The war dynamic in Iran has driven the largest oil shock in recent history. There remain material probabilities that the inventory shock persists regardless of the war's outcome. Since the war announcement, our systems have maintained long exposure to the oil complex. Today, we offer our insights on how to think through the risk/reward of this exposure and its risk management.

We scan through:

Expected Returns

Positioning Risks

Short-Term Regimes

To chart a course for managing energy exposure.

Let’s dive in.

We begin with the Expected Returns. For those unfamiliar with our approach to expected-returns investing, you can find a complete breakdown here:

Where Are The Expected Returns?

Expected returns form the foundation of all investing. We invest in assets that are at a discount to their expected future value and earn compensation for bearing uncertainty around that outcome. The expected compensation for bearing this risk is the source of returns in investing. While most asset classes exhibit positive expected returns over long ho…

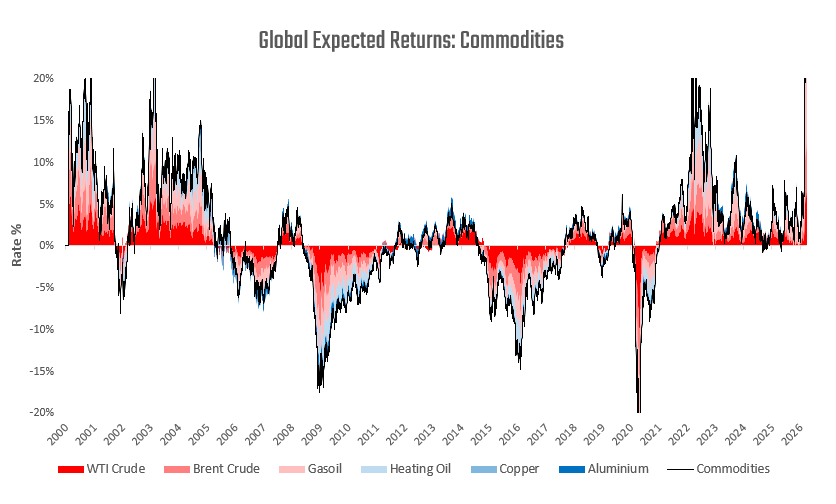

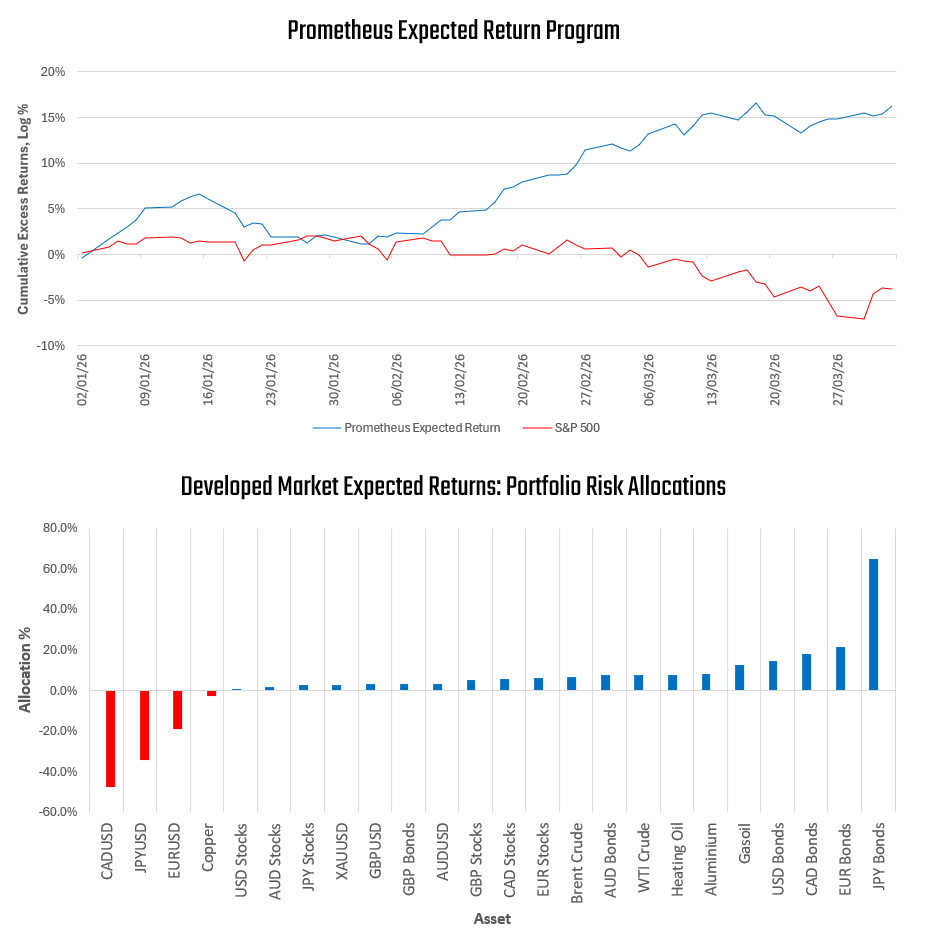

Energy market term structures continue to offer the most attractive risk premiums we have seen in the Russia-Ukraine War in 2022. We visualize this risk-premium below:

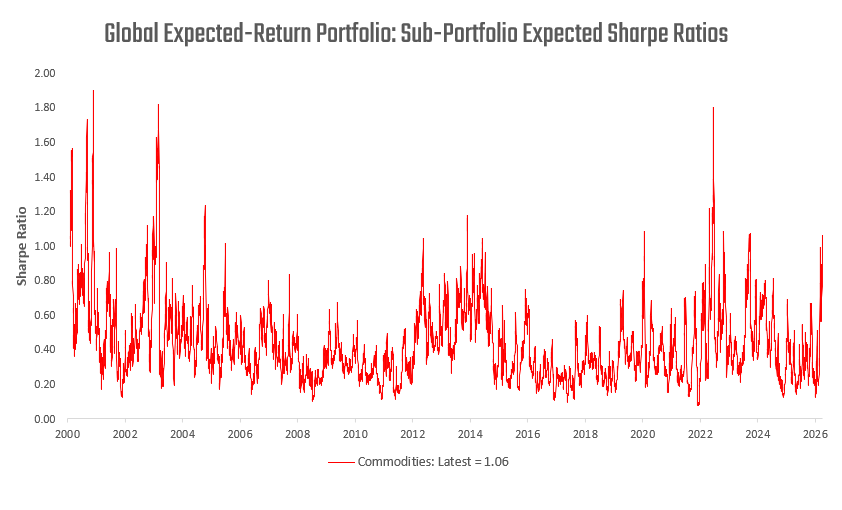

We can translate these expected returns into Naive Expected Sharpe Ratios, which are commensurately elevated:

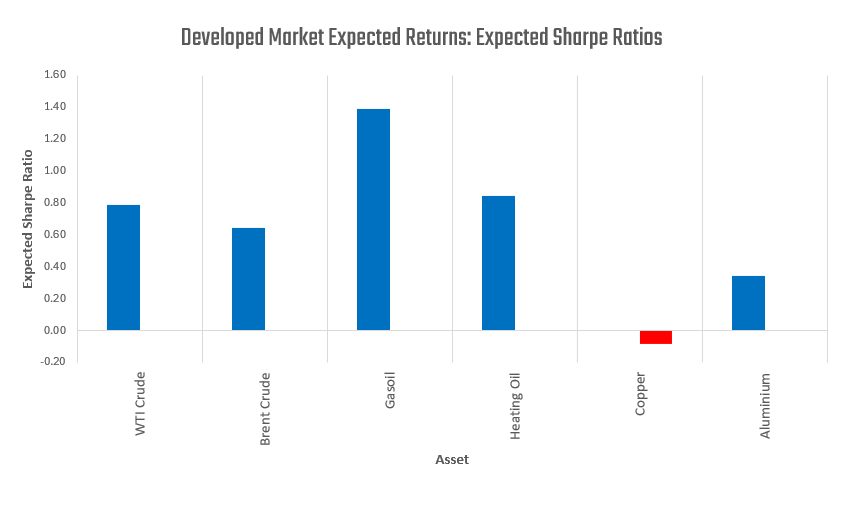

We show that the distribution of these expected returns is uniform amongst the energy complex (ex-industrials):

For many investors who are native to equity and bond markets, these pro-cyclical expected returns (expected returns that rise with price rises) are unintuitive. In commodities, supply shocks drive up the spot price, while hedging pressures create a backwardated term structure. The combination of these dynamics creates a time-varying risk premium for those willing to buy the commodities into price increases. This dynamic opposes the mechanics in equities and bonds, where investors are largely rewarded for buying assets on weakness.

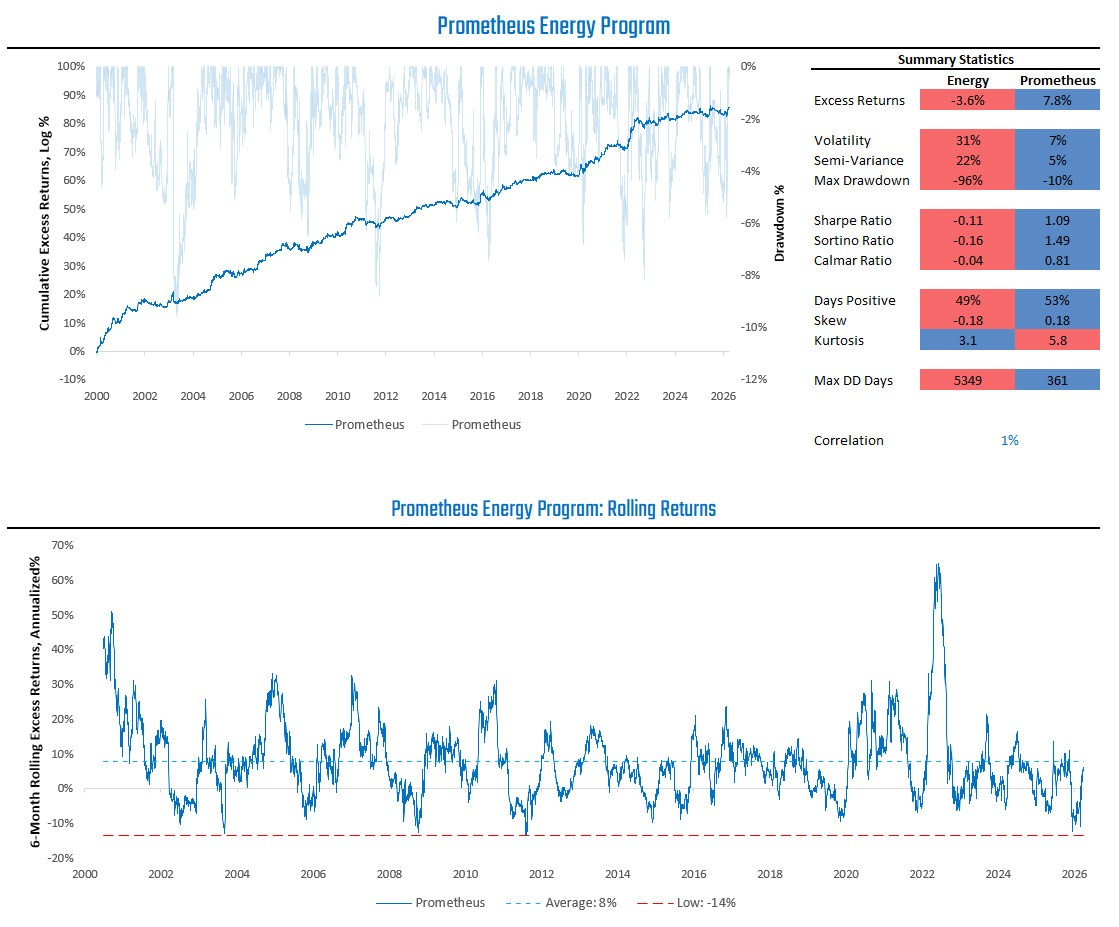

It is the systematic recognition of these mechanics that has allowed the Prometheus Expected Return Program to perform strongly in this environment:

Thus, we think that if there is a time to own commodities, it is in this type of backdrop. However, we need guardrails against a sudden turn in these conditions. Much of today’s regime’s dynamics are contingent upon the policy actions of the US administration and Iran's reaction function. A quick de-escalation of the military conflict will unwind speculative positioning in energy, but is unlikely to fully restore global supply in the near term or to remove the geopolitical risk premium now priced into global energy markets. As such, the biggest threat to energy exposure today is a military de-escalation-induced unwind in positioning.

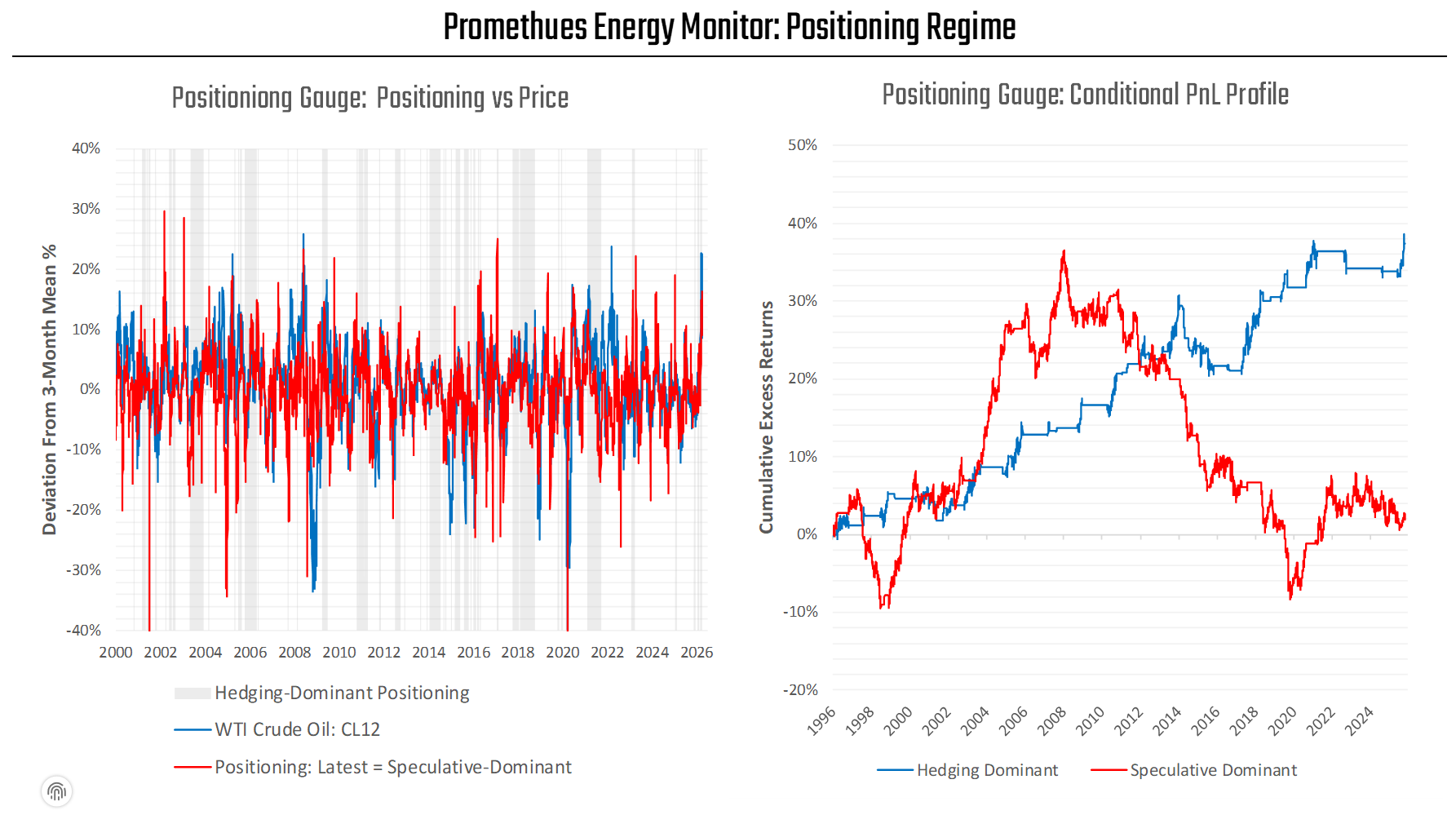

To help navigate these dynamics, we share our positioning gauge (updated daily for Prometheus Institutional clients), which helps us determine whether prices are being driven by speculators or hedgers. A Speculative-Dominant oil market is more fragile than a Hedging-Dominant market:

Today, we’re in a Speculative-Dominant environment, with risk of a big positioning unwind. However, in the background, we also see a good amount of hedging from commercials. As such, we are in a positive, but not optimal, backdrop for energy positions. A modest unwind of speculative positioning, while negative in the short-term, may be the ideal backdrop for the energy complex over the medium-term— a dynamic we will continue to be on the lookout for. Until then, positioning risk abounds and should temper sizing.

Finally, we share our proprietary short-term regime recognition from the Prometheus Energy Program. To help our subscribers navigate these uncertain times, we continue to share the positions from the program via the Substack chat feature:

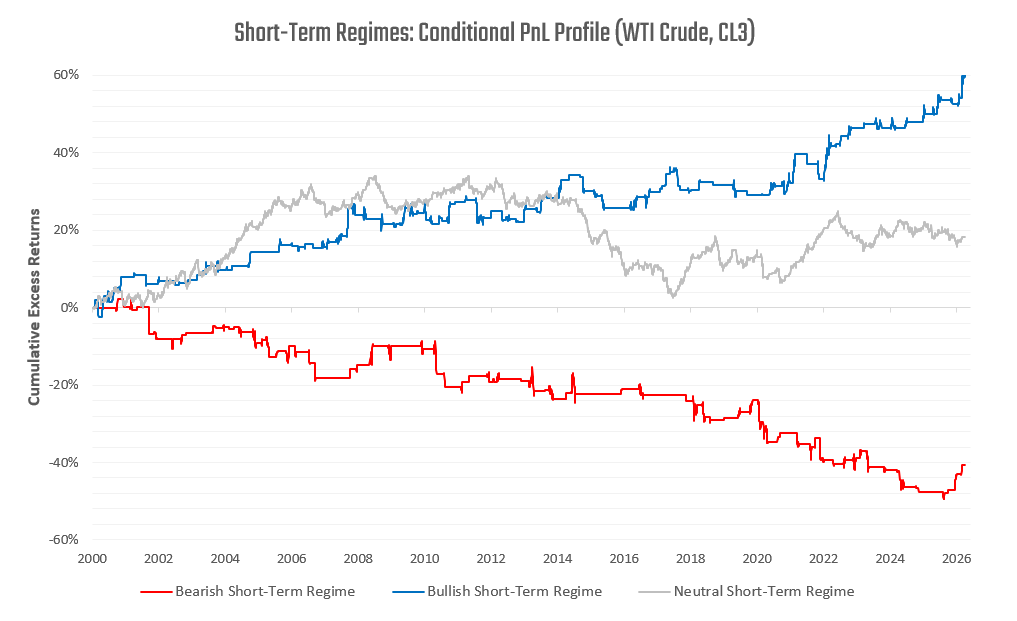

Based on the program's underlying signals, we can classify regimes as Bullish, Bearish, or Neutral. The objective is to identify the highest-signal periods for energy markets, not every signal:

As we can see above, our short-term regimes are good guides for the short-term price regime. Currently, these signals suggest we are in a Neutral Short-Term Regime, after being in a Bullish Short-Term Regime over the last month. This is not a bearish or bullish sign, but just an indication that short-term forward returns are less predictable than they have been recently.

Looking across Expected Returns, Positioning Risks, and Short-Term Regimes— we think energy exposure continues to make sense in the current backdrop. However, being prepared for a speculative unwind in sizing and drawdown controls remains imperative for navigating this environment optimally. If Expected Returns, Positioning, and Short-Term Regimes all align, conditions will be in place for significant long exposure. Until then, a more cautious approach is warranted. Clients of Prometheus Institutional can track the evolution of these conditions daily. Email us at info@prometheus-research.com for access.

Until next time.