We will release our Prometheus S&P 500 program next month. However, markets are moving quickly, and we wanted to share insights from our signals to help investors navigate risk during these challenging times.

The Prometheus S&P 500 Program seeks to outperform the S&P 500 over a full investment cycle. We define a full investment cycle as a period of time where markets have experienced bull and bear markets with a generalized upward drift. Since our last note, the program has performed in line with its design, with our downside protection primarily driving performance.

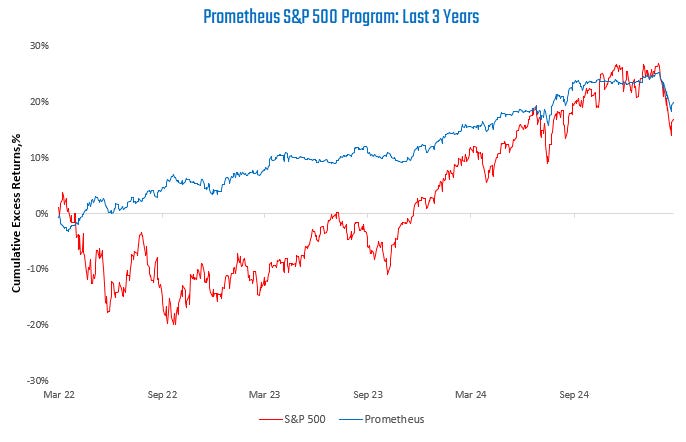

For the purposes of this post, we will share the programmatic views of the conservative version of this program. This program targets a maximum of 10% expected risk. This version will lag indexes during extremely strong, highly volatile bull markets. However, over the full investment cycle, this program seeks to outperform by maintaining responsible upside exposure while reducing or avoiding drawdowns. We visualize the simulated 3-year returns below:

Today, while equity markets are in a drawdown of approximately 6.5%, the program has taken only about half that drawdown, maintaining a drawdown of 3%. This is consistent with the portfolio objectives. Today, the portfolio is positioned as follows:

Our strategies continue to maintain largely the same exposures as last week. Our 10% risk control continues to limit equity risk, with modest Treasury and cash positions as complements. There are three major takeaways from these positions:

Beta Timing: Our beta timing program suggests a higher likelihood of positive forward returns than negative ones. The economy is still in expansionary territory, and this sell-off has cheapened equities relative to other assets, earnings expectations, and recent price levels. Despite accounting for near-term trends, our beta timing process indicates a positive near-term outlook for equities.

Sector Selection: While our Beta Timing engine continues to suggest a positive near-term outlook for equities, we would be reticent to neglect more standard valuation measures. These measures have reduced our overall sector exposure. Within the cross-section of equity sectors, our signals prefer Industrial & Technology stocks as their investment activity continues to climb. While the medium-term outlook for equity expected returns is low, we expect relative value opportunities for sector selection.

Risk Control: We think this one is crucial. Any long-term investor seeking to outperform equities over the long term can benefit from controlling their risk, especially when equities have large and sudden drawdowns. By reducing overall exposures when the equity market has a spike in volatility, we reduce the volatility drag on our portfolios. With equity volatility spikes, pulling back on total exposure is essential and likely to be additive.

Bond Overlays: Our systems have deployed a tactical bond overlay. However, with equity market trends now closer to a turning point, our strategies may begin to reduce bond exposures if a durable upside equity trend performs.

We think combining these measures will allow investors to have significant upcapture during a bull market and limited downcapture in a bear market. These observations come from a time-tested approach to markets. We visualize this testing below:

Equity markets have begun to see moderately improved trends. Our systems see the potential for these trends to continue to improve. If trend breadth widens and equity volatility begins to compress, we will likely begin to reduce bond exposures as our strategies increase equity exposures.