An update on our macro regime probabilities and daily tracking of fundamental economic conditions and what they mean for macro markets.

Every day at midday, we share updates to our US Macro Regime Probabilities with Prometheus Institutional, along with our synthesis of what the current regime probabilities suggest.

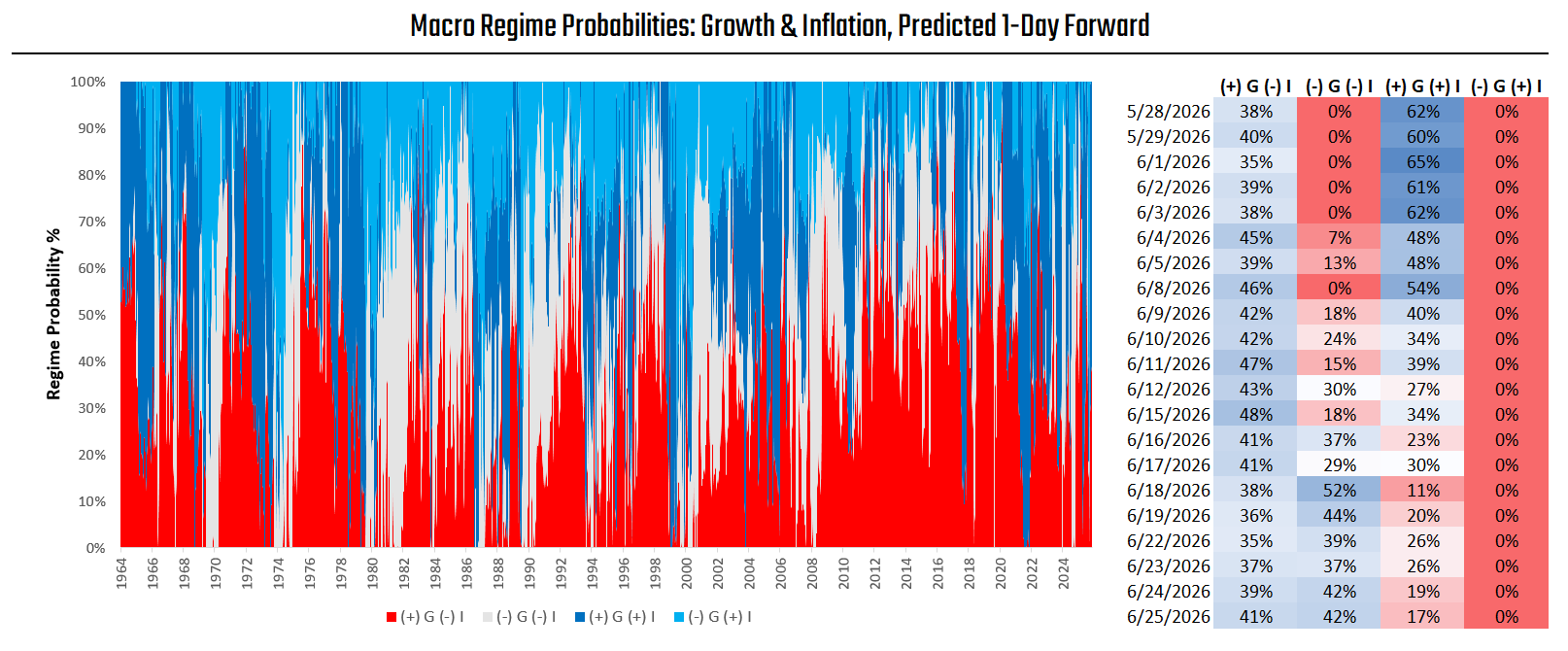

Our Macro Regime Probabilities use our bottom-up signals across asset markets to construct forward-looking estimates for the cross-asset macro market regime. These signals incorporate both fundamental and price-based information to produce high-frequency, forward-looking estimates for the US cross-asset environment. These signals are best used as a forward-looking guide for the cross-sectional returns across macroeconomic assets. We define the regimes as follows:

(+) G (-) I: Rising Growth & Falling Inflation, Equities Outperform

(+) G (+) I: Rising Growth & Rising Inflation, Commodities Outperform

(-) G (-) I: Falling Growth & Falling Inflation, Treasuries Outperform

(-) G (+) I: Falling Growth & Rising Inflation, TIPs Outperform

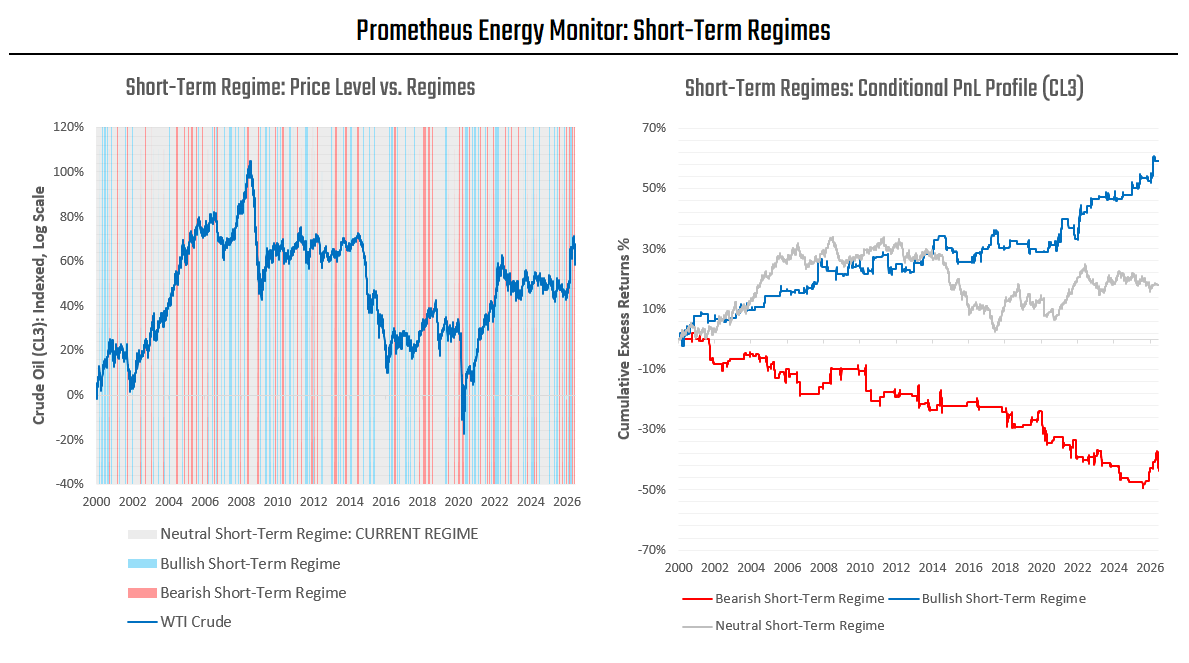

Synthesis: Our Macro Regime Probabilities continued to show a far flatter distribution of macroeconomic outcomes than in the recent past, with a dominance of disinflationary outcomes. As we have repeatedly noted, disinflationary outcomes remain contingent on sustained weakness in the oil complex. Given that oil has reversed most of its post-war announcement moves and global economic activity continues to underpin demand, the potential for a further breakdown in oil prices appears more limited. Furthermore, our short-term regime signals for crude have now turned neutral:

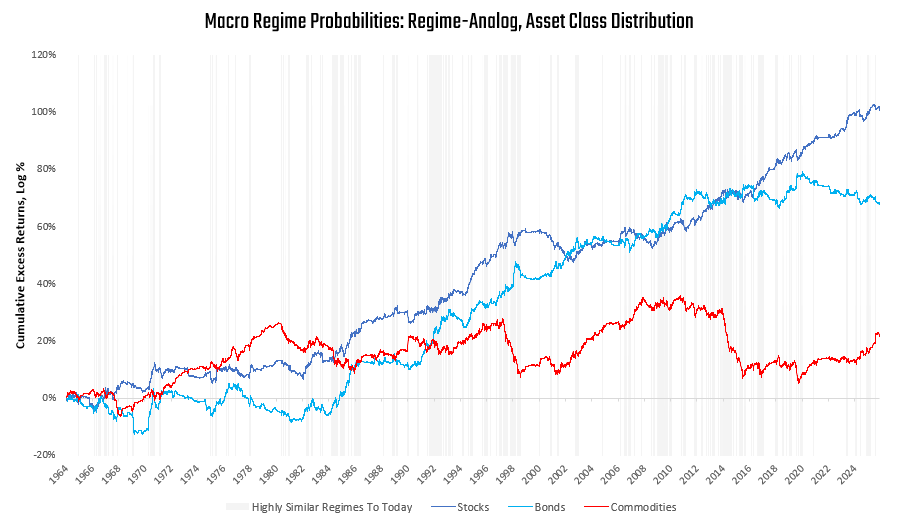

The regime-expected return profiles of assets continue to favor equities and fixed income over commodities:

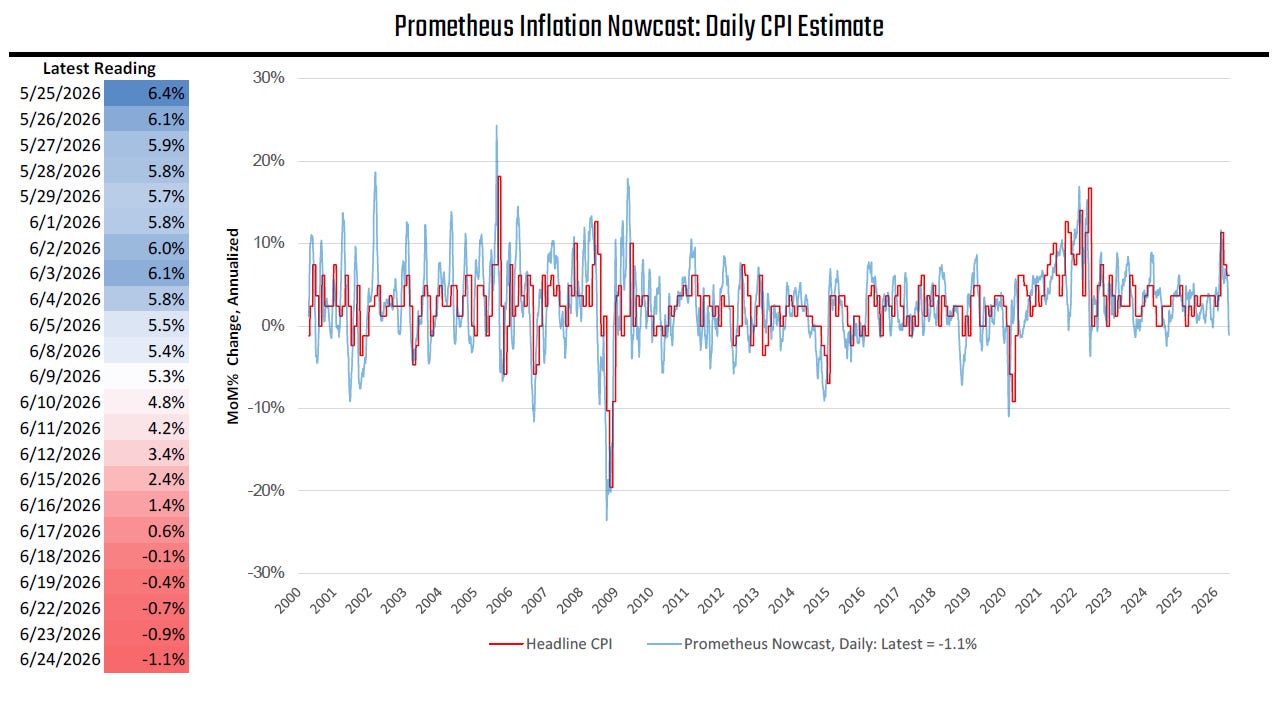

A risk-matched mix of equities and fixed income offers attractive risk-adjusted returns with a historical Sharpe of 0.75 (time-weighted by regime similarity). This is supported by our fundamental tracking as well. Our CPI Nowcast remains well south of 2%:

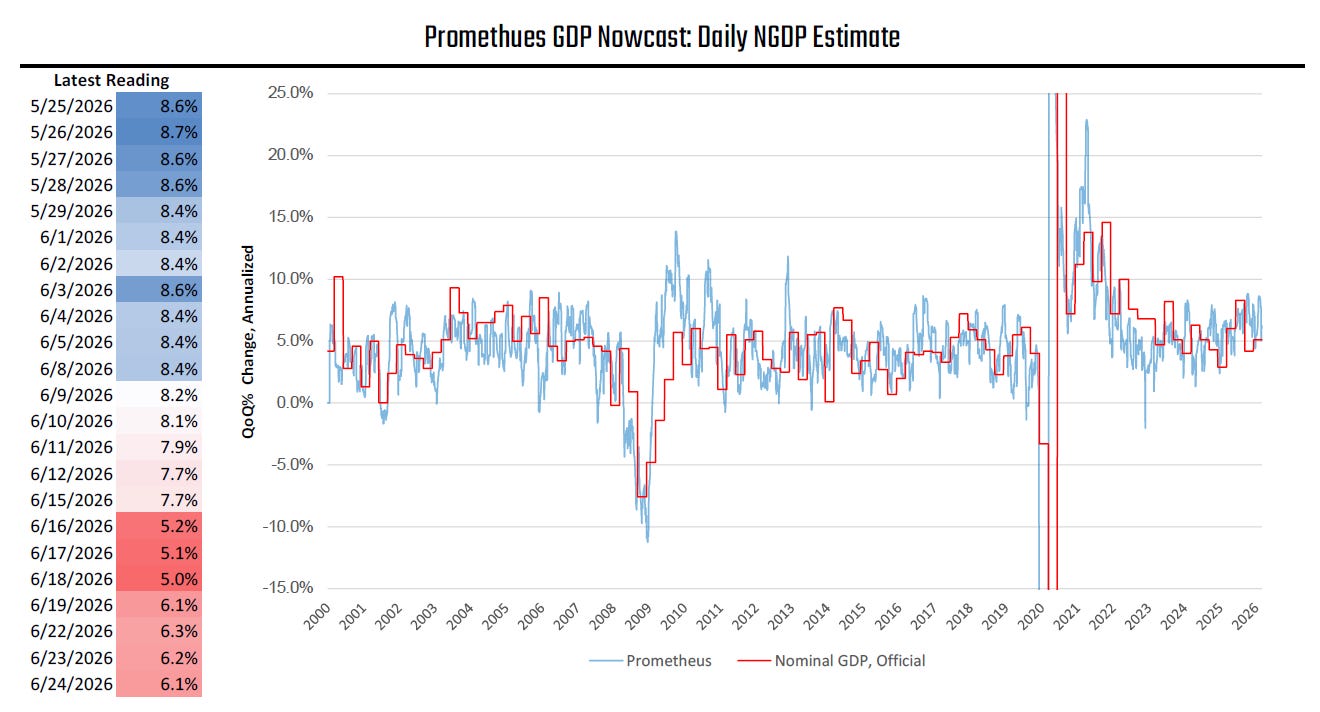

Alongside the near-term disinflation, our nominal growth trackers remain elevated:

Given this backdrop of disinflationary growth, a mix of equities and fixed income looks poised to perform well in the near term. However, we continue to flag that the fixed-income bid remains contingent on sustained downward moves in oil, and current indications suggest there is materially less room for that trend to continue. Equities, while beneficiaries of disinflation, are more insulated from a potential halt to oil declines. A mix of equities and bonds, risk managed with stops, likely offers the best payoff in most scenarios.

Until next time.