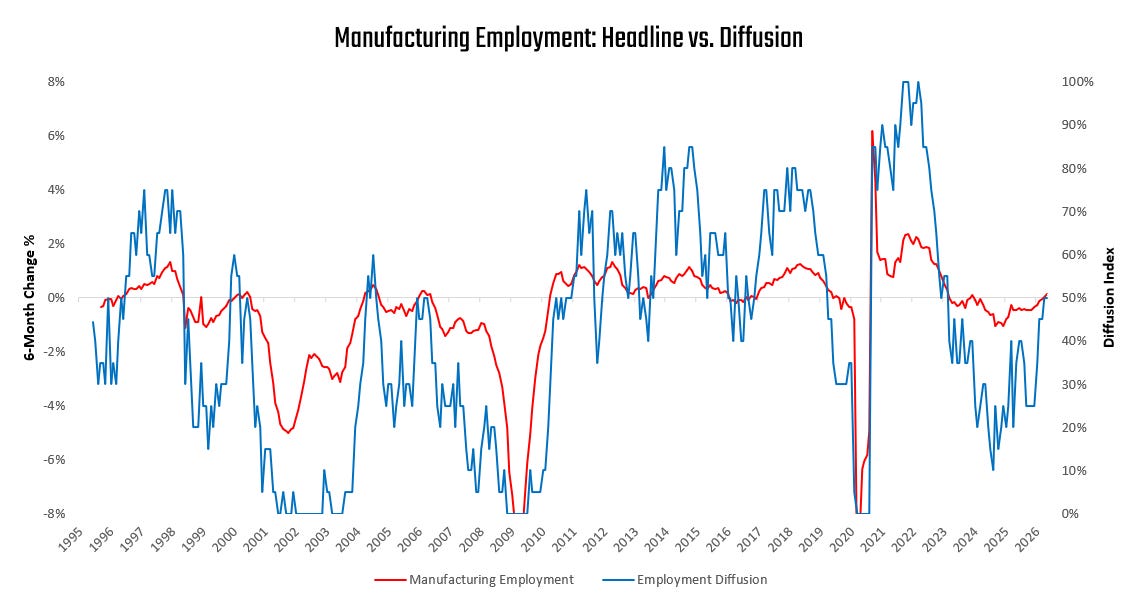

Additionally, we see another integral driver of the business cycle experiencing rising employment: manufacturing.

Thus, while the latest month-on-month data was slow, broad-based indications from the payrolls survey continue to suggest improving conditions.

Meanwhile, the household survey continues to paint a weaker picture:

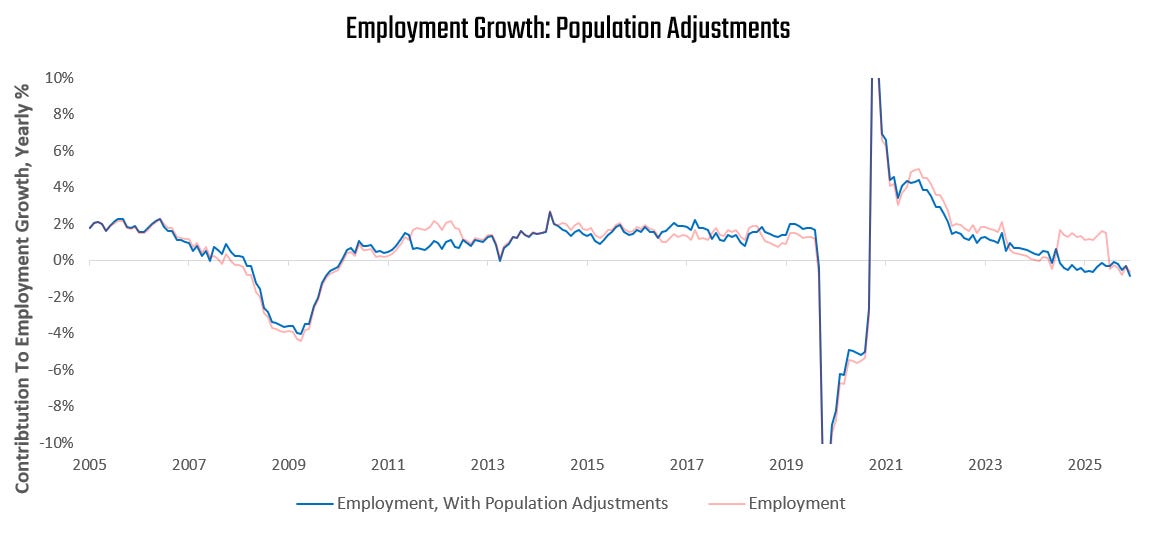

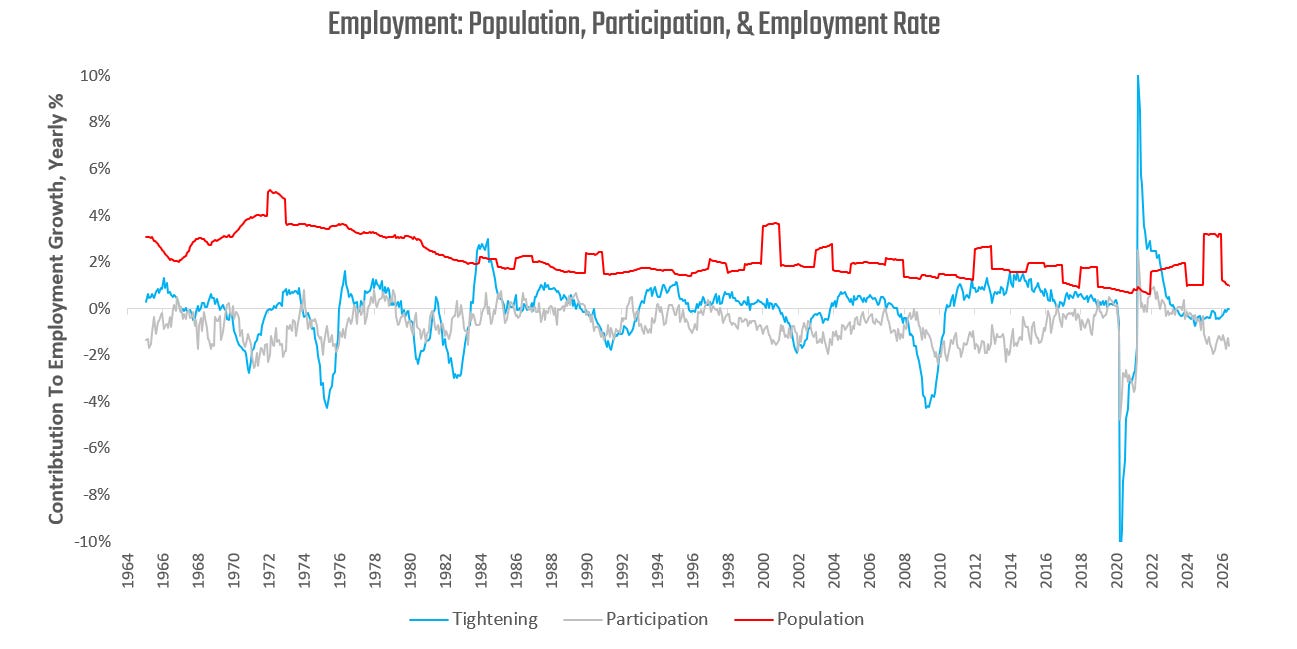

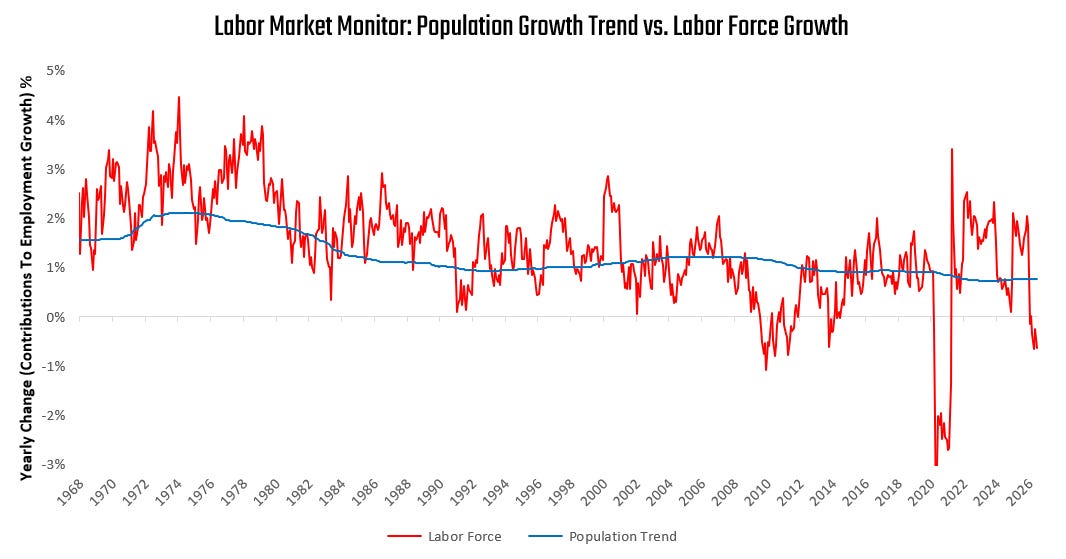

As we have noted for more than a year now, the weakness in the household survey continues to emanate from participation rates falling. We show our decomposition of labor markets into participation, changes in population, and labor market tightening:

We isolate the effect of labor force weakness on employment growth, which we can see is a material downward pressure on employment:

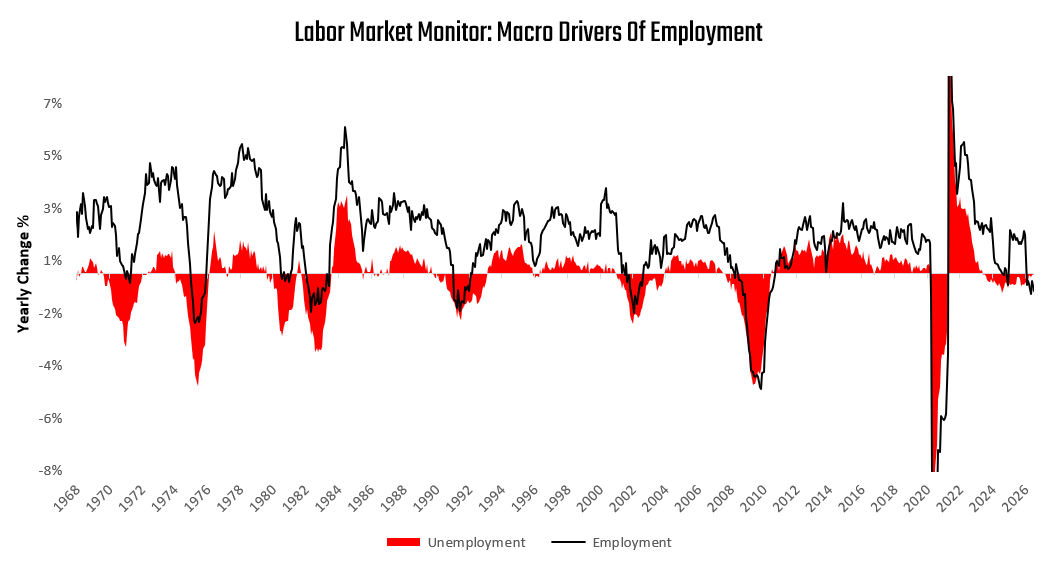

It is crucial to recognize that while this labor force dynamic is a weight on employment growth, it is not indicative of underlying business cycle conditions. We show how over time, employment rates are the driver of cyclical variation in the labor market:

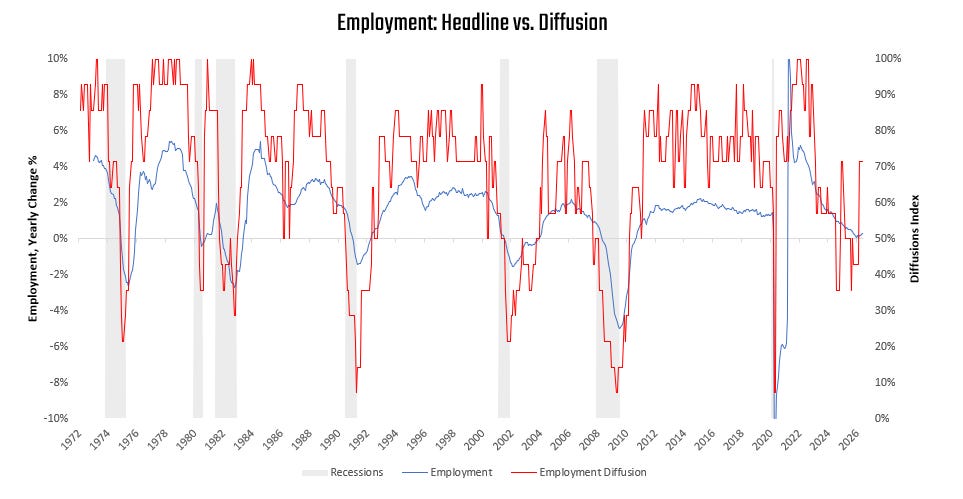

When we zoom in on unemployment conditions, we continue to see a tight labor market. Given the secular tightness, there is little room for further acceleration, but we see no signs of deterioration:

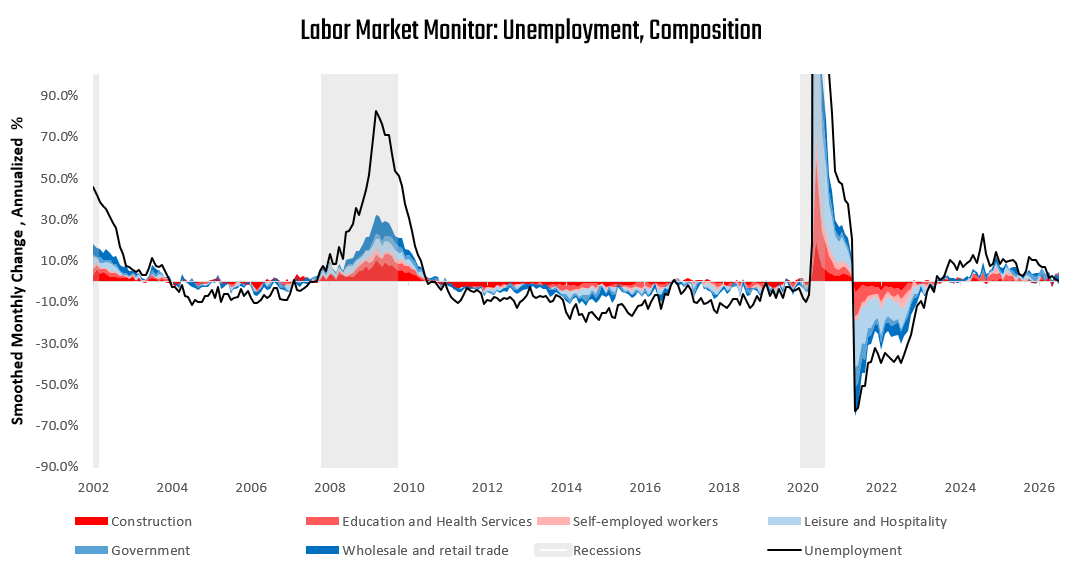

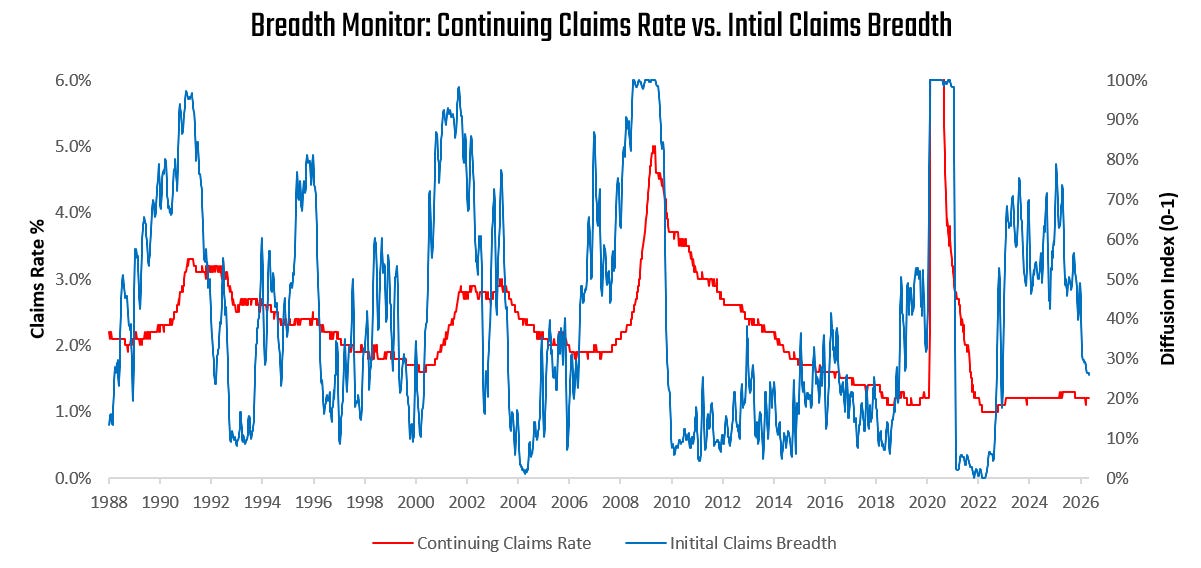

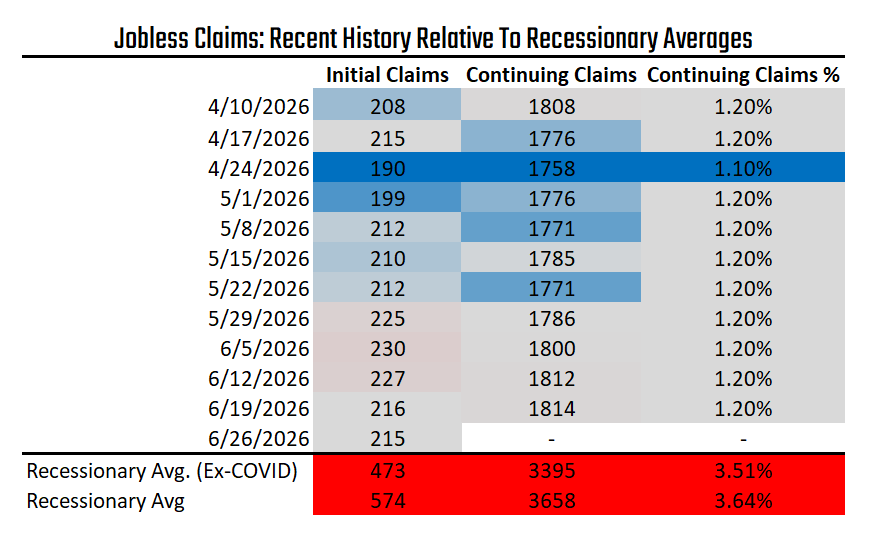

Mirroring these unemployment dynamics, we see the latest claims data continuing to suggest a tight labor market:

These readings remain well-removed from recessionary conditions:

Scanning across the broad range of labor data, we see a labor market limited by demographic shifts driving down participation rates. However, from a business cycle perspective, we continue to see a strong labor market, consistent with business activity.