We offer an update to our short-term regime signals for crude.

Before we dive into today’s note, we want to flag our latest milestone: 15,000 readers. Prometheus continues to grow and remains committed to bringing institutional-grade systematic investment strategies and research to everyday investors. To welcome you all, we’re offering a discount to new subscribers for the next year:

The offer ends soon. See you on the other side.

This update will be brief. For our longer-form views on managing energy exposure, we recommend our recent note on the topic, linked below. This note will serve as an update to the same.

The case we’ve outlined for a month now has come to pass— we’ve got the speculative unwind of energy positions following a de-escalation announcement from Trump. Energy tanked as expected. We hope you’ve applied our near-constant guidance to use sizing/stops to mitigate this and have come out with strong performance.

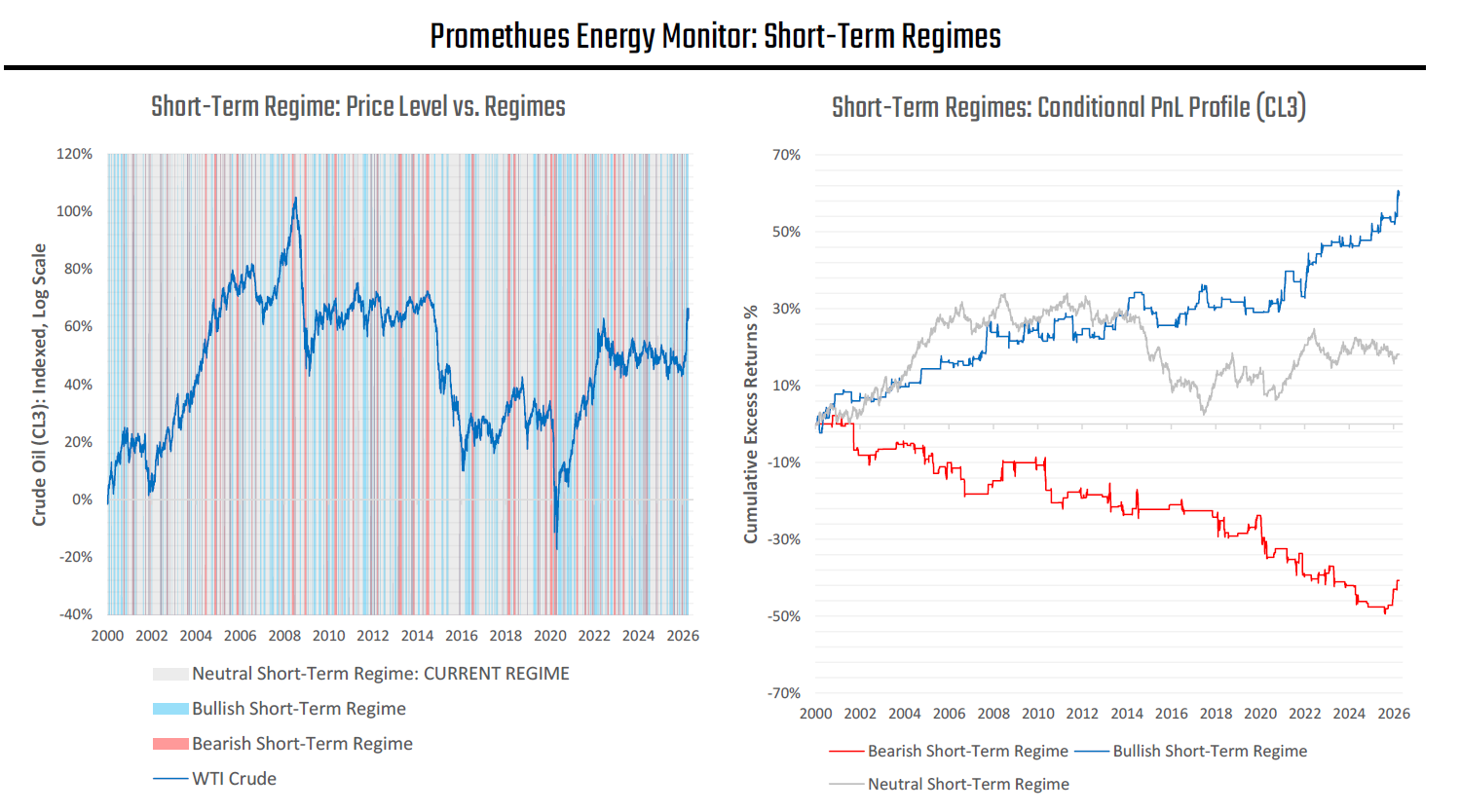

Given this exogenous change, we need to pause and assess conditions, as we have undergone a regime shift. Fortunately, this exogenous regime shift aligns with our proprietary short-term regime signals. As a refresher:

The Prometheus Energy Program uses short-term signals to forecast the energy market in the near term. Leveraging the programs’ underlying signals, we can classify periods into Bullish, Bearish, or Neutral regimes. The objective is to identify the highest signal periods for energy markets, not every signal. These signals offer a roadmap for navigating the short-term backdrop for energy markets.

Our latest regime signals place us in a neutral energy regime, which, per the expected return profiles visualized above on the right, suggests a much less positive energy backdrop than the recent past. Of course, these signals may shift quickly, and we will keep you abreast of these changes.

Fundamentally, we remain a regime of significant oil shortage. This shortage is a strong and consistent support for the entire oil complex. However, we are currently still working through a well-telegraphed unwind of speculative positioning. There is still potential for an extremely strong energy backdrop— but we need time for markets and the economy to digest before we look to play this again.

Until next time.

Just curious, the front month was extremely volatile, while longer-dated contracts like December stayed relatively stable. Does what matters more tend to be volatility at specific tenors, or the volatility of the spread between them, since the latter is what reflects the cost or carry of holding the position?